When you're mapping out the budget for your new home, the purchase price and your deposit are naturally front and centre. But there's another major cost that often catches people by surprise: stamp duty.

Think of it as a mandatory state government tax you pay for the privilege of transferring a property's legal title into your name. In Victoria, it's officially called 'land transfer duty', and overlooking it can be a costly mistake.

Your Guide To Understanding Victorian Stamp Duty

This isn't just a small administrative fee. For many buyers, stamp duty is one of the biggest single expenses they'll face outside of their deposit, often running into the tens of thousands of dollars.

Getting your head around what stamp duty is in Victoria is the first critical step towards a smooth property purchase. While it might feel like just another tax, the revenue collected from it helps fund essential public services that we all rely on, including:

- Hospitals and our healthcare system

- Public schools and education

- Emergency services and vital transport infrastructure

Why This Tax Matters To You

The amount of stamp duty you'll owe is tied directly to the value of the property you're buying. It's a sliding scale—the higher the purchase price, the more duty you'll pay. This cost has a real impact on the total funds you need to have ready for settlement and can even affect your borrowing power with lenders.

For most homebuyers, stamp duty is a significant financial hurdle. Factoring it in from day one gives you a realistic budget and helps you avoid that last-minute scramble for funds during the stressful settlement period.

This guide is here to demystify it all. We’ll break down exactly how the tax is calculated, walk through the crucial concessions that could save you thousands, and clarify when it needs to be paid. Navigating the rules can feel complex, but with the right knowledge, you can tackle your property purchase with total confidence. Let's get started.

How Victorian Stamp Duty Is Calculated

So, how do they actually land on that final stamp duty figure? It’s not a simple flat fee. Instead, the calculation for stamp duty in Victoria comes down to two key things: the property's value and a set of progressive tax brackets. The whole system is designed so the percentage you pay climbs as the property's value goes up.

The starting point is what’s known as the property's dutiable value. Now, this isn't always the price you shook hands on. The State Revenue Office (SRO) will use whichever is higher: the purchase price or the property's current market value. This is to make sure the tax is based on the property's true worth at the time of the sale.

Let's say you buy a house from a family member for a friendly price of $700,000, but an independent valuation confirms it's actually worth $800,000 on the open market. In this case, the stamp duty will be calculated on the $800,000 figure. It’s a crucial detail that can significantly bump up your final costs if you're not prepared for it.

Understanding The Progressive Rate System

Victoria’s stamp duty system works on a sliding scale. Think of it like income tax brackets—you pay different rates for different portions of the property's value. This means a more expensive property naturally attracts a higher overall rate of tax, making it a major line item in your budget, especially in pricier markets.

The rates are set up to increase the tax as property values rise. For instance, for properties valued up to $130,000, the rate is relatively gentle. But once a property’s value crosses that $130,000 mark, the rate jumps significantly. For high-end properties that go over the $2 million mark, Victoria applies a premium rate, making it one of the more expensive states for big-ticket property deals.

Victorian Stamp Duty Rates And Thresholds

To give you a clearer picture, let's break down the specific rates and thresholds for residential properties. The table below shows exactly how the stamp duty is structured based on the property's dutiable value.

| Dutiable Value Range | Rate Of Duty |

|---|---|

| $0 – $25,000 | 1.4% of the dutiable value |

| $25,001 – $130,000 | $350 + 2.4% of the dutiable value over $25,000 |

| $130,001 – $960,000 | $2,870 + 6% of the dutiable value over $130,000 |

| $960,001 – $2,000,000 | 5.5% of the dutiable value |

| Over $2,000,000 | $110,000 + 6.5% of the dutiable value over $2,000,000 |

As you can see, it's not a simple one-size-fits-all percentage. It's a mix of a base amount plus a percentage applied to the value within that specific bracket. To get an exact number for your situation without the headache, it's best to use our simple stamp duty calculator for Victorian properties.

Additional Factors That Change The Calculation

The final stamp duty bill isn't just about the property's price tag. A few other factors can come into play and really change the final number you have to pay. It’s vital to know where you stand, as these can either add to your costs or give you some welcome relief.

Key variables include:

- Your Residency Status: Foreign purchasers get hit with an extra 8% foreign purchaser additional duty (FPAD). This is on top of the standard stamp duty, which can massively inflate the total tax for non-resident buyers.

- Property Type and Use: The numbers can look different depending on whether you're buying your own home (Principal Place of Residence), an investment property, or a commercial site. Some of the best concessions, which we'll cover next, are only available if you plan to live in the property.

- Your Buyer Profile: Are you a first-home buyer? This is the big one. You could be eligible for a huge discount or even a full exemption, completely wiping out your stamp duty bill.

Understanding these nuances is key to accurately budgeting for your property purchase. What seems like a straightforward calculation can quickly become more complex once your specific circumstances are applied.

For example, two people buying identically priced homes could end up with wildly different stamp duty bills. One might be a first-home buyer living in the property and pay next to nothing, while the other could be a foreign investor facing a much heavier tax bill. It’s these distinctions that really matter when looking at the concessions and exemptions available.

Key Stamp Duty Concessions And Exemptions

Navigating the cost of stamp duty can feel like a huge hurdle, but this is where some serious relief comes into play. The Victorian government offers several concessions and exemptions designed to take the financial pressure off certain property buyers. Getting your head around these opportunities is a must—they could literally save you tens of thousands of dollars.

These savings aren’t just handed out, though. You need to meet specific criteria and make sure you apply for them. The biggest discounts are almost always aimed at first-home buyers and people purchasing a home to actually live in, making it that much easier to get a foot on the property ladder.

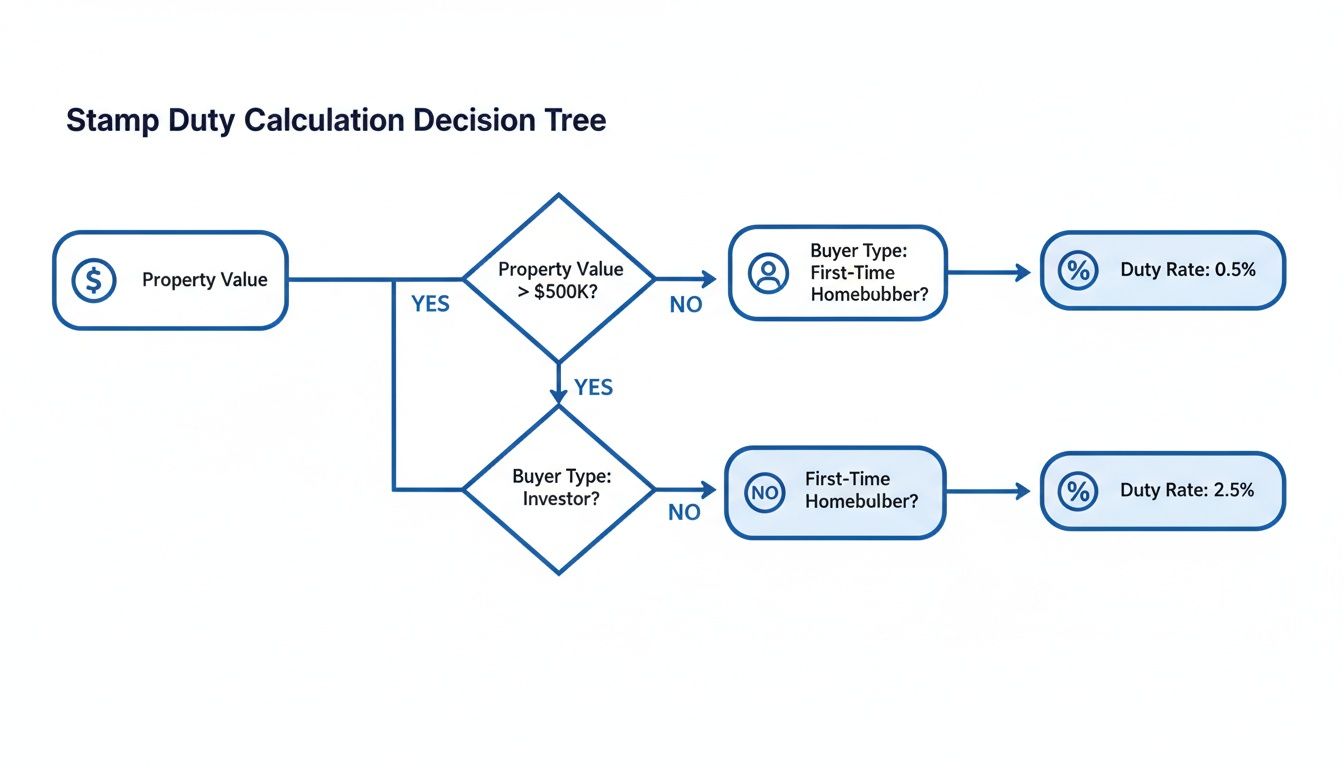

This decision tree shows how your property's value and your buyer profile are the first two questions that decide your stamp duty outcome.

The main takeaway here is that your stamp duty journey starts with these simple questions, but they lead to vastly different financial results.

The First Home Buyer Advantage

For anyone stepping into the property market for the first time, the First Home Buyer Duty Exemption or Concession is pure gold. It's a genuine game-changer that can dramatically slash the upfront cost of buying your home.

If you're an eligible first-home buyer and your property is valued at $600,000 or less, you could be looking at a full exemption. That means you pay $0 in stamp duty. It's a massive saving you can put straight towards your deposit or other buying costs.

What if your first home is valued between $600,001 and $750,000? You might still qualify for a concession. This works on a sliding scale, so the closer your property's value is to the $600,000 mark, the bigger your discount will be.

To grab this fantastic opportunity, you'll need to tick a few boxes:

- New or Established Home: The savings apply whether you're buying a brand-new build or an existing home.

- Buyer Status: You (and your spouse/partner, if you have one) must never have owned residential property anywhere in Australia before.

- Residency Requirement: At least one of the buyers has to move into the property and live there as their main home for a continuous 12-month period, starting within 12 months of settlement.

Principal Place Of Residence Concession

Even if you're not a first-home buyer, there are still savings to be had. The Principal Place of Residence (PPR) Concession is available to anyone buying a home they plan to live in, as long as the property value is no more than $550,000.

Just like the first home buyer benefit, this one requires you to move in within 12 months of settlement and live there for at least a year. It’s the government’s way of making housing more affordable for owner-occupiers compared to investors.

Understanding the difference between an owner-occupier and an investor is crucial. The most generous government concessions are almost always reserved for those buying a home to live in, not to rent out.

Off-The-Plan Duty Concession

Buying a property before it’s even built—known as "off-the-plan"—comes with its own unique stamp duty advantage. The Off-the-Plan Duty Concession means you pay duty on the value of the property when you sign the contract, which is often a lot less than what it's worth once construction is finished.

This concession works by subtracting the construction costs incurred after the contract date from the property's dutiable value. It's available for all property types, but the deal is much sweeter if the property is going to be your main home.

Key perks of the off-the-plan concession include:

- Reduced Dutiable Value: You’re taxed on the land and pre-construction value, not the fully finished home.

- Combined Savings: You can often stack this with other discounts, like the First Home Buyer or PPR concessions, to maximise your savings.

This makes buying a new apartment or townhouse a really attractive option for anyone looking to keep those upfront government charges as low as possible.

Other Important Exemptions

Beyond the major concessions, there are a few other exemptions that apply to specific life events. It's vital to know about these, as they can completely wipe out the need to pay stamp duty on certain property transfers.

- Spouse or Partner Transfers: Moving ownership of a property between spouses or domestic partners is generally exempt from stamp duty, but only if it's their shared home. This is common during relationship changes or for estate planning.

- Breakdown of a Relationship: Property transfers that happen because of a divorce or the end of a de facto relationship are also exempt from duty.

- Deceased Estates: If you inherit a property through a will, you typically don't have to pay stamp duty on that transfer.

Each of these situations is governed by specific rules from the State Revenue Office (SRO). It's always a smart move to get professional advice from your conveyancer to make sure you meet all the requirements and correctly claim any exemption you're entitled to.

Real-World Stamp Duty Calculation Examples

Theory is one thing, but seeing the numbers in action is where it all clicks. Let's walk through three common buyer scenarios in Victoria to see just how dramatically the final stamp duty bill can change.

These examples put the rates and concessions into a real-world context, showing you the tangible impact your situation has on the tax you'll pay. By crunching the numbers, you'll get a much better feel for what stamp duty in Victoria looks like for your budget.

Example 1: The First-Home Buyer

Meet Olivia. She’s ready to buy her first apartment for $650,000 and plans to live in it as her principal place of residence (PPR).

Because her property falls between the $600,001 and $750,000 bracket, she’s eligible for the First Home Buyer Duty Concession. Without it, she’d be facing a huge bill of $34,070.

- Property Price: $650,000

- Buyer Type: First-Home Buyer (concession eligible)

- Standard Duty (without concession): $34,070

- Concession Applied: A tapered reduction based on the sliding scale.

- Final Stamp Duty Payable: Roughly $11,357

That single concession just saved Olivia an incredible $22,713. This is a perfect example of why knowing your entitlements is non-negotiable for first-home buyers. That saving is a massive boost to a deposit or can easily cover all her moving costs.

Example 2: The Second-Home Buyer (Upgrader)

Now for Ben and Sarah. They're selling their current home to upgrade to a larger family house for $900,000. They're not first-home buyers, but since they'll live in the new property, they are classified as owner-occupiers.

With no first-home buyer benefits available, they're up for the full rate of stamp duty.

- Property Price: $900,000

- Buyer Type: Owner-Occupier (upgrading)

- Calculation: The duty is based on the standard Victorian rates for this value.

- Final Stamp Duty Payable: $49,070

This figure shows just how significant stamp duty is for those moving up the property ladder. It’s a major upfront cost that has to be factored into the total purchase budget.

Example 3: The Property Investor

Finally, let's look at David, who is buying a rental apartment for $700,000. As an investor, he has no intention of living there, which means he isn't eligible for the key concessions that owner-occupiers or first-home buyers can access.

He will pay the full, standard rate of land transfer duty.

- Property Price: $700,000

- Buyer Type: Investor

- Eligibility: No major concessions apply.

- Final Stamp Duty Payable: $37,070

These scenarios highlight a key point: two people buying properties at similar prices can end up with vastly different tax bills. An investor at $700,000 pays the full amount, while a first-home buyer at $650,000 pays only a fraction of the standard rate thanks to a concession.

Not sure how your own numbers stack up? The easiest way to get a precise estimate is to use a reliable stamp duty calculator for Australia. It takes the guesswork out of budgeting and gives you a clear figure to work with.

Paying Your Stamp Duty: What You Need to Know

Knowing how much stamp duty you owe is one thing, but understanding when and how to pay it is just as crucial. The payment process is a key step in finalising your property purchase, and getting the timing wrong can lead to stressful delays on settlement day. The good news is, it's a well-trodden path, and you won't be navigating it alone.

Timing is everything. In Victoria, your stamp duty is generally due within 30 days of your property's settlement date. This isn’t the day you sign the contract of sale, but the official date the property title legally transfers to your name. This 30-day window gives you a clear deadline to get your funds sorted.

Your Conveyancer or Solicitor Does the Heavy Lifting

Thankfully, you're not expected to handle the complex paperwork and transfer funds to the State Revenue Office (SRO) by yourself. This is where your conveyancer or solicitor becomes your best friend, stepping in to manage the entire process for you. They act as the essential link between you, your lender, and the SRO.

Your legal eagle will:

- Calculate the exact duty payable, making sure to include any concessions or exemptions you're entitled to.

- Prepare and lodge all the necessary documents with the SRO to get the property transfer registered.

- Arrange the payment of the stamp duty from the funds made available at settlement.

They ensure everything is done correctly and on time, which is vital for a smooth settlement. Think of them as the project manager for your property's legal and financial handover.

How Stamp Duty Affects Your Home Loan

Stamp duty isn't just another cost to add to the list; it's directly tied to your home loan application and how much you can borrow. Lenders need to see that you have enough cash to cover not only your deposit but all the other costs that come with buying a home.

Lenders won't give your home loan the final green light until they see proof of "sufficient funds to complete." This means you must show you have the deposit, the stamp duty, and other fees like conveyancing and registration costs ready to go.

This is exactly why it’s so important to budget for what is stamp duty in Victoria right from the very beginning. Let's say you've saved a $100,000 deposit for an $800,000 house but completely forgot about the $43,070 stamp duty bill. You'll suddenly find yourself with a major financial shortfall, putting your entire loan approval at risk.

By factoring this tax into your savings goals from day one, you show lenders you’re a well-prepared and low-risk borrower, making your path to approval a whole lot smoother.

Upcoming Changes To Commercial Property Stamp Duty

While this guide has mostly covered residential property, a huge shift is on the horizon for commercial and industrial properties that every investor and business owner needs to watch.

The Victorian Government is kicking off a major reform designed to get rid of the hefty, upfront cost of stamp duty for these kinds of properties. It’s a game-changer.

The new system starts on 1 July 2024. From that date, when a commercial or industrial property is sold, stamp duty will be paid one last time. After that sale, the property moves into a completely new tax system, wiping out the stamp duty burden for all future owners.

So, what replaces it? Instead of that single massive payment, the property will now be subject to an annual Commercial and Industrial Property Tax (CIPT). This yearly tax is a simple, flat rate of 1% of the property's unimproved land value.

What This Reform Means For Buyers

The big idea behind this change is to make it easier for businesses to buy their own premises or move locations without being hit by a massive tax bill right at the start. Taking stamp duty out of the equation is meant to free up capital, letting businesses pour more money into their operations, new equipment, or hiring more staff.

This reform completely changes the financial sums for commercial property investment in Victoria. It moves the tax burden from a huge, one-off payment when you buy, to a smaller, predictable annual cost you can budget for.

For buyers, this means the barrier to entry is much lower. Of course, it also adds a new ongoing expense to factor into your annual costs. To help businesses handle that final stamp duty payment before a property switches over to the CIPT system, the government is offering a transition loan. This lets you pay off that final stamp duty bill over 10 years with a government-backed loan.

The impact is already being felt. The reform is expected to significantly cut stamp duty obligations between 2025-26 and 2028-29. In fact, over 3,700 properties have already transitioned to the new annual tax model, meaning their future stamp duty costs are gone for good.

You can find out more about how the state government is transitioning from upfront charges to an annual property tax on the Victorian Budget website.

How Expert Guidance Simplifies Your Property Purchase

Trying to get your head around stamp duty in Victoria can feel like a huge, and often expensive, hurdle on your property journey. While it's important to understand the rules, rates, and concessions, you absolutely don't have to figure it all out alone. This is exactly where professional guidance turns a confusing process into a clear, manageable plan.

A good mortgage broker acts as your strategic partner, making sure every potential cost is factored into your financial picture right from the start. They do more than just find you a home loan; they help you build a complete and realistic budget that accounts for all those upfront expenses, including the full stamp duty amount.

Your Advocate For Savings And Clarity

For first-home buyers, this kind of support is invaluable. An expert broker will meticulously check your eligibility for every available saving, from the First Home Buyer Duty Exemption to the Principal Place of Residence (PPR) Concession. They ensure no opportunity to lower your costs is missed, potentially saving you thousands of dollars that can go straight back into your deposit or cover other settlement fees.

This guidance is just as crucial for property investors. A broker can help you structure your finances for the best possible outcome, making sure your investment strategy lines up with your long-term financial goals. They bring clarity to how stamp duty impacts your overall purchasing power and cash flow.

Partnering with a mortgage broker removes the guesswork. Instead of worrying if you've budgeted correctly for stamp duty, you get the confidence that comes from having a clear, expert-verified financial roadmap for your property purchase.

From Initial Estimates To Final Settlement

The path to property ownership gets a lot simpler when you have the right tools and support. It all starts with getting a reliable estimate of your costs, which is why accessible online calculators are so important for that initial planning phase. From there, expert advice ensures your chosen loan structure can comfortably cover all the settlement costs, preventing any nasty last-minute surprises.

Ultimately, understanding what stamp duty is in Victoria is the first step, but applying that knowledge effectively is what makes for a smooth and successful purchase. A quick chat with a professional can set you on the right path, giving you the clarity and confidence you need to move forward. This strategic partnership helps turn a complex financial obligation into just another straightforward part of your exciting home-buying adventure. 🏠

Ready to purchase your property with a clear financial plan? The team at Diamond Lending is here to guide you through every step, ensuring you understand all your costs and maximise your savings. Book a quick, no-obligation chat with our experts today!