Ever heard of a no doc private loan? It's a specialised way to get funding where lenders are more interested in the value of your property assets than a pile of payslips or tax returns. For self-employed folks and property investors with solid equity but messy paperwork, it’s a game-changer.

Navigating Finance Without Traditional Paperwork

For a lot of self-employed Aussies, business owners, and property developers, the typical loan application is a nightmare. Traditional banks are stuck in the past, rigidly looking at your financial history. They demand two years of perfectly consistent, taxable income, all laid out in neat tax returns.

This cookie-cutter approach just doesn't work for people with complex or fluctuating income. If your earnings are project-based, or you've just launched a promising new business, proving your ability to repay in a way that satisfies a major bank can feel like an impossible task. It’s a fast track to missed opportunities and stalled projects, leaving entrepreneurs feeling like the system is built against them.

Shifting the Focus from Past to Potential

This is exactly where no doc private loans find their sweet spot. Instead of asking, "What did you earn last year?", private lenders ask a completely different question: "What is your asset worth and how will you pay this back?"

That simple change in perspective unlocks doors that would otherwise be slammed shut. The focus shifts from historical paperwork to the real-world value of your property and the strength of your plan. It's a funding path designed for those who don’t fit the standard 9-to-5 mould.

A no doc private loan provides a funding pathway based on the strength of your assets and your exit strategy, not stacks of historical income documents. It’s a solution that values present equity over past earnings.

At its core, it's about unlocking the capital tied up in your assets without jumping through the endless hoops of traditional banking. For the right borrower, it’s a powerful tool for grabbing time-sensitive opportunities, bridging funding gaps, or simply getting a project off the ground without delay. This guide will show you exactly how it all works.

What Exactly Is a No Doc Private Loan?

Let's get one thing straight from the start: a no doc private loan isn't about having zero paperwork. Not at all. It’s about using different paperwork—the kind that tells a story about your assets and your plan, rather than just digging up your past tax returns.

Think of it like a private investor backing a solid business idea. They aren't fixated on your financial history from two years ago; they're far more interested in whether the project itself makes commercial sense. In this world, your property is the business plan, and your exit strategy is the proof that it's a winner.

This is the core idea behind a no doc private loan. It’s a form of asset-backed finance offered by private lenders who operate outside the rigid, tick-a-box world of the major banks.

It’s All About the Asset

Traditional banks are bound by strict, one-size-fits-all lending criteria. They need to see historical income documents like payslips and tax assessments to calculate your serviceability. If your paperwork doesn't fit neatly into their system, your application is usually dead in the water, no matter how valuable your property or project is.

Private lenders come at it from a completely different angle. They zoom in on two things that matter most:

- The Security Property: How strong is the real estate you're putting up as collateral? They'll look at its value, location, and how easily it could be sold.

- The Exit Strategy: Do you have a clear, believable plan to pay back the loan? This could be selling the property, refinancing to a traditional loan down the track, or using incoming business revenue.

This "asset-first" approach allows them to fund deals with incredible speed and flexibility, solving problems that banks simply can't touch.

A Different Kind of Lending Partnership

This style of lending really took hold in Australia’s financial scene back in the early 2000s. The market for no-doc and low-doc products grew fast, created to help self-employed people who didn't have the standard proof of income. At its peak, this slice of the market made up a significant chunk of bank assets, proving there was a real need for funding that bypassed the usual red tape.

By focusing on the property's equity and the borrower's exit plan, a no doc private loan becomes a powerful strategic tool. It’s not meant to be a long-term mortgage; it's a short-term solution designed to help you jump on an opportunity when it appears.

A no doc private loan completely reframes the lending question. It shifts the focus from, "What does your past paperwork say?" to "What is your asset worth, and what's your plan for the future?"

This is absolutely vital for property developers who need bridging finance or for business owners who have to lock down a commercial site before a competitor snaps it up. For a deeper look into how this works in the real world, check out our comprehensive guide on no doc loans in Australia. It’s a system built on commercial logic, common sense, and the tangible value of property.

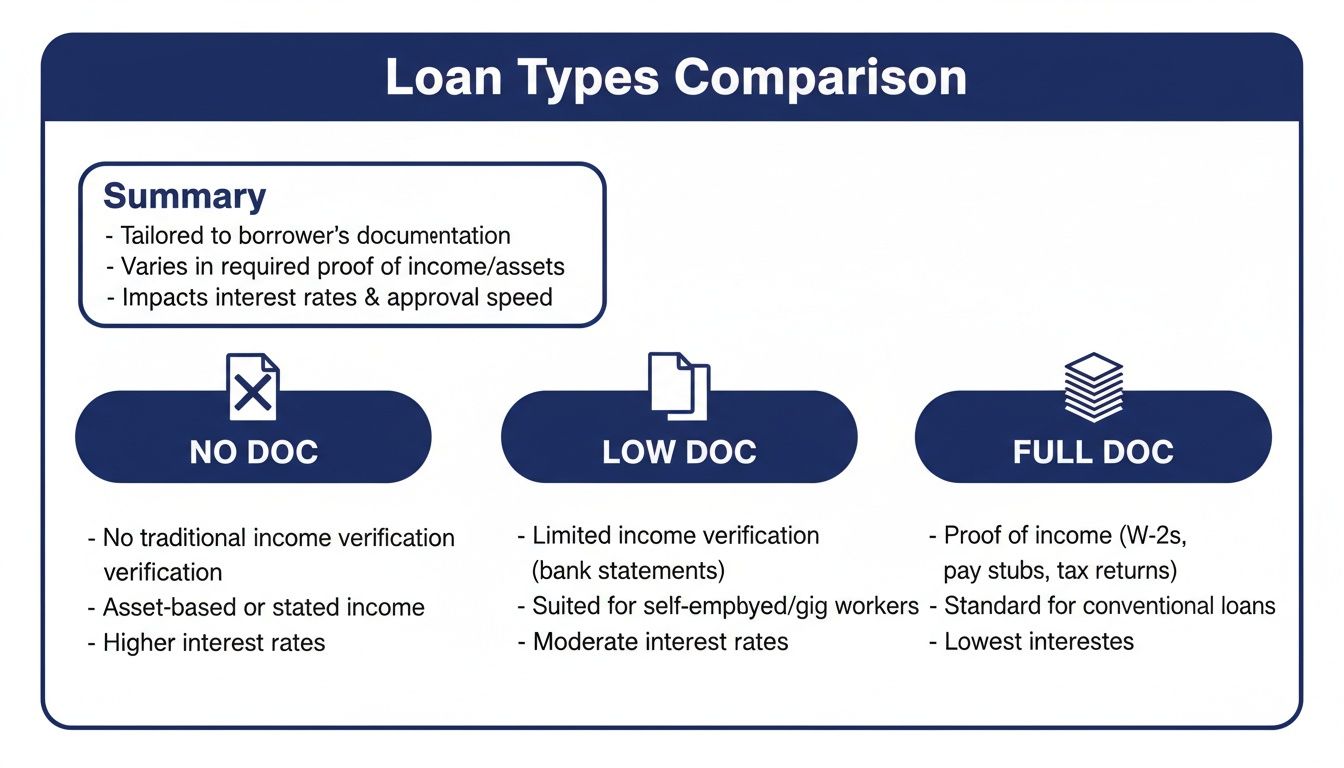

Comparing No Doc, Low Doc, and Full Doc Loans

Choosing the right loan can feel like you're trying to find your way through a maze of industry jargon. You'll hear terms like "no doc," "low doc," and "full doc" thrown around, but what do they actually mean for you?

Each of these loan types is a different path, designed for a different kind of borrower. The trade-offs usually come down to paperwork, speed, and cost. Getting your head around these differences is the first real step toward finding a funding solution that genuinely fits your goals.

The Documentation Spectrum

The biggest difference between these loans boils down to one thing: paperwork. Specifically, how much of it you need to provide to prove you can repay the loan. This can range from a complete financial deep-dive to simply showing the value of the property you're offering as security.

A full doc loan is the classic home loan you’d get from a major bank. It’s built for PAYG employees with a straightforward financial history. Lenders will want to see everything, including:

- At least two years of personal and business tax returns.

- Recent payslips to verify your current income.

- Detailed financial statements and profit-and-loss reports if you run a business.

A low doc loan is the happy medium. It was created for self-employed Aussies and small business owners who have a solid trading history but might not have their tax returns perfectly up to date. Instead of the full suite of documents, lenders are often happy with:

- Business Activity Statements (BAS) from the last 6-12 months.

- A formal letter from your accountant confirming your income.

- Business bank statements that show a healthy, consistent cash flow.

Then you have the no doc private loan. This option throws the traditional income verification rulebook out the window. The lender's focus shifts almost entirely from your past earnings to the strength of your security property and your plan to exit the loan.

A Side-by-Side Comparison

To really see how these loans stack up, let's put them next to each other. This table cuts through the noise and highlights the key differences that matter most when you're making a decision.

Loan Documentation Levels Compared

| Feature | No Doc Private Loan | Low Doc Loan | Full Doc Loan |

|---|---|---|---|

| Primary Lender | Private Lenders & Non-Banks | Specialist Lenders & some Banks | Major Banks & Traditional Lenders |

| Documentation | Asset & Exit Strategy Focused | Alternative Income Verification (e.g., BAS) | Full Financials & Tax Returns |

| Approval Speed | Very Fast (days) | Moderate (weeks) | Slow (weeks to months) |

| Interest Rates | Higher | Moderate | Lower |

| Loan-to-Value Ratio (LVR) | Typically up to 75% | Up to 80% | Up to 80% (or higher with LMI) |

| Ideal Borrower | Property Investors, Developers | Self-Employed, Business Owners | PAYG Employees, Established Businesses |

This comparison makes it clear that each loan is a specific tool for a specific job. There's no "best" option—only the one that’s right for your unique circumstances.

Why Choose One Over the Other?

The table shows you the what, but the why is where the real strategy comes in.

A full doc loan is the go-to for someone with a stable, easily proven PAYG income who wants the lowest possible interest rate for a standard 30-year mortgage. It's safe, predictable, and cheap.

A low doc loan is perfect for a consultant or a small business owner whose income is regular but whose tax returns aren't lodged yet. It finds a great middle ground on rates and paperwork, giving entrepreneurs access to finance without the administrative headache.

A no doc private loan is a highly specialised tool. It is purpose-built for time-sensitive, asset-backed transactions where the opportunity cost of waiting for a traditional bank is far greater than the higher interest rate.

Think about a property developer who finds the perfect site, but it’s going to auction in a week. They can't afford to wait months for a bank to approve their finance. A no doc private loan lets them use the equity in another property to secure funding in just a few days. They snap up the opportunity and can then refinance to a cheaper loan later on.

It all comes down to understanding that trade-off between speed, cost, and paperwork. Once you nail that, you can make a truly smart financial decision.

Who Qualifies for a No Doc Private Loan

A no doc private loan isn’t for everyone, but for the right borrower, it’s an incredibly powerful tool. These loans are built for people and businesses who have solid equity tied up in real estate but don't have the neat-and-tidy income paperwork that mainstream banks demand.

Think of it this way: private lenders are looking for borrowers whose stories make commercial sense, even if their tax returns don’t paint the full picture just yet. The best candidates are often asset-rich, but their income might be complex, inconsistent, or not yet fully captured on paper.

The Ideal Borrower Profiles

Certain situations and professions are a natural fit for this kind of funding. Private lenders are used to dealing with these types of applicants and understand their unique financial circumstances. If you see yourself in one of these categories, a no doc private loan could be the key to your next big move.

- Property Developers: A developer needs to act fast to snap up a new site or bridge a funding gap between construction stages. They’ve got plenty of equity across their portfolio but simply can’t afford to wait months for a bank to say yes.

- Business Owners: An entrepreneur might need to buy a commercial property quickly to expand their business. The company could be highly profitable, but recent investments or growth expenses might make their documented income look deceptively low.

- Self-Employed Individuals: Consultants, contractors, and freelancers often deal with fluctuating income. They might have just landed a massive contract, but last year's tax return doesn't come close to reflecting their current earning potential.

In every case, the common threads are a time-sensitive need and strong property backing that gives the lender a solid safety net.

The chart below gives you a quick visual comparison of the different documentation levels, showing exactly where no doc loans fit into the puzzle.

As you can see, when the paperwork requirements drop from Full Doc to No Doc, the lender’s focus pivots sharply from historical income to the quality of the asset itself.

What Private Lenders Look For

When a private lender reviews a no doc loan application, their mindset is laser-focused on two things. They cut through the traditional bank checklists and concentrate on the commercial reality of the deal. If you get this, you’ll know if you qualify.

The entire lending decision for a no doc private loan rests on two pillars: the quality of the real estate security and the clarity of your exit strategy. Get these right, and the lack of traditional income proof becomes secondary.

Let’s break down exactly what that means.

1. Quality of the Real Estate Security

The property is the absolute foundation of the loan. Lenders need to be completely confident that if things go sideways, the asset can be sold without hassle to get their money back. They’ll assess:

- Location: Is the property in a desirable, high-demand metro or key regional area?

- Property Type: Standard residential or commercial properties are far easier to fund than highly specialised or unusual assets.

- Loan-to-Value Ratio (LVR): Lenders will almost always cap the LVR at around 75%. This means you need a serious amount of your own skin in the game, creating a substantial buffer that protects the lender.

2. Clarity of the Exit Strategy

A no doc private loan is a short-term fix, usually for 1-3 years. The lender needs to see a clear, believable plan for how you’ll pay back the loan in full when the term is up. Common exit strategies include:

- Selling the Property: You plan to sell the security property or another asset you own to clear the debt.

- Refinancing: Once your project is finished or your income situation is more stable and "bank-friendly," you'll refinance to a long-term loan with a traditional lender.

- Incoming Revenue: Using expected funds from a business sale, the completion of a project, or a large contract payout to settle the loan.

Your ability to spell out a logical and achievable exit strategy is just as crucial as the property itself. It proves to the lender that you’ve thought the whole thing through, turning what might seem like a risky proposal into a calculated business decision.

The Application and Alternative Documentation Process

So, how do you actually get a no doc private loan across the line when you don’t have the neat pile of payslips and tax returns a traditional bank demands?

The whole process is refreshingly different. It's built for speed and commercial common sense, stripping away the red tape to focus on what truly matters to a private lender: the strength of your asset and your plan to repay the loan.

Instead of a long, drawn-out ordeal, the journey from initial chat to funding can happen in a matter of days, not months. The key is understanding that 'no doc' simply means alternative documentation—evidence that proves your financial standing in other ways.

The Four Key Steps to Funding

The path to securing your funds is designed to be efficient and transparent. While every lender has their own nuances, the journey typically follows four clear stages so you know exactly where you stand.

-

Initial Consultation and Scenario Assessment: This is a quick, no-fuss conversation with an expert broker. You’ll explain what you need the funds for, the property you’re using as security, and your exit strategy. The goal is to figure out fast if private lending is the right fit.

-

Indicative Approval and Valuation: If the deal looks solid, you'll receive an indicative offer outlining the likely terms. From there, the next step is a formal valuation of the security property. A private lender needs an independent, up-to-date value to confirm the asset's worth and calculate the Loan-to-Value Ratio (LVR).

-

Formal Approval and Loan Documents: Once the valuation comes back and aligns with everyone’s expectations, the lender will issue a formal, unconditional approval. You'll then get the official loan documents to review and sign.

-

Swift Settlement: After the documents are signed and returned, things move very quickly. Funds are often disbursed within 24-48 hours, giving you the capital you need to seize your opportunity without delay.

Proving Your Position Without Payslips

This is where people often have the most questions. How do you build a compelling case without the usual paperwork? Lenders accept several common-sense forms of alternative documentation to verify your financial standing and the viability of your plan.

This isn’t about taking a risky shortcut; it's a structured method based on credible, asset-focused evidence.

The core idea behind a no doc private loan is simple: your assets and your exit plan tell a more powerful story than old tax returns. The 'alternative' documents you provide are all about proving the strength of that story.

The documentation is designed to be straightforward to pull together but powerful enough to give the lender total confidence in the deal.

Key Alternative Documents You Will Need

To get your no doc private loan application approved, you’ll typically be asked for a combination of the following:

- A Signed Asset and Liability Declaration: This is just a simple form where you list out your current assets (property, vehicles, investments) and liabilities (other loans, credit cards). It gives the lender a clear snapshot of your net worth, which is a key metric for them.

- An Accountant's Letter: A letter from your accountant can be incredibly persuasive. It can verify your financial position, confirm your business is trading, and add a layer of professional credibility to your proposed exit strategy.

- A Written Loan Purpose Summary: This is a clear, concise summary explaining why you need the funds and exactly how they will be used. It shows the lender you have a well-thought-out plan.

- A Detailed Exit Strategy Plan: This is arguably the most critical piece of the puzzle. You must clearly outline how you will repay the loan. Whether it's through the sale of the property, refinancing to a mainstream lender later on, or using incoming business revenue, your plan needs to be logical and achievable.

While the paperwork is different from a bank loan, the need for a solid, professionally presented case is just as important. This approach is what makes a no doc private loan a secure and reliable funding solution for the right borrower.

Understanding the Costs, Risks, and Regulations

Any smart financial move means looking at the picture from all angles. A no doc private loan offers incredible speed and flexibility, but that convenience comes with a different cost and risk profile compared to a standard bank loan. It’s crucial to get your head around these factors before you jump in.

The higher costs really just reflect the lender's position. They’re taking on more risk by skipping the traditional income verification hoops, and they're getting you the funds in a fraction of the time a bank would. This trade-off is balanced out with higher interest rates and setup fees.

The True Cost of Speed and Convenience

When you opt for a no doc private loan, you're essentially paying a premium for fast, asset-focused funding. The costs are transparent, but they're structured differently from a long-term mortgage you might be used to.

- Higher Interest Rates: You should expect interest rates to be noticeably higher than what the major banks offer. This is the main way private lenders cover themselves for the increased risk that comes with these kinds of loans.

- Establishment and Valuation Fees: There will be upfront costs to get the loan set up. This includes things like application fees, legal charges, and the cost of an independent property valuation. These are all standard in the private lending space.

These costs aren't hidden surprises; they're just part of how this specialised financial product works. For the right borrower, the return they get from grabbing a time-sensitive opportunity far outweighs these expenses.

Think of a no doc private loan as a strategic business expense. The key is making sure the potential profit from your project or investment comfortably covers the cost of the finance.

Potential Risks and How to Mitigate Them

Every financial decision has some risk, and it’s vital to go in with your eyes open. With any short-term loan, the single biggest risk is failing to pull off your exit strategy.

Because these loans typically run for terms of one to three years, the clock is always ticking. If your plan to sell the property or refinance gets delayed, you could find yourself under pressure as the loan's maturity date looms. This is why having a solid, realistic exit plan—and a backup plan—is absolutely essential.

Another thing to remember is the nature of the loan itself. These are commercial arrangements, not consumer credit products. That means they fall outside some of the protections offered by the National Consumer Credit Protection (NCCP) Act.

The Australian Regulatory Landscape

It's important to understand the legal framework for these loans in Australia. The National Consumer Credit Protection (NCCP) Act 2009 was put in place to protect individuals taking out loans for personal, domestic, or household reasons.

However, a no doc private loan is almost always used for business or investment purposes—like buying a commercial property, funding a development, or injecting cash into a business. This means they generally aren't regulated by the NCCP Act.

This distinction is precisely why private lenders can offer more flexible, asset-focused solutions. They aren’t tied down by the same rigid income verification rules that apply to consumer loans. It allows them to assess a deal on its commercial merits, but it also puts more responsibility on you, the borrower, to fully understand the terms and risks involved. This regulatory environment ensures these loans serve their intended purpose: as a powerful tool for savvy investors and business owners.

How a Specialist Broker Secures Your Funding

Trying to find the right no doc private loan on your own is like navigating a maze without a map. The world of private lending isn't advertised on billboards; it's a complex network of investors and non-bank institutions, and each one has a very specific appetite for risk and the kinds of deals they'll even look at. This is where partnering with a specialist broker changes the entire game.

Think of a specialist broker as your guide and advocate. Instead of you spending countless hours trying to find a lender who gets your unique situation, a broker does all the heavy lifting. They already have established relationships with a wide range of private lenders, many of whom you’d never find through a Google search.

This insider access is a massive advantage. It means your application lands in front of the right decision-makers from day one—lenders who are actively looking to fund deals just like yours. That saves you time, frustration, and the risk of racking up multiple rejections on your credit file.

Structuring Your Application for a 'Yes'

Getting a no doc private loan approved is less about filling out forms and more about telling a compelling story. An expert broker knows exactly what private lenders need to see to feel confident in a deal. They help you craft a narrative that doesn't just ask for money, but clearly shows why it’s a smart investment for them.

This involves:

- Polishing your exit strategy until it is clear, logical, and completely believable.

- Gathering the right alternative documentation to build a strong, credible case that proves your capacity.

- Presenting your loan purpose in a way that aligns perfectly with the lender's investment goals.

A specialist broker doesn't just find you a loan; they help you structure your entire proposal for success. They understand the lender's mindset and ensure every part of your application speaks their language, dramatically increasing your chances of approval.

Beyond the application itself, a skilled broker can negotiate on your behalf. They use their relationships and deep market knowledge to secure better interest rates and terms than you might get going it alone. They make sure the loan structure is sound and that your exit strategy isn't just a plan on paper, but a viable reality.

With the right expert partner, what might seem like a complicated financial product becomes a powerful strategic tool. It’s the key to unlocking your property's equity and seizing the kind of opportunities that build real wealth. The path forward is often much simpler than you think.

Ready to unlock your next opportunity without the paperwork headache? The team at Diamond Lending specialises in connecting investors and business owners with fast, reliable funding solutions. It all starts with a simple, no-obligation chat to see how we can help. Contact us today to discuss your scenario.