Got a blueprint and a block of land? A standard home loan isn't going to cut it. Building development loans are a specialised form of finance engineered to fund the entire lifecycle of a property development project, from buying the site right through to completing construction.

This isn't just a mortgage for a new build; it's the financial engine designed to turn architectural plans into a physical, profitable asset, whether that's a duplex, a row of townhouses, or a multi-storey apartment complex.

Unpacking Building Development Loans

Think of a building development loan as the lifeblood of your project. It supplies the critical capital needed to navigate the complex journey from an empty lot to a finished, marketable property. The real difference lies in how it handles cash flow, which is totally unique to the construction world.

Instead of getting a single lump sum, funds are released in stages, known as drawdowns. These payments are directly tied to hitting key construction milestones—like the slab being poured or the frame going up. This structure protects everyone involved; the lender knows their money is funding real progress, and you only pay interest on the funds you’ve actually used.

What Does This Funding Cover?

A well-structured building development loan is designed to cover the full spectrum of project costs, giving developers the financial backing they need at every critical phase. It goes way beyond just the bricks and mortar.

- Land Acquisition: The initial purchase of the development site.

- Soft Costs: All the professional and council fees, including architects, engineers, surveyors, and Development Application (DA) lodgement fees.

- Hard Costs: The nuts and bolts of the build—all physical construction expenses like materials, labour, and site preparation.

- Contingency: A crucial buffer set aside to cover unexpected costs or delays, which is typically around 10-15% of the total build cost.

This specialised approach provides the necessary capital to transform an idea into a tangible asset. It empowers developers, builders, and investors to seize opportunities and bring new housing to the market. Mastering this type of finance is essential for success.

Market Demand and Project Viability

The relentless demand for new housing continues to fuel the need for effective development finance. In the 12 months leading up to March, Australia saw a staggering 91,790 loans issued for new housing construction or purchase. That’s an 8.5% increase from the previous year.

What's really driving this is investors, who accounted for a significant 14.1% rise in these loans. You can read more about this housing finance momentum and its market impact.

This robust activity shows exactly why understanding building development loans is so crucial for anyone looking to build. In today's dynamic and competitive market, it’s the key financial tool that enables projects to move from concept to completion.

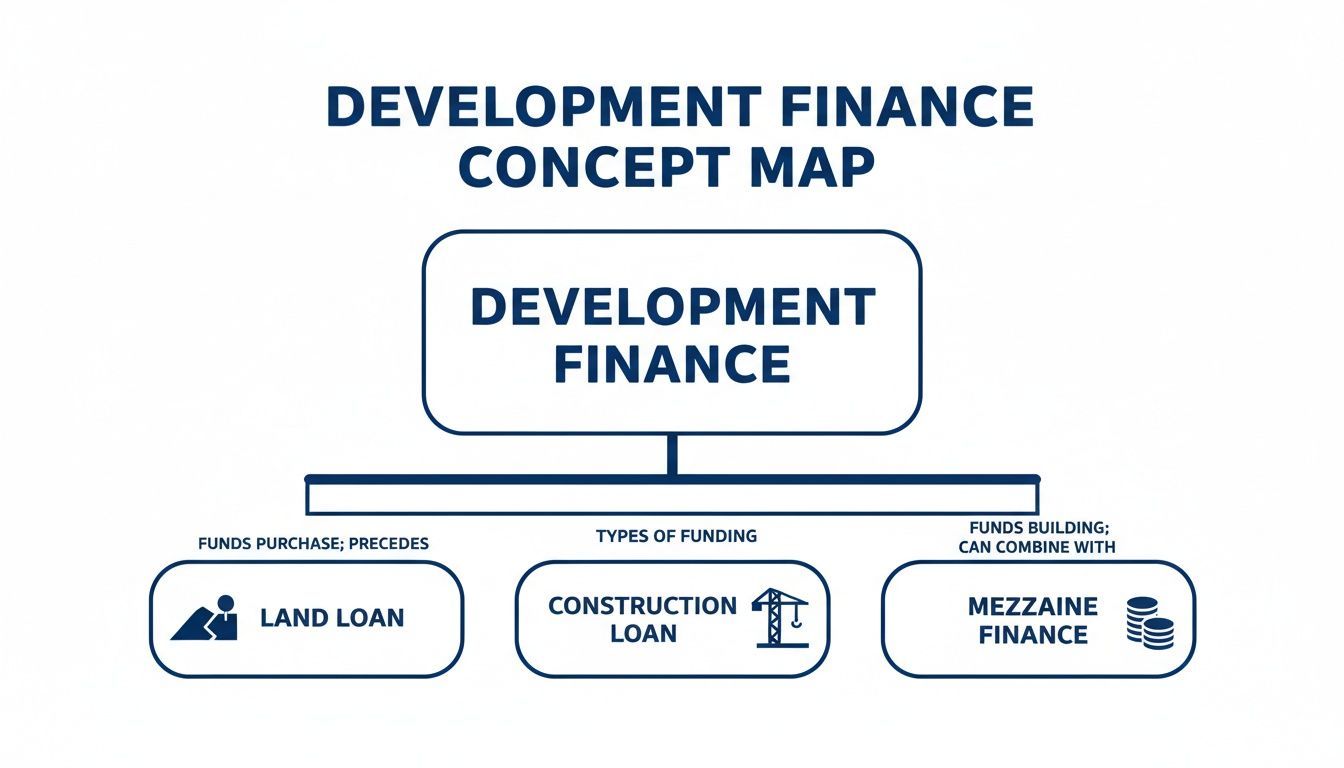

What Are the Different Types of Development Finance?

Not all development loans are cut from the same cloth. Just like a builder needs different tools for framing, plumbing, and finishing, a developer needs a flexible financial toolkit to get a project over the line. Matching the right type of finance to your project’s scale and stage is what separates a smooth build from a stressful one.

Knowing how these different funding structures work allows you to build a powerful and flexible financial stack. Let's walk through the main tools in a developer's financial arsenal.

Land Loans: Securing Your Site

Before a single foundation can be poured, you need the land. A Land Loan is the very first piece of the puzzle, giving you the capital to purchase the development site itself. These loans are unique because they finance an asset that doesn’t generate any income… yet.

Lenders see raw, undeveloped land as a higher-risk play than an established property. Because of this, you can expect them to ask for a larger deposit or apply stricter criteria compared to other loan types. The goal here is simple: secure the site so you can move forward with planning, approvals, and getting ready for the build.

Construction Loans: Funding the Build

Once you own the land and have your plans approved, the Construction Loan takes centre stage. This is the workhorse of development finance, designed to cover all the "hard costs" of the actual build—from excavation and materials to labour and landscaping.

Its key feature is the staged drawdown process. Instead of handing over a lump sum, the lender releases funds in agreed-upon stages that line up with key construction milestones. For example, payments are made after the slab is poured, the frame goes up, or the property reaches lock-up stage.

This structure is smart for two reasons:

- It keeps interest costs down, as you only pay interest on the money you’ve actually used, not the total loan amount from day one.

- It provides oversight. A quantity surveyor usually signs off on the work before the next payment is released, ensuring everything is on track and built to standard.

Mezzanine Finance: Bridging the Equity Gap

Often, the amount a senior lender (like a bank) is willing to chip in won't cover the total project cost. This creates a funding gap between the main loan and the developer's available cash. Mezzanine Finance is a specialised, second-tier loan designed to fill this exact gap.

Think of it as a financial bridge. It sits between the senior debt and your own equity, allowing the project to proceed without you needing to find a huge amount of extra capital upfront. While the interest rates are higher to compensate for the added risk, it's an incredibly powerful tool for getting a viable project off the ground.

Mezzanine finance can be the critical ingredient that makes a project financially feasible. It allows developers to take on larger projects by reducing the initial cash they need to contribute, unlocking opportunities that might otherwise be out of reach.

Bridging Loans: For Short-Term Agility

Finally, Bridging Loans offer a short-term fix for immediate cash flow needs. These are fast, flexible loans used to "bridge" a temporary financial gap—like snapping up a new site before the sale of your last project has settled, or covering an unexpected cost that pops up.

While it's not a long-term funding strategy, bridging finance provides crucial liquidity when speed is everything. For developers who need to act on an opportunity now, it's an indispensable tool. For those seeking fast, flexible solutions outside the big banks, specialised private lending can also deliver the agility needed to keep a project moving forward without delay.

Comparing Key Development Finance Options

To help you see how these pieces fit together, here's a quick comparison of the main funding types. Each one has a specific job to do, and knowing which to use—and when—is key to a successful development.

| Loan Type | Primary Purpose | Typical Loan Term | Best For |

|---|---|---|---|

| Land Loan | Purchasing the raw land for development. | 1-3 years | Securing a site before development approvals or construction begins. |

| Construction Loan | Funding the "hard costs" of the physical build. | 1-2 years | The main construction phase, with funds released in stages. |

| Mezzanine Finance | Filling the gap between senior debt and developer equity. | 1-2 years | Projects where the developer wants to maximise leverage and minimise their upfront cash. |

| Bridging Loan | Providing fast, short-term cash flow for urgent needs. | 1-12 months | Acquiring a new site quickly or covering unexpected project costs. |

Choosing the right loan structure depends entirely on your project's specific needs, timeline, and your own financial position. By understanding these options, you're better equipped to build a funding strategy that supports your vision from start to finish.

Understanding Key Metrics Like LVR and LTC

If you want to get a development loan approved, you need to learn to speak the lender’s language. This means getting comfortable with two critical acronyms that ultimately decide how much you can borrow: the Loan to Value Ratio (LVR) and the Loan to Cost Ratio (LTC).

Think of it like this: the total cost of all your project ingredients—the land, the materials, the consultants—is your Total Development Cost (TDC). The finished project, ready to sell for a profit, represents the Gross Realisation Value (GRV). Lenders use these two figures to work out how much skin they’re willing to put in the game.

Loan to Cost Ratio (LTC) Explained

The Loan to Cost Ratio (LTC) is pretty straightforward. It compares the size of the loan to the total cost of the project. It’s the lender’s way of asking, “How much of the upfront cost are we covering, and how much are you contributing?”

Basically, it’s a measure of your "skin in the game." A bigger contribution from you means a lower LTC, which lenders love to see because it reduces their risk. This ratio is based on all your hard and soft costs, from buying the land to paying the architect.

The formula is simple:

LTC = (Loan Amount / Total Development Cost) x 100

Loan to Value Ratio (LVR) Explained

The Loan to Value Ratio (LVR), on the other hand, looks at the bigger picture. It compares the loan amount to the project’s estimated value once it’s completely finished and ready to hit the market.

This metric gives the lender a safety buffer. They’ll always get an independent valuation to determine this future value, as it sets the absolute ceiling on how much they’ll lend. It’s their protection in case the market takes a turn and final sale prices aren't what you'd hoped for.

The formula looks similar but focuses on the end value:

LVR = (Loan Amount / Gross Realisation Value) x 100

This diagram breaks down how these different finance components fit together.

As you can see, each loan type has a distinct job, from securing the land right through to funding the build.

A Practical Example in Action

Let's put this into practice with a small townhouse development.

- Total Development Cost (TDC): $2,000,000

- Gross Realisation Value (GRV): $2,800,000

Say a lender offers you terms of 80% LTC and 70% LVR. They will calculate the maximum loan using both metrics and—this is the important part—lend you whichever amount is lower.

- Based on LTC: 80% of $2,000,000 = $1,600,000

- Based on LVR: 70% of $2,800,000 = $1,960,000

In this case, your maximum loan is capped at $1,600,000. That means you'll need to fund the remaining $400,000 of the project costs yourself. This is where your own cash or property equity comes in. If you want to understand that better, check out our guide on what is equity in property.

Lenders will nearly always cap their loan based on the lower of the LVR and LTC calculations. This conservative approach is their primary method for managing risk in any building development loan.

With the major banks stepping back, non-bank lenders have jumped in to fill a $50 billion funding gap, often with more flexible terms. It's not uncommon for them to approve loans in just a couple of weeks, offering LVRs of 60-70% and LTCs up to 80%. This has made them an essential part of the modern developer's toolkit.

Your Eligibility and Documentation Checklist

Getting a building development loan isn't just about having a great idea. It's about convincing a lender you have a bulletproof plan, backed up by solid evidence. Lenders are really trying to answer two simple questions: can you deliver on your promises, and is this project actually going to make money?

Think of it like pitching a new business. You need to show a clear path to profitability and prove you've got the team and the skills to get there. Nailing your documentation is the first and most critical step—it’s the foundation of a lender’s confidence in you and your project.

The Developer: Your Personal and Financial Snapshot

Before a lender even glances at your blueprints, they want to know who they’re getting into business with. This part of the process is all about your track record, financial stability, and real-world experience in property development.

You’ll need to paint a clear picture of your financial health and history. This usually includes:

- Proof of Experience: Got a portfolio of past projects? Show it off with photos, financials, and outcomes. If you're new to the game, any relevant experience in construction or project management is a huge plus.

- Financial Statements: If you're applying through an established business, lenders will want to see the last two years of financials. For individuals, a detailed statement of your personal assets and liabilities is standard.

- Proof of Identity: Just the standard 100-point identification checks for all directors or individuals on the application.

The Project: The Commercial Viability Checklist

Once the lender is comfortable with you, their focus shifts entirely to the project itself. Every document you supply from here on should work together to prove one thing: that this project is low-risk and has a high chance of being successful and profitable. 📈

This is where you get into the nitty-gritty. Your aim is to leave no stone unturned, anticipating every question a lender's credit team might throw at you.

A well-prepared application answers a lender's questions before they're even asked. The more organised and thorough your paperwork, the faster and smoother your approval will be.

Key project documents you can't do without:

- A Detailed Development Proposal: A sharp, clear executive summary of the project, outlining the concept, who you're building for (target market), and your overall strategy.

- Council Approved Plans: This is non-negotiable. You'll need the stamped and approved architectural drawings and your Development Approval (DA).

- A Robust Feasibility Study: This is the financial heart of your pitch. It needs to detail every projected cost, the expected Gross Realisation Value (GRV), and, most importantly, the anticipated profit margin.

- A Fixed-Price Building Contract: A signed contract with a reputable, licensed builder is a game-changer. It gives the lender cost certainty and shows you've locked in a key part of the puzzle.

- Quantity Surveyor (QS) Report: An independent QS report verifies your construction costs and timeline. For lenders, this is a crucial, objective assessment of your budget's realism.

Navigating Low-Doc and No-Doc Options

For many self-employed builders, contractors, and small business owners, traditional income evidence like payslips just isn’t how their world works. This is where low-documentation (low-doc) options for building development loans are a lifesaver.

These loans are designed for borrowers who have strong assets and a solid business history but can't easily produce standard income verification. Instead of payslips, lenders will accept other documents to prove you can service the loan.

Common alternative documents include:

- Business Activity Statements (BAS): Your last 12 months of BAS lodgements give a clear snapshot of your business's turnover.

- An Accountant's Letter: A letter from your accountant confirming your income and the financial health of your business can go a long way.

- Business Bank Statements: Usually, the last six to twelve months of statements are enough to demonstrate consistent cash flow.

It's important to remember that low-doc isn't a shortcut for weak projects or bad credit. Instead, it's a flexible pathway for credible, experienced business owners to get the development finance they need, based on the real-world financial strength of their operations.

The Application Process from Start to Finish

Securing a building development loan isn’t a one-step transaction; it’s a journey with several key stages. Knowing what’s coming helps you set realistic expectations and makes the whole process smoother, right from your first chat with a broker to the final invoice being paid.

Let’s pull back the curtain on the typical application timeline.

The real work starts long before you fill out any forms. It begins with a deep-dive strategy session to talk through your project’s vision, budget, and timelines. This first conversation is all about aligning your goals with what’s financially achievable, setting a rock-solid foundation for everything that follows.

From there, the goal is to get pre-approval. This is where a lender does a preliminary check on your finances and the project's basic viability. It gives you a conditional green light and, just as importantly, a clear idea of how much you can likely borrow.

From Formal Application to Settlement

With pre-approval sorted, it’s time for the formal application. This is when you’ll submit all the documentation we've talked about, and the lender’s due diligence really kicks into gear. They’ll scrutinise everything—your feasibility study, building contracts, and council-approved plans—to make sure every detail stacks up.

A critical piece of this puzzle is the lender's independent valuation. They’ll send out a valuer to assess the project's "on-completion" value, or Gross Realisation Value (GRV). This number is what ultimately confirms the ceiling on what they're prepared to lend. Once the valuation is in and their checks are complete, you’ll get a formal loan offer, which leads to settlement.

How Staged Drawdowns Work in Practice

Settlement doesn’t mean a lump sum of cash lands in your bank account. Instead, development finance uses a system of staged drawdowns. This means funds are released in stages as you hit key construction milestones, acting as the financial engine that keeps your project moving forward.

This progressive payment structure is smart because it protects both you and the lender. You only pay interest on the money you’ve actually drawn down, which keeps your holding costs manageable while the site isn't yet generating any income.

The staged drawdown process is central to effective project management. It ensures that capital is deployed precisely when and where it's needed, tying funding directly to tangible construction progress and maintaining project momentum.

A typical drawdown schedule is tied to major construction phases:

- Deposit: The initial funds to get the builder started.

- Slab Down: Payment is released once the concrete foundation is poured.

- Frame Stage: Funds are provided once the building’s frame and roof trusses are up.

- Lock-Up Stage: Payment is made when external doors, windows, and roofing are installed, making the property secure.

- Fixing Stage: This covers internal fit-outs like plasterboard, kitchen cabinets, and bathroom fixtures.

- Completion: The final payment is made once the project is practically complete, confirmed by a final inspection.

Before each payment is released, a quantity surveyor usually inspects the site to verify the work has been done. This methodical approach gives you peace of mind and ensures your builder is paid on time, keeping the whole project on track. As new housing commitments continue to grow, understanding this process is more critical than ever. Recent figures show owner-occupier commitments for new dwellings hit a 3.5-year high of AUD 58.2 billion in the third quarter, which just goes to show how strong the demand is. You can discover more insights about these lending indicators.

How a Broker Can Get Your Development Finance Across the Line

Trying to navigate the world of development finance on your own isn't just tough—it's a massive drain on your time and energy. Bringing a specialist finance broker on board isn't about handing off paperwork. It's about getting a financial co-pilot who knows the landscape inside and out and can guide your project from a plan on paper to a completed build.

A broker’s biggest advantage is their network. Let’s be frank: the major banks have rigid, conservative scorecards. If your project doesn't tick every single box, you'll likely get a "no". But a specialist broker lives and breathes this stuff, and they have strong relationships with a whole ecosystem of non-bank and private lenders.

These lenders are far more agile. They actually specialise in development finance and are comfortable looking at projects with unique structures or those that sit just outside the banks' narrow policies. This opens up a whole world of funding options you’d never find on your own.

Building a Bulletproof Application

Beyond just playing matchmaker with lenders, a good broker is your strategist. They know exactly what underwriters are looking for and will help you shape your application to give it the absolute best chance of a fast, clean approval. This is way more than just collecting documents.

A skilled broker will help you:

- Sharpen Your Feasibility Study: Making sure your costings, GRV projections, and profit margins are crystal clear, realistic, and presented in a way lenders understand and trust.

- Play to Your Strengths: They'll highlight your experience and the project's best features to build confidence with the credit team.

- Tackle Weaknesses Head-On: A great broker spots potential red flags in your application and addresses them proactively, so they don’t become deal-breakers down the line.

This level of preparation makes your project a much stronger proposition. It doesn't just improve your approval odds; it speeds the whole process up.

The Art of Negotiation and a Smoother Process

Perhaps the most valuable part is having a seasoned negotiator fighting in your corner. Brokers use their industry know-how and lender relationships to secure better terms than you could likely get alone. We're talking better interest rates, higher LVR or LTC ratios, or more practical drawdown schedules that actually work with your build timeline.

A great broker doesn't just find you a loan; they find you the right loan. They run the entire process for you—from the first submission to the final settlement—so you can focus on what you do best: managing the actual development.

By handling the endless back-and-forth with lenders, valuers, and solicitors, a broker saves you a huge amount of time and stress. They see problems coming, fix them before they escalate, and keep the money side of your project flowing. This ensures you have the capital you need, right when you need it, which is absolutely critical for any successful development.

Common Questions About Building Development Loans

When you’re diving into the world of development finance, a lot of specific questions pop up. To give you some real-world clarity, we’ve put together straight answers to the queries we hear most often from developers.

How Is Interest Calculated and Paid on a Development Loan?

With a development loan, interest is almost always capitalised. What does that mean? Instead of you making monthly interest payments out of your own pocket, the interest is simply added to the total loan balance while you’re building.

This structure is a game-changer for your cash flow, especially when the project isn’t generating any income yet. The crucial detail here is that interest is only charged on the funds you’ve actually drawn down.

So, if you have a $1 million loan facility but you’ve only used $200,000 for the initial site works, you only pay interest on that $200,000. Once the project is finished, the full loan amount—including all that capitalised interest—is repaid, usually from the sale of the properties or by refinancing to a standard investment loan.

What Are the Main Risks and How Can I Mitigate Them?

Every development project faces the same big three risks: construction delays, unexpected cost blowouts, and a dip in the property market that hits your sale prices. The good news is, there are practical steps you can take to get ahead of these challenges.

A well-structured finance plan from an expert broker is your first and best line of defence. It ensures you have the right funding structure and contingencies in place before you even break ground.

Here’s how you can build a safety net around your project:

- Lock in a fixed-price building contract with a reputable, licensed builder. This puts a firm cap on your construction costs and gives you certainty.

- Build a contingency fund into your budget. We recommend setting aside 10-15% of the total build cost to create a financial buffer for any surprises.

- Hire an experienced project manager to keep the build on track and handle the contractors effectively.

- Do your homework with thorough market research and a conservative feasibility study. This helps protect you against shifts in property values.

Can I Get a Loan Without Any Pre-Sales?

Yes, you absolutely can, but your application needs to be much stronger. While the major banks often insist on a certain number of pre-sales to prove market demand and lower their risk, many specialist non-bank lenders are far more flexible.

To get a "no pre-sale" development loan across the line, you’ll need to show you’re a lower-risk bet in other areas. This usually means putting more of your own equity into the deal (leading to a lower LVR), having a solid personal financial position, and—most importantly—a proven track record of delivering successful projects.

These loans might carry a slightly higher interest rate to compensate the lender for taking on that extra risk. But for seasoned developers confident in their project's appeal, this flexibility is invaluable for getting dirt turning sooner.

Ready to turn your development plans into reality? The team at Diamond Lending has access to a wide panel of bank and non-bank lenders specialising in development finance. Let us help you structure the right funding for your project. Start your journey with us today.