Think of your home as more than just a place to live. It's a powerful financial asset, and understanding property equity is the key to unlocking its potential.

Simply put, your equity is the portion of your home that you truly own. It's the difference between what your property is worth today and what you still owe on your mortgage.

Your Home as a Financial Scorecard

Imagine your property as a growing savings account. With every mortgage repayment you make, you're tucking away more savings. At the same time, the property market is working in the background, hopefully increasing its overall value.

The calculation itself is straightforward, but the number it reveals is incredibly powerful. It tells you exactly how much of your biggest asset is yours, free and clear.

The Simple Equity Formula:

Current Market Value of Your Property – Outstanding Loan Balance = Your Equity

Let's run a quick example. If your home is currently valued at $900,000 and you have $400,000 left on your loan, your equity is $500,000. This figure is a critical indicator of your financial health and something every homeowner should know.

The Two Engines of Equity Growth

Your equity doesn't grow by accident; two key forces are at play. One is your own disciplined effort, and the other is the broader property market. Both work together to increase your stake in your home over time.

This is why property is often seen as a cornerstone of wealth creation in Australia. You have a direct hand in growing your equity, but you also benefit from market movements.

To make it clearer, here's a simple breakdown of how your equity grows.

| Growth Method | How It Works | Simple Example |

|---|---|---|

| Loan Repayments | Every mortgage payment you make chips away at your debt, which directly increases your ownership stake. | Paying down your $500,000 loan by $20,000 boosts your equity by that same amount. |

| Market Appreciation | Your home's value rises over time due to factors like high demand, location, or home improvements. | A property bought for $750,000 is now valued at $900,000, adding $150,000 to your equity. |

Once you get a handle on this concept, you start to see your property in a new light. It’s not just your home—it’s a flexible financial tool you can use for renovations, investments, or achieving other financial goals.

How to Calculate Your Home Equity in Minutes

Figuring out your home equity is much simpler than most people think. Think of it as a quick financial health check, one that turns an abstract idea into a hard number you can actually use.

First, you need to know the current market value of your home. This isn't what you paid years ago; it's what it would realistically sell for in today's market. You can get a solid estimate from a professional real estate appraisal, a formal bank valuation, or by simply researching recent sales of similar homes in your neighbourhood.

Next, find your outstanding loan balance. This is the exact dollar amount you still owe on your mortgage. You’ll find this on your latest home loan statement or by logging into your online banking portal.

The Equity Calculation in Action

Once you have those two figures, the formula is straightforward. It gives you a clean snapshot of where you stand financially.

Current Market Value – Outstanding Loan Balance = Your Equity

Let’s run through a real-world example. Imagine your home in a Melbourne suburb gets a professional valuation of $950,000. You check your home loan statement and see your remaining mortgage balance is $450,000.

- $950,000 (Market Value) – $450,000 (Loan Balance) = $500,000 (Your Equity)

In this scenario, you’re sitting on an impressive $500,000 in home equity. That’s not just a number on a page—it's a significant asset that represents real wealth you’ve built over time. For a quick estimate, you can play around with some of Diamond Lending's online home loan calculators to explore different scenarios.

Understanding Your Loan-to-Value Ratio

Lenders, however, tend to look at your equity through a different lens called the Loan-to-Value Ratio (LVR). This percentage simply shows how much of your property's value is still financed by a loan. A lower LVR means you own more of your home outright, which makes you a lower-risk borrower in their eyes.

Calculating your LVR is a two-step process:

- Divide your outstanding loan balance by your property's current market value.

- Multiply that result by 100 to get a percentage.

Using our previous example: ($450,000 ÷ $950,000) x 100 = 47.4% LVR. An LVR this low signals strong financial standing and can seriously boost your borrowing power for future investments or projects.

This wealth creation is a cornerstone of financial security for countless Australian homeowners. Recent data shows the total value of residential properties has surged, with the mean price climbing to $1,045,400. When you set that against the average national loan size for owner-occupiers, it highlights a massive equity buildup happening right across the country.

Four Smart Ways to Access Your Home Equity

So, you’ve figured out how much equity you have. That’s the first step. The next is understanding how to put that value to work for you. Your home equity isn’t just a number on a statement; it’s a powerful financial tool you can use to fund renovations, invest, or consolidate debt.

For Aussie homeowners, there are a few well-trodden paths to unlock this wealth. Each strategy has its own pros and cons, and the right one really depends on what you’re trying to achieve. Let's break down the four most common ways to tap into your home's value.

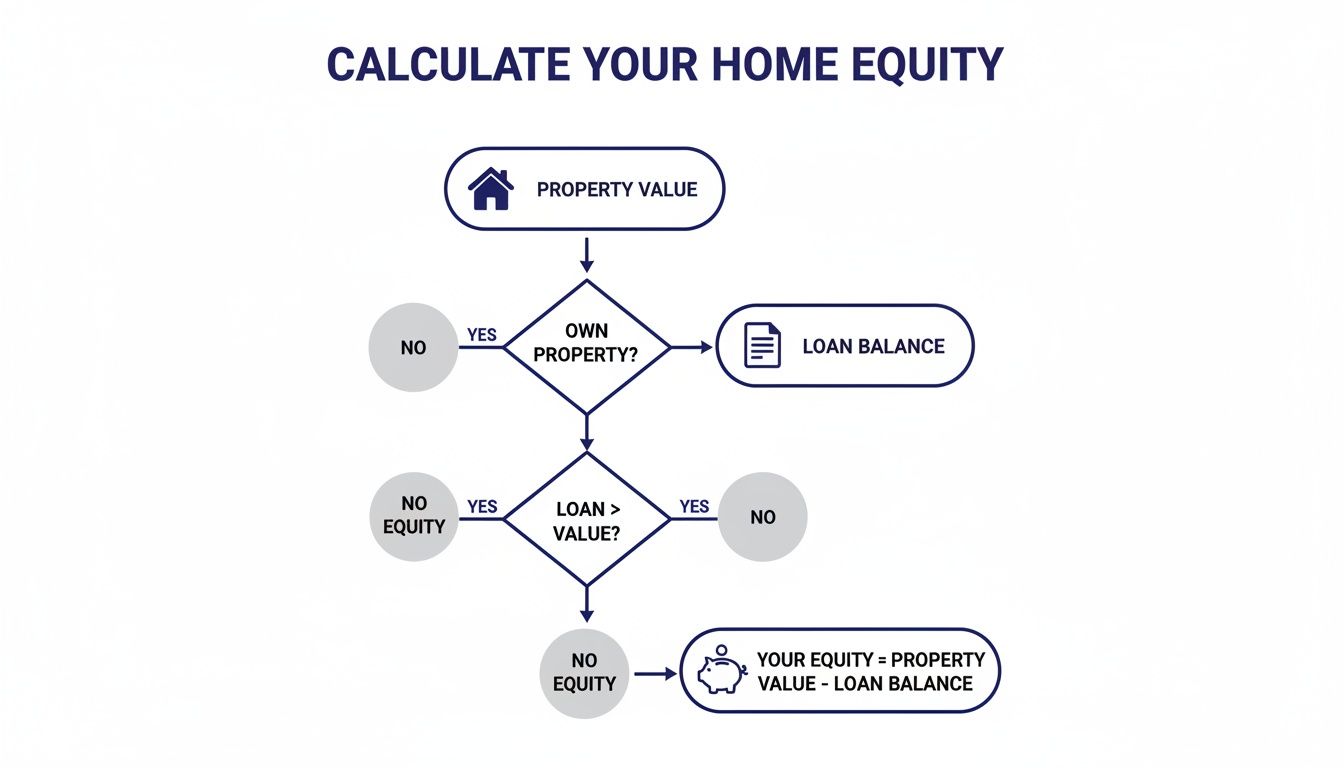

This flowchart shows the simple maths behind working out your equity – the essential starting point for any of these strategies.

As you can see, it's a straightforward calculation: what your property is worth, minus what you still owe the bank.

Cash-Out Refinancing

A cash-out refinance is probably the most popular way to access a big chunk of equity in one go. You’re essentially swapping out your current home loan for a new, larger one. The difference between the two loans is then paid out to you as a tax-free lump sum.

This approach is perfect for large, one-off projects where you know exactly how much cash you need upfront. Think of it as hitting the reset button on your mortgage to unlock a portion of your home’s value for immediate use.

- Best For: Funding a major home renovation, consolidating high-interest debts into a single payment, or coming up with the deposit for an investment property.

- Key Consideration: You’re taking on a brand-new loan, which means a new interest rate and new terms. It's a significant financial move that needs careful thought.

Redraw Facility

Many variable-rate home loans in Australia come with a handy feature called a redraw facility. It lets you access any extra repayments you’ve made on your mortgage over and above your scheduled minimums. In simple terms, you’re just pulling back the money you’ve already paid ahead of time.

It’s a simple, often fee-free way to get your hands on smaller amounts of cash for unexpected expenses or opportunities. The only catch is that it’s only an option if you’ve been disciplined enough to make those extra payments.

Home Equity Line of Credit (HELOC)

A Home Equity Line of Credit (HELOC) works a bit like a high-limit credit card that’s secured against your home. Instead of a single lump sum, you get a revolving credit line you can draw on, repay, and draw on again as you need.

The flexibility here is incredible because you only pay interest on the money you actually use. Historically, these equity gains have empowered countless homeowners. For more details, you can explore the latest data on dwelling values from the Australian Bureau of Statistics.

A HELOC is a fantastic tool for managing unpredictable cash flow, such as for a small business owner, or for funding a project that will be completed in stages, like a multi-phase renovation.

Equity Release and Private Lending

For more complex or time-sensitive situations, equity release through private lenders can be a game-changer. This path is often used by savvy investors or property developers who need short-term funding, like a bridging loan to snap up a new property before their old one sells.

While private lending usually comes with higher interest rates and fees, it offers a level of speed and flexibility that traditional banks just can't match. This makes it an invaluable tool for very specific investment scenarios where timing is everything.

Comparing Equity Access Methods

Choosing the right way to access your equity can feel overwhelming. This table breaks down the four main options to help you see which one might be the best fit for your goals.

| Method | Best For | Key Consideration | Flexibility |

|---|---|---|---|

| Cash-Out Refinance | Large, one-off expenses like renovations or an investment deposit. | Involves creating a new loan with new rates and terms. | Low |

| Redraw Facility | Smaller, unexpected costs. Quick and easy access to your extra repayments. | Only available if you've made extra payments on your loan. | Moderate |

| HELOC | Ongoing projects or managing fluctuating cash flow, like for a business. | You only pay interest on the amount you use, but rates can be variable. | High |

| Equity Release/Private Lending | Urgent, short-term needs like bridging finance or property development. | Higher rates and fees, but offers unmatched speed and flexibility. | Very High |

Each method serves a different purpose. A cash-out refi gives you a lump sum for a big project, while a HELOC offers ongoing flexibility. A redraw is great for tapping into your own hard-earned extra payments, and private lending is the go-to for speed and certainty. The best choice is the one that aligns with your financial strategy.

Navigating the Risks of Using Property Equity

Tapping into your home equity can feel like unlocking a secret weapon to fund investments or big life goals, but it’s something to be treated with serious respect. It’s not like dipping into a savings account; you’re taking on more debt. Because of that, it's crucial to understand what you're getting into before making a move.

The most immediate change is that your total loan amount goes up. This usually means higher monthly repayments, which can add real strain to your household budget, especially if your job situation changes or unexpected costs pop up. An interest rate rise could also make those new, larger repayments much harder to manage.

The Danger of Negative Equity

One of the biggest risks when you borrow against your home is the potential to fall into negative equity. This is a tough spot where your property's market value drops below the total amount you owe on your mortgage.

Let's imagine your home is valued at $800,000 and you have a $500,000 loan. You decide to access an extra $100,000 of equity, bringing your total debt to $600,000. If a market downturn hits and your property's value falls to $580,000, you suddenly owe more than your home is worth.

Being in negative equity makes it extremely difficult to sell your property without taking a financial hit. It can also trap you, limiting your ability to refinance until the market bounces back and your home’s value recovers.

While the Australian property market has proven resilient over the long haul, downturns can and do happen. We're seeing ongoing affordability challenges where property prices often grow faster than incomes. At the same time, rising property values—often driven by a shortage of homes for sale—continue to build equity for many homeowners, creating a buffer against economic shifts. You can read more about the latest housing system trends to get a better feel for these market dynamics.

Understanding the Associated Costs

Accessing your equity isn't free. A common mistake is treating it like a risk-free pile of cash, but that can be a costly assumption once you factor in the expenses.

When you apply to release equity, whether through a refinance or a new loan, you’ll likely run into several upfront fees. These can include:

- Application Fees: What the lender charges just to process your new loan application.

- Valuation Fees: The cost to have a professional valuer confirm your property's current market worth.

- Government Charges: These are state-based fees for registering and deregistering the mortgage on your property title.

- Lenders Mortgage Insurance (LMI): This is a big one. If accessing equity pushes your Loan-to-Value Ratio (LVR) above 80%, you will almost certainly have to pay LMI. This insurance protects the lender, not you, and can add thousands of dollars to your loan.

Being clear-eyed about these risks—from negative equity to the different fees involved—is what allows you to make a smart, informed decision about how and when to use the wealth you’ve built in your property.

How the Property Market Shapes Your Equity

Your home equity isn’t a fixed number; it’s constantly on the move, shifting with the pulse of the Australian property market. Think of it like a boat on the ocean—market waves can lift it higher or cause it to dip. Understanding these outside forces is crucial when you’re figuring out how to make your equity work for you.

When the market is ‘hot’, strong buyer demand and a shortage of homes for sale can send your property's value soaring. This market appreciation can build your equity in a big way, often without you lifting a finger or making a single extra repayment. You’re essentially gaining wealth just by owning property in the right place at the right time.

We’ve seen this play out clearly in recent Australian market trends. Take September 2025, for example, when the Cotality Home Value Index shot up 0.8% nationally. That was its biggest monthly jump since October 2023. A key driver was the record-low number of listings in major areas—down a massive 53% in Darwin and 45% in Perth. This created intense competition among buyers and gave homeowners a serious equity boost. You can learn more about how low listings impact property values by reading the full report.

When the Market Cools Down

On the flip side, a cooling market can pull your equity in the opposite direction. Things like rising interest rates or a wider economic slowdown can reduce buyer demand, which might mean slower price growth or even a drop in property values.

In these conditions, your equity might stall or even shrink, even as you diligently keep paying down your mortgage. This is why it’s so important to see your equity not as a static number, but as a living asset that’s tied to powerful market cycles.

This direct link between the market and your personal wealth is why timing is everything. Knowing when the market is strong helps you pick the right moment to tap into your equity for an investment. And understanding the risks in a downturn helps you protect the value you've worked so hard to build.

Your Next Steps with Diamond Lending

So, you've got a handle on what property equity is and how it works. That's the first step. Now, let's look at how you can put this powerful asset to work to achieve your financial goals. Whether you’re planning a major renovation, looking to buy an investment property, or just want to get your other debts under control, your equity is one of the most valuable resources you have.

The best way to explore your options is to have a chat with a Diamond Lending broker. We can help you figure out exactly how much equity you can access and map out the right strategy for your unique situation.

When Should You Talk to a Broker?

It's a smart move to bring in an expert when you're about to make a significant financial decision. We specialise in helping clients navigate these key moments.

- Planning a Renovation: Ready to upgrade your home? We can help you structure the right loan to fund the entire project, from start to finish.

- Investing in Property: This is a classic move. You can use the equity in your current home as the deposit for your next investment property.

- Debt Consolidation: Want to simplify your finances? We can help you roll high-interest credit cards into your home loan, often at a much lower rate.

Guidance for Unique Circumstances

For self-employed people or anyone with a few bumps in their credit history, having a strong equity position can be a complete game-changer. It shows financial stability and can open doors to lending solutions that might otherwise be out of reach. We excel at finding pathways for clients in these situations, including specialised private lending options for unique scenarios.

We're also seeing a big shift in Australia's property market right now. Investors are getting creative, using their equity to fuel all sorts of strategies—from diversifying into new property types to buying interstate in high-growth lifestyle regions. For more on this, the State of the Housing System 2025 report offers some fantastic insights into how investors are leveraging equity in the current climate.

To get started, we'll usually just need a few key documents:

- Proof of income (like payslips or your BAS if you're self-employed)

- Recent statements for your current home loan

- Your identification documents

Reach out to Diamond Lending today for a no-obligation chat about where you want to go next.

Common Questions About Property Equity

Getting your head around property equity can bring up a few questions. To help you feel more confident about your position, we’ve put together some straightforward answers to the queries we hear most often from homeowners.

How Much Equity Can I Actually Access?

In Australia, most lenders are comfortable letting you borrow up to 80% of your property's value (an 80% LVR) without needing to pay for Lenders Mortgage Insurance (LMI).

Your accessible equity is the difference between this 80% mark and what you still owe on your loan.

Let's break it down. Say your home is valued at $1,000,000 and you have $400,000 left on your mortgage. A lender will typically let you borrow up to $800,000 (80% of the value). To find your accessible equity, you just subtract your loan balance from that figure: $800,000 – $400,000 = $400,000. That's the amount you could potentially tap into. While some lenders might go higher, it almost always means paying for LMI.

Does Making Extra Mortgage Repayments Build Equity Faster?

Absolutely. Every extra dollar you put into your home loan goes straight to the principal, reducing your debt and instantly boosting your equity. It’s one of the most direct and effective ways to build your ownership stake in your property.

This strategy doesn't just grow your equity; it also slashes the total interest you'll pay over the life of the loan. Think of it as a double win—you own more of your home sooner and save a heap of money in the long run.

Is It Possible to Lose My Property Equity?

Yes, it's possible. Your equity isn't set in stone because it's tied to your property's market value. If the market takes a significant dip, your home's value could fall to a point where it’s worth less than what you owe the bank. This situation is called negative equity.

While the Australian property market has shown incredible resilience over the long term, short-term fluctuations are always a reality. This is a critical risk to consider before you decide to borrow against your home.

What Is the Difference Between Usable and Total Equity?

These terms get thrown around a lot, and while they sound similar, there’s a key difference. Total equity is the simple, top-line figure: your property's current market value minus your outstanding loan balance.

Usable equity (or accessible equity) is the portion of that total a lender will actually let you borrow against. Banks hold back a buffer—usually 20% of your property’s value—to protect themselves against a potential drop in the market. So, even if you have $500,000 in total equity, a lender might only consider around $300,000 of it as usable for a new loan.

Ready to explore what your property equity can do for you? The team at Diamond Lending is here to provide expert guidance and find the right strategy for your financial goals. Start a conversation with us today.

Article created using Outrank