So, you're thinking about building wealth through real estate? Fantastic. The key that unlocks that door is a property investment loan.

Now, it's easy to think of this as just another mortgage, but that's the first mistake. This isn't finance for your "forever home." It’s strategic business funding designed to help you buy an asset that generates income, grows in value, or ideally, does both.

Unlocking Wealth with a Property Investment Loan

When you buy a home to live in, the bank’s main concern is simple: can your salary cover the repayments? But with an investment loan, the conversation changes entirely. It’s a commercial decision. The lender isn't just looking at your payslips; they're assessing the property's power to earn its keep through rent.

This is a critical distinction. You're not just buying a place to call home; you're acquiring a business asset designed to build your financial future. For thousands of savvy Australians, this is the most powerful and accessible pathway to long-term wealth.

Investment Loan vs Owner-Occupier Loan Key Differences

To really grasp the difference, it helps to see the two loan types side-by-side. While both get you the keys to a property, their purpose and the rules of the game are worlds apart.

| Feature | Property Investment Loan | Owner-Occupier Home Loan |

|---|---|---|

| Primary Goal | Generate income and/or capital growth. It's a business asset. | Provide a primary place of residence. It's a personal asset. |

| Interest Rates | Typically slightly higher due to perceived increased risk. | Generally lower as the property is your primary home. |

| Tax Implications | Loan interest and many property expenses are often tax-deductible. | Loan interest is generally not tax-deductible. |

| Lender Assessment | Focuses on both your income and the property's potential rental income. | Primarily assesses your personal income and ability to repay. |

| Loan Features | Often structured as interest-only to maximise cash flow and tax benefits. | Usually principal and interest repayments to build equity faster. |

Understanding these fundamentals is the first step. One loan is for lifestyle; the other is purely for your balance sheet.

Why Australians Are Turning to Property Investment

The Aussie love affair with property isn't just a cliché; it's a proven wealth creation strategy. And right now, it’s heating up. The September 2025 quarter saw a massive surge, with new investor loans hitting a staggering $39.8 billion—that's a 17.6% jump from the previous quarter.

Investors now account for 40% of all new home loan commitments, a clear sign that people are taking advantage of borrowing conditions and strong rental demand. If you want to dig into the numbers, Broker Pulse's detailed report has a great breakdown.

So, what’s driving this? It boils down to a few powerful motivators:

- Generating Passive Income: The clearest win. A steady stream of rental income that covers the mortgage and bills, often with cash left over for you.

- Capital Growth: This is the long game. Over time, property values tend to rise, building your net worth while you sleep.

- Leveraging Your Capital: An investment loan lets you control a large, valuable asset with a relatively small upfront deposit. It’s about making a small amount of your money do a very big job.

- Tax Advantages: The Australian tax system offers real benefits to investors. Deducting loan interest and other expenses can significantly lower your overall tax bill.

A loan for an owner-occupied home is about finding a place to live. A property investment loan is about making your money work for you. The mindset shift from homeowner to investor is the first and most important step.

Getting this difference right from the start is your foundation for making smart, profitable decisions down the track. Their purpose, assessment rules, and strategic potential are completely different, and this guide will walk you through everything you need to know.

Exploring Different Types of Investment Loans

Choosing the right structure for your investment loan is like picking the right tool for a specific job. You wouldn't use a hammer to saw wood, and the loan you choose needs to align perfectly with your investment strategy. A mismatch can hurt your cash flow, eat into your returns, or slow down your portfolio's growth.

This isn't just a small decision; it has major long-term consequences for your financial outcomes. The market is full of different products, each with its own pros and cons designed for different types of investors. Getting your head around these options is the first step toward making a smart, confident choice.

Principal and Interest vs Interest-Only Loans

One of the first forks in the road you'll come to is how you want to structure your repayments. This choice directly impacts your monthly cash flow and how fast you build equity in your property.

Principal and Interest (P&I) Loans

With a Principal and Interest (P&I) loan, every single repayment you make is split into two parts: the interest charged by the lender, and a small piece of the original loan amount (the principal). Think of it as slowly but surely chipping away at the mountain of debt.

This approach builds your equity faster because you’re reducing what you owe from day one. It's a solid, straightforward strategy favoured by investors who want to own their assets outright sooner.

Interest-Only (IO) Loans

An Interest-Only (IO) loan lets you pay only the interest for a set period, usually one to five years. Because you aren't paying down any of the actual loan balance, your repayments are significantly lower during this time.

This structure is a powerful tool for maximising your cash flow, which you can then reinvest or use to cover other property expenses. It’s a popular strategy for investors aiming to expand their portfolio quickly or who are banking on capital growth for their returns.

Keep in mind that once the interest-only period ends, the loan switches to a P&I structure. Your repayments will jump up significantly because you'll need to pay off the entire principal over a shorter remaining loan term.

Fixed Rate vs Variable Rate Loans

Once you've sorted out your repayment type, the next big decision is about your interest rate. This is all about balancing the need for security against the opportunity for savings.

A variable rate loan means your interest rate can move up or down based on the Reserve Bank of Australia's official cash rate and your lender's own funding costs. This gives you flexibility and the potential for lower repayments if rates fall. The flip side is uncertainty—your repayments will rise if rates go up.

On the other hand, a fixed rate loan locks in your interest rate for a specific period, usually from one to five years. This provides absolute certainty over your repayments, making budgeting a breeze and protecting you from rate hikes. The trade-off is that you won't benefit if rates drop, and these loans often have less flexibility and higher break costs if you want to exit early.

It’s also possible to get a split loan, which combines both fixed and variable parts. This offers a 'best of both worlds' approach—part of your loan is predictable, while the other part can benefit from potential rate cuts.

Which Investment Loan Structure Is Right for You?

Choosing the right loan depends entirely on your goals. Are you chasing maximum cash flow, looking to build equity quickly, or do you just want the certainty of knowing exactly what you'll pay each month? This table breaks it down.

| Investment Goal | Best Loan Structure | Primary Benefit |

|---|---|---|

| Maximum Cash Flow | Interest-Only (IO) Loan | Lower initial repayments free up cash for other investments or expenses. |

| Faster Equity Building | Principal & Interest (P&I) Loan | Reduces the loan balance from day one, building equity more quickly. |

| Budgeting Certainty | Fixed Rate Loan | Repayments are locked in, protecting you from interest rate rises. |

| Flexibility & Potential Savings | Variable Rate Loan | Allows you to take advantage of falling interest rates and often has more features. |

| Balanced Approach | Split Loan (Part Fixed, Part Variable) | Provides a hedge against rate movements with partial certainty and partial flexibility. |

Ultimately, the best structure is the one that fits your personal risk tolerance and supports your long-term property investment plan.

Specialised Investment Finance Options

Beyond the standard loan types, there are specialised products designed for specific investment scenarios. Two of the most common are construction loans and commercial property loans.

- Construction Loans: If you're planning to build a new investment property or do a major renovation, a standard loan won't cut it. A construction loan releases funds in stages (or 'progress payments') as building milestones are hit, so you only pay interest on the money you've actually used.

- Commercial Property Loans: This type of finance is for buying business premises like offices, retail shops, or warehouses. These loans often have different terms, require higher deposits, and involve a more complex assessment focused on the property's commercial viability and any existing lease agreements.

The Australian property market isn't just diverse in its loan offerings; it's also experiencing incredible growth. Australia's residential real estate portfolio has now hit a staggering $12 trillion valuation, doubling in just ten years. Growth is also spreading, with Queensland, Western Australia, and South Australia gaining market share and creating new opportunities for savvy investors. You can dive deeper into these regional trends in the latest Australian property update.

How Lenders Assess Your Application

Getting a 'yes' from a lender on a property investment loan isn't about charm or a good pitch. It’s all about calculated risk. From the bank's perspective, they need total confidence you can handle the loan today, tomorrow, and even if interest rates climb or your tenant moves out.

To figure this out, lenders put your financial profile under the microscope. Think of it like a full financial health check, where they're looking for stability, discipline, and your overall capacity to take on more debt. Knowing what they’re looking for is half the battle won.

The Foundations of Approval

Before the complex calculations begin, every lender starts with the same non-negotiables. These are the absolute pillars of any investment loan application, and nailing them sets you up for success.

Your application really boils down to three key things:

-

Deposit and LVR: Your deposit is your skin in the game. Lenders use the Loan-to-Value Ratio (LVR) to see how much you’re borrowing versus the property’s value. A 20% deposit (meaning an 80% LVR) is the gold standard that helps you dodge Lenders Mortgage Insurance, but some lenders will consider a 10% deposit if the rest of your application is rock-solid.

-

Genuine Savings: Lenders love to see a consistent savings habit over at least three months. It’s not just about the amount; it proves you have financial discipline and can manage your money—a huge green flag that suggests you’ll handle your mortgage repayments just fine.

-

Stable Income: A reliable income stream is non-negotiable. If you’re a PAYG employee, this is pretty straightforward. For self-employed investors, it means gathering more paperwork, but the goal is the same: prove you have consistent cash flow to service the loan.

Calculating Your Borrowing Power

This is where things get a bit more technical. Your borrowing power isn't just a simple multiple of your salary. It's a detailed stress test of your ability to manage all your financial commitments, including the new loan, with a big safety buffer built in.

Lenders will tally up every existing debt you have—credit cards, car loans, HECS, and your own home loan. Then, they’ll run a "stress test," calculating your repayments at an interest rate that’s often 2.5-3% higher than the actual rate you’ll be paying. This ensures you won't default if rates head north.

For an investment loan, how a lender treats potential rent is critical. They don’t count 100% of it. Instead, they "shade" it, meaning they'll only consider around 75-80% of the expected rental income. This buffer accounts for the realities of being a landlord, like vacancies, agent fees, and surprise maintenance costs.

Solutions for Self-Employed Investors

What if you don't have payslips to prove your income? For self-employed Aussies, this is a common hurdle. This is exactly where Low Documentation (Low-Doc) loans come into play, designed specifically for business owners, contractors, and freelancers.

Instead of payslips, you’ll use alternative evidence to prove your income. The most common documents lenders ask for include:

- Business Activity Statements (BAS): Your BAS from the last 6-12 months paints a clear picture of your business's turnover.

- An Accountant's Letter: A signed declaration from your accountant confirming your income is a very powerful tool.

- Business Bank Statements: A few recent statements showing consistent cash flow is often enough to demonstrate stability.

Getting this paperwork organised upfront will make your application much stronger. For a more detailed walkthrough, our guide on how to obtain a home loan dives deeper into the documentation process. Navigating these requirements can feel tricky, but working with a specialist broker means we can match you with a lender who actually understands the realities of running a business.

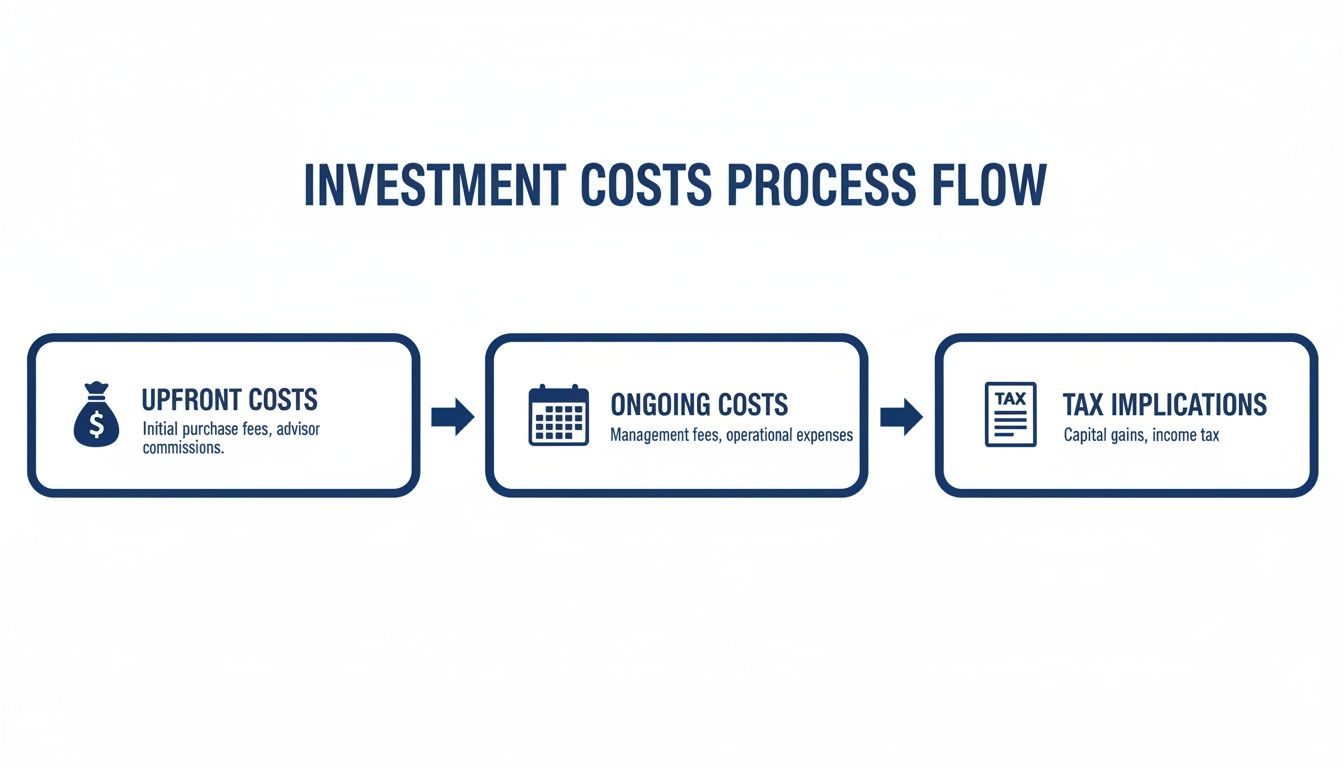

Understanding Your True Investment Costs

A savvy property investor knows to look well beyond the advertised purchase price. That figure is just the starting line, not the finish. Securing a property investment loan gets the deal done, but it’s the real costs of buying and holding the asset that can catch unprepared buyers by surprise.

Think of it like buying a car. The sticker price is one thing, but it’s the fuel, insurance, and ongoing maintenance that really shape your budget. To avoid nasty financial shocks down the road, you need a clear-eyed view of every single expense from day one. These costs fall into three main buckets: the initial cash you need to get the keys, the ongoing expenses to hold the property, and the tax rules that can make or break your long-term returns.

Your Upfront Investment Expenses

Before you can collect a single dollar in rent, you’ll need to cover several significant upfront costs. These are one-off payments needed to finalise the purchase, and they must be factored into your savings plan completely separately from your deposit.

Your major upfront expenses will typically include:

- Stamp Duty: This is a state government tax on property transactions and is often the largest single expense after your deposit. The amount you pay varies wildly depending on which state the property is in and its value.

- Conveyancing and Legal Fees: You’ll need a solicitor or conveyancer to handle the legal heavy lifting of transferring ownership. These fees cover everything from contract reviews and property searches to making sure the settlement process goes off without a hitch.

- Lenders Mortgage Insurance (LMI): If your deposit is less than 20% of the property's value, you will almost certainly have to pay LMI. It's a one-off insurance premium that protects the lender—not you—if you default on the loan.

Ongoing and Hidden Costs

Once the property is yours, the expenses don't stop. These ongoing costs are the lifeblood of your investment, and underestimating them can quickly turn a profitable asset into a financial drain. It’s crucial to budget for these from the get-go.

Beyond your regular loan repayments, remember to account for loan establishment fees or annual package fees your lender might charge. You'll also face council rates, water rates, landlord insurance, and potentially body corporate or strata fees for apartments and townhouses.

And a word of advice? Always set aside a buffer for property management fees and unexpected maintenance. A burst hot water system doesn't wait for a convenient time.

The Tax Landscape: Gearing and Capital Gains

This is where a good strategy can really pay off. Understanding the tax implications of your investment is critical, as the Australian tax system offers specific advantages for property investors, primarily through the concept of "gearing."

Gearing simply describes the relationship between the rental income your property generates and the costs you incur to own it. Your gearing status has a direct impact on your taxable income.

Let's break it down:

- Negative Gearing: This is when your total expenses (like loan interest, council rates, and maintenance) are greater than your rental income. You can then claim this loss as a tax deduction against your personal income, which can result in a significant tax refund. Many investors use this strategy, banking on future capital growth to deliver their main profit.

- Positive Gearing: Your property is positively geared when the rental income is higher than all your deductible expenses. This means the asset generates a profit from day one, which is then added to your taxable income.

- Capital Gains Tax (CGT): When you eventually sell your investment property for more than you paid, that profit is subject to CGT. However, if you hold the asset for more than 12 months, you may be eligible for a 50% discount on the tax you owe. Planning your exit strategy with CGT in mind is absolutely vital.

Grasping these costs is fundamental to building a robust portfolio. In fact, many investors use the value they've built in their existing properties to fund new purchases, a concept you can explore further in our guide on what is equity in property?.

Your Step-By-Step Loan Application Checklist

Getting an investment loan can feel like a huge mountain to climb. But honestly, it’s not. With a bit of organisation, it's more like a series of smaller, manageable hills. A clear plan is your best friend here, ensuring you tick every box without the last-minute panic.

Think of this checklist as your road map, breaking down the entire journey from the "what if?" stage right through to getting the keys.

Phase 1: Strategy and Preparation

Before you even think about talking to a lender, the real work begins. This is where you get your financial ducks in a row and figure out exactly what you want to achieve. Nail this part, and everything that follows becomes so much easier.

-

Define Your Investment Strategy: What's the goal here? Are you hunting for a property that delivers strong rental income (cash flow), or are you playing the long game for capital growth? Your answer shapes the kind of property you'll look for and, just as importantly, the loan structure that will support it.

-

Give Yourself a Financial Health Check: It’s time to get brutally honest with your numbers. Pull together a clear snapshot of your income, expenses, assets, and liabilities. This is also the perfect time to check your credit score. If you spot any errors or old issues, sort them out now—before a lender’s credit assessor does.

-

Gather Your Core Documents: Start collecting the paperwork now to avoid a mad scramble later. You'll need things like your last two payslips, your most recent tax returns and Notices of Assessment, bank statements showing your savings history, and statements for any existing debts like credit cards or a car loan.

Phase 2: Securing Pre-Approval

Think of pre-approval as your golden ticket. It's a conditional nod from a lender for a specific loan amount, which tells sellers and real estate agents you're a serious, qualified buyer. You’re not just window shopping.

Getting pre-approved gives you a firm budget, stopping you from wasting weekends looking at properties you can't afford. It also puts you in the fast lane for final approval once you find the one. In a competitive market, this is a massive advantage.

A pre-approval isn't a rubber stamp, but it’s the most powerful tool an investor has when making an offer. It demonstrates financial readiness and gives you significant bargaining power.

Phase 3: Final Application and Settlement

So, you've found the perfect property and your offer has been accepted. Fantastic. Now it's time to turn that pre-approval into a formal, unconditional approval. The lender will do their final due diligence on both you and the property itself to lock in your investment loan.

The infographic below gives you a great overview of the typical costs you'll encounter along the way.

As you can see, your financial commitments are spread across different stages—upfront, ongoing, and tax-related.

Here’s what happens next:

- Submit the Full Application: You'll give the signed contract of sale to your broker or lender, who will then lodge the formal loan application.

- Property Valuation: The lender will arrange for an independent valuer to inspect the property to make sure it's worth what you're paying for it.

- Formal Approval: Once the valuation comes back clean and your finances are double-checked, the lender issues unconditional (or formal) approval. This is the big green light.

- Loan Documents: The official loan contracts and mortgage documents will be sent to you to sign and return.

- Settlement: On the big day, your legal reps and the lender exchange all the necessary funds and documents. Just like that, the property is officially yours. Congratulations.

Of all the lessons you learn in property investing, the most valuable often come from the mistakes others have made. Getting your property investment loan approved feels like a massive win, but it’s the decisions you make after that moment that will shape your long-term success.

Steering clear of a few common but costly errors can be the difference between a high-performing asset and a constant financial headache.

Too many new investors get tunnel vision, focusing only on the purchase price while completely missing the bigger picture. This kind of oversight can lead to serious financial pain down the track.

Over-Leveraging Your Finances

One of the riskiest moves an investor can make is borrowing right up to their absolute limit. It’s tempting, I get it. Securing the biggest loan possible feels like you’re maximising your opportunity, but it leaves you with zero buffer for the unexpected.

An interest rate hike, an empty property for a few months, or a sudden big repair bill can instantly flip your investment from an asset into a cash-draining nightmare.

The smarter play? Borrow well within your means. You want enough cash in the bank to cover at least six months of mortgage repayments and other running costs. It’s a defensive move that protects both your investment and your sanity.

Underestimating Ongoing Costs

Another classic mistake is building a budget that only covers the mortgage repayment. That’s just one piece of the puzzle. To run a successful investment property, you have to account for all the ongoing expenses, and believe me, they add up fast.

These costs go way beyond the loan itself and must be baked into your cash flow forecasts:

- Council and water rates

- Landlord insurance premiums

- Property management fees

- Body corporate or strata levies (for apartments and townhouses)

- A "sinking fund" for maintenance and repairs

Smart investing isn't just about buying property; it's about running it like a business. A detailed budget that anticipates all expenses is your most important business plan.

Partnering With a Specialist Broker

Trying to navigate all this on your own is a common—and often expensive—mistake. This is where partnering with an expert mortgage broker becomes your single greatest advantage. A specialist broker does more than just find you a loan; we become your strategic partner, helping you sidestep these exact pitfalls.

We give you access to a much wider panel of lenders than you could ever approach on your own, finding lender policies that genuinely align with your investment goals. More importantly, we provide the right advice to help you structure your finances correctly, avoid over-leveraging, and choose a loan product that supports, rather than hinders, your strategy.

Building a sustainable and profitable property portfolio starts with making smart choices from day one. Don't leave your financial future to chance. Book a no-obligation consultation with the Diamond Lending team today, and let's build your success together.

Frequently Asked questions

When you’re diving into the world of property investment, a lot of questions come up. It's completely normal. Getting clear, straightforward answers is the key to moving forward with confidence. Let's tackle some of the most common queries we hear from aspiring investors right across Australia.

How Much Deposit Do I Need for an Investment Property?

The magic number everyone talks about is a 20% deposit, and for good reason—it’s the benchmark for avoiding Lenders Mortgage Insurance (LMI). That said, some lenders are willing to come to the party with investment loans on deposits as low as 10%.

But hold on, that’s not the only cash you’ll need stashed away. You also have to account for the hefty upfront costs like government stamp duty and legal fees. These can easily tack on another 5% of the purchase price to your savings goal, so budgeting for them is non-negotiable.

Can I Use Equity from My Home for a Deposit?

Absolutely, and it’s one of the smartest ways to get your foot in the door of your next investment. This strategy, often called an equity release or cash-out refinance, lets you borrow against the value you’ve painstakingly built up in your own home.

Think of your home equity as a powerful financial resource just sitting there, waiting to be used. A good broker can help you structure the release correctly to maximise what you can borrow and get your investment plans off the ground.

Are Interest Rates Higher for Investment Loans?

Usually, yes, but the gap is often smaller than most people assume. Lenders see a property investment loan as having a slightly higher risk than a loan for the home you live in, so they typically apply a marginally higher interest rate.

The trick is not to just accept the first rate you’re offered. A sharp broker can put dozens of lenders head-to-head to find a seriously competitive rate that suits your financial situation, potentially saving you thousands over the life of the loan.

While the headline rate for an investment loan might be 0.5% to 0.75% higher, remember this crucial fact: the interest you pay is often tax-deductible. This can go a long way in offsetting the extra cost.

What Do I Need for a Low Doc Investment Loan?

Low-doc loans are a game-changer for self-employed investors who don’t have a neat stack of payslips to prove their income. Instead of the usual paperwork, lenders will ask for other ways to verify what you earn.

You’ll typically need to provide some combination of the following:

- Your Business Activity Statements (BAS) from the last 6-12 months

- A formal letter from your accountant confirming your income

- Recent business bank statements that show a consistent flow of cash

Every lender has their own rulebook here, and the requirements can vary wildly. For any self-employed investor, partnering with a broker who lives and breathes low-doc policies is the key to a smooth, successful application.

Ready to build your property portfolio with a loan structured for success? The team at Diamond Lending has the expertise to guide you through every step. Book your complimentary strategy call today.