Getting the right vehicles and equipment is essential for your business to grow, but paying for them outright can seriously drain your cash reserves. This is exactly where vehicle and equipment finance becomes a powerful tool. Think of it less like a simple loan and more like a strategic way to get the assets you need now—from a new work ute to critical construction gear—while keeping your capital free for everything else that keeps your business humming.

Powering Your Business With Smart Asset Finance

For any Aussie business, having the right tools isn't just a nice-to-have; it's fundamental to making money. Whether it’s a delivery van for a courier or specialised machinery for a workshop, these assets are the engines of your operation. The problem? Their high upfront cost can feel like a major roadblock.

This is precisely the challenge that smart asset finance is designed to solve. Instead of sinking your working capital into one massive purchase, you can spread the cost over the asset’s useful life. This simple shift turns a huge capital expense into a predictable, manageable operating cost.

Preserving Cash Flow for Growth

Healthy cash flow is the lifeblood of any business, crucial for both survival and expansion. By financing key assets, you keep your money in the bank, ready to be deployed where it’s needed most. This preserved capital can be used for:

- Operational Expenses: Easily cover day-to-day costs like wages, rent, and supplies without the financial squeeze.

- Marketing and Sales: Invest in campaigns that bring in new customers and drive real revenue growth.

- Expansion Opportunities: Stay agile enough to jump on new projects or enter new markets the moment an opportunity pops up.

The core idea is simple: use your capital to run and grow your business, not just to own stuff. Financing lets you get the mission-critical tools you need without sacrificing the financial flexibility that sets you up for success.

Ultimately, vehicle and equipment finance gives your business a serious competitive edge. It allows you to get your hands on the latest, most efficient gear now, rather than waiting months or years until you’ve saved up enough to buy it outright. This guide will walk you through exactly how it all works and help you find the perfect solution for your business.

How Vehicle and Equipment Finance Actually Works

So, how does this all work in the real world?

At its heart, vehicle and equipment finance is simply a smart way to get the tools your business needs now, without emptying your bank account. It’s a specialised type of funding designed to skip the massive upfront cash payment, keeping your working capital free for things like wages, inventory, or marketing.

Let's walk through a common scenario. Imagine your construction company lands a big contract and needs a new excavator to get the job done. That machine costs $80,000—a huge hit to your cash flow if you paid for it outright.

Instead of draining your funds, you partner with a lender. They purchase the excavator for you. In exchange, your business makes regular, predictable payments over an agreed term, usually three to five years. The best part? You have full use of that excavator from day one, putting it to work and generating income immediately.

Think of It as a 'Business Rent-to-Own'

A great way to wrap your head around it is to think of it like a business 'rent-to-own' model. You get the immediate benefit of the asset while paying for it over its useful life.

And here’s a crucial difference from other business loans: you don't typically need to put up your house or other property as security. Why? Because the asset itself—the truck, the IT hardware, the coffee machine—is the security for the loan.

This is exactly why vehicle and equipment finance is often much easier to get approved for, especially for new or growing businesses. Lenders see less risk because a tangible, valuable asset is backing the deal. It's a powerful and incredibly practical solution for getting those mission-critical tools.

To make it happen, a few key players need to work together. Understanding their roles makes the whole process clear and smooth, especially when you have the right people in your corner.

The Key Players in Your Finance Journey

Getting your new gear funded is really a team effort. There are three main parties involved, and each has a vital part to play.

- Your Business (The Borrower): That's you. You’re the one who needs the asset to run your operations and grow. Your job is to find the right piece of equipment and show how it’s going to help your business make money.

- The Lender (The Financier): This is the bank or specialist non-bank lender who puts up the cash to buy the asset. They assess your application and hold security over the asset until you've made the final payment.

- The Specialist Broker (Your Advocate): A broker, like the team here at Diamond Lending, is the critical link between you and the lender. We don't lend the money ourselves. Instead, we use our industry knowledge and deep network of lenders to find the perfect match for your specific situation. A good broker fights for the best terms on your behalf and handles all the paperwork, saving you a massive amount of time and stress.

Asset finance is about acquiring mission-critical tools without sacrificing the capital you need to run your business.

This partnership is built for one thing: efficiency. A good broker knows the unique lending appetites of dozens of different financiers—who’s happy to fund used equipment, who has the sharpest rates, and who is best for low-doc applications. By navigating this complex market for you, we make sure you not only get a 'yes', but you get a deal that genuinely fits your business goals.

Comparing Your Finance Options: Chattel Mortgage vs Hire Purchase vs Lease

Picking the right finance structure for a new vehicle or piece of equipment isn't just a small detail—it's a critical business decision. It directly shapes your cash flow, your tax obligations, and whether you actually own the asset in the long run.

Think of it like this: you need to get from Point A to Point B. The destination is the new asset, but you have three different roads you can take to get there. The path you choose depends entirely on your business's financial strategy. Do you want to own it straight away? Prefer lower initial costs? Or need the flexibility of not having it on your balance sheet?

The three main roads in Australia are the Chattel Mortgage, Hire Purchase, and Lease.

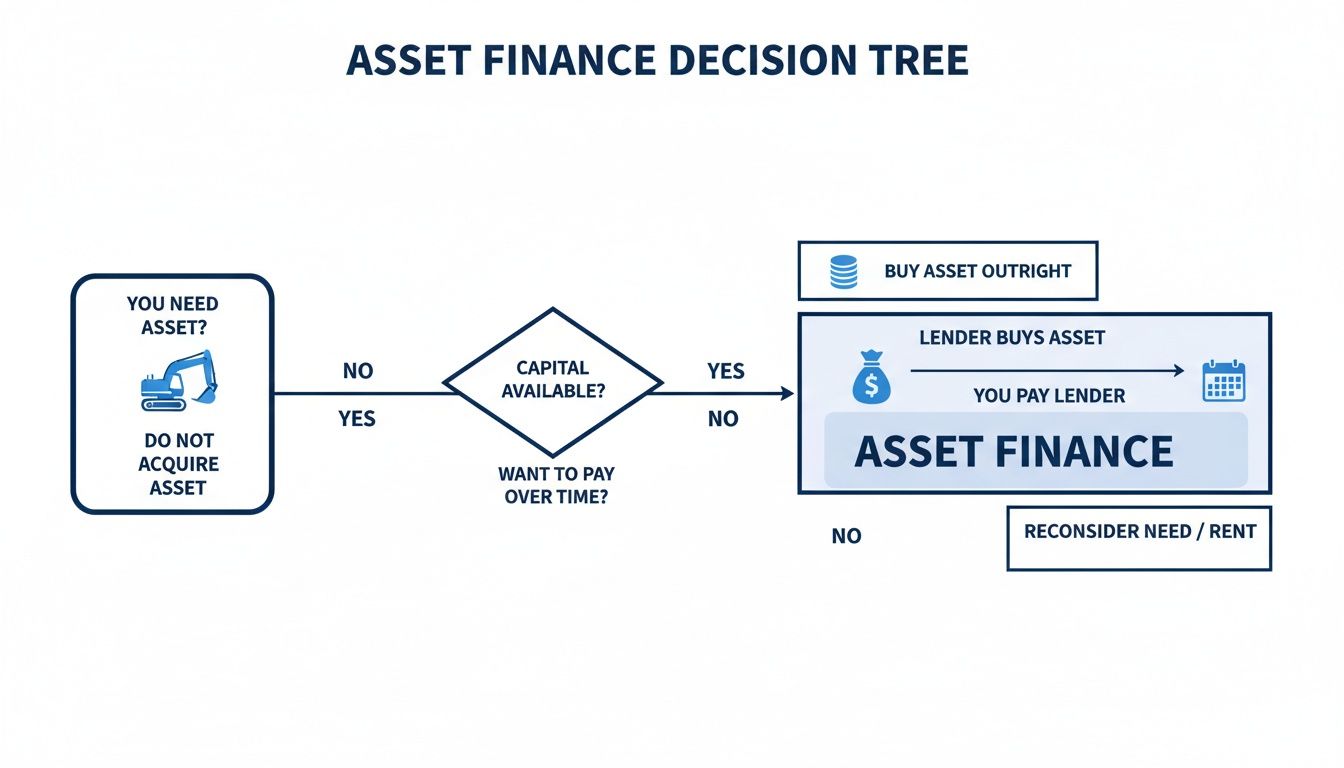

At its core, the process is pretty straightforward. You find the asset you need, the lender buys it, and you pay them back over an agreed-upon term to use it. This decision tree gives you a great visual breakdown of that flow.

But the real magic happens when you dig into the specifics of each agreement, as that’s what defines the relationship between you and the lender.

Chattel Mortgage: The Path to Immediate Ownership

The Chattel Mortgage is easily one of the most popular ways to finance business assets in Australia, especially for businesses registered for GST. Here’s how it works: the lender gives you the funds to buy the asset, and you take ownership from day one. In return, the lender takes out a "mortgage" (or security interest) over the asset—the "chattel"—until the loan is fully paid off.

The big win here is pretty clear. Because you own the asset immediately, you can typically claim the full GST from the purchase price on your next Business Activity Statement (BAS). You can also claim depreciation on the asset and the interest portion of your repayments as tax deductions.

A Chattel Mortgage is the go-to for businesses that want to own their assets from the start and get the most out of their tax benefits. It’s a direct and powerful way to build your company’s asset base.

This structure is a perfect match for long-term workhorses like commercial utes, construction machinery, and manufacturing equipment. If owning the asset at the end of the term is your number one priority, this is usually the most direct route. For a deeper dive, check out our guide on securing car finance for your business assets.

Hire Purchase: A Hire-Then-Own Journey

A Hire Purchase works a bit differently. In this setup, the finance company buys the asset you need, and your business effectively hires it from them for a set period. You make your regular payments, and once you make that final payment at the end of the term, ownership officially transfers over to you.

The key difference is that during the hire period, the financier is the legal owner. This changes the tax game. You can still generally claim the interest charges and depreciation, but the GST is claimed bit by bit on each rental payment, not as a lump sum upfront like with a chattel mortgage.

This "hire-then-own" model is a solid choice for businesses that want a clear path to ownership but prefer to avoid the immediate balance sheet impact.

Finance and Operating Leases: Using an Asset Without Owning It

Finally, we have leases, which are really just long-term rental agreements. The main idea behind a lease is that there's often no plan to own the asset when the term is up.

-

Finance Lease: This is a longer-term arrangement where the financier buys the asset and you lease it for most of its useful life. When the lease ends, you usually have a few options: pay a final "residual" amount to take ownership, trade it in for a newer model, or simply extend the lease. The lease payments themselves are generally tax-deductible.

-

Operating Lease: This is more of a short-term rental, perfect for equipment that gets outdated fast—think IT hardware or certain types of vehicles. The lender owns the asset and carries all the risk of what it will be worth down the track. A huge advantage here is that the payments are treated as a simple operating expense, which keeps the asset and the liability completely off your balance sheet.

Chattel Mortgage vs Hire Purchase vs Lease At a Glance

Feeling a bit overwhelmed by the options? Don't worry, that's normal. Breaking it down side-by-side really helps clarify which structure might be the best fit for your specific situation. This table cuts through the jargon and gets straight to the point.

| Feature | Chattel Mortgage | Hire Purchase | Finance/Operating Lease |

|---|---|---|---|

| Ownership | You own the asset from day one. | The lender owns the asset until the final payment is made. | The lender owns the asset throughout the term. |

| GST Claim | Claimed upfront on the asset's purchase price. | Claimed progressively on each rental instalment. | Claimed progressively on each lease payment. |

| Tax Deductions | Interest on repayments and asset depreciation. | Interest on instalments and asset depreciation. | The full lease rental payment is typically deductible. |

| Best For | Businesses wanting immediate ownership and maximum tax benefits. | A clear hire-to-own path with predictable payments. | Short-term use of assets or keeping debt off the balance sheet. |

Ultimately, there's no single "best" option—only the one that’s best for you. The right vehicle and equipment finance structure is the one that supports your business's financial health, cash flow, and long-term growth plans.

The Rise of Sustainable and Used Asset Financing

The world of vehicle and equipment finance is definitely changing. While the big, traditional assets are still the backbone of Australian industry, two powerful trends are reshaping how businesses get the tools they need. There's a growing commitment to sustainability on one side, and on the other, an ever-present demand for cost-effective used machinery.

These aren't just passing fads. They show how modern financing has become flexible enough to support both cutting-edge green tech and the proven, budget-friendly workhorses that keep businesses moving.

This shift isn't just about changing preferences; it’s a smart response to new economic realities and government incentives. Lenders are adapting their products to meet this demand, creating specialised pathways for businesses to invest in electric fleets or lock in great terms on pre-owned gear. Understanding these options is the key to making savvy buying decisions.

The Green Revolution in Asset Acquisition

Sustainability is no longer a buzzword—it's a core business strategy. Driven by eye-watering fuel costs, handy government incentives, and a genuine desire to lower their environmental impact, Aussie businesses are increasingly looking at electric and hybrid vehicles. This isn't just a small trend; it's a massive market movement backed by serious money.

The numbers really tell the story. According to the Australian Finance Industry Association (AFIA), Australia's electric and hybrid vehicle finance sector hit an incredible $6.17 billion in new business value. That's a massive 50% jump from the previous year. This boom funded the purchase of 104,835 electric and hybrid vehicles, showing a clear shift in how businesses are thinking about their fleets. You can dig into the full EV report from AFIA to see these market dynamics for yourself.

This growth is being supercharged by attractive incentives that make financing green assets particularly appealing. Things like novated leasing for EVs can offer substantial tax benefits, which can make the total cost of ownership incredibly competitive against traditional petrol or diesel models. Lenders have clocked this and are now rolling out specific products tailored for these sustainable assets.

Why Businesses Are Embracing Sustainable Finance

- Reduced Operating Costs: Less spent on fuel and maintenance for electric vehicles means a healthier bottom line over the life of the asset. It’s that simple.

- Government Incentives: Tax breaks, rebates, and exemptions on things like the Fringe Benefits Tax (FBT) for eligible EVs make the financial case even stronger.

- Enhanced Brand Reputation: Running a green fleet shows you’re a responsible corporate citizen, which can attract both customers and top talent who care about sustainability.

- Future-Proofing Operations: Investing in low-emissions tech gets your business ready for stricter environmental rules down the track and positions you as a forward-thinking leader.

The Enduring Power of the Used Asset Market

While sustainable technology is clearly the future, the market for used vehicles and equipment remains a powerful force right now. For startups, sole traders, and any business managing a tight budget, financing pre-owned assets is just a smart, practical strategy. It allows them to get essential, high-quality gear without the hefty price tag of a brand-new model.

Buying used doesn't mean settling for second-best. It’s all about maximising value and getting proven, reliable tools working for you quickly and affordably. Whether it's a five-year-old prime mover or a specialised piece of manufacturing equipment, a well-maintained used asset can deliver an exceptional return on investment.

Navigating the used equipment market is where a skilled broker truly shines. They know which lenders have an appetite for older or more specialised assets and can structure a deal that secures favourable terms, turning a potential financing challenge into a straightforward approval.

Lenders have developed specific finance products just for the second-hand market. While they might have rules around the age of the asset at the end of the loan term, the process is often just as smooth as financing something new. This flexibility is vital, ensuring that every business, no matter its size or capital, has a pathway to get the tools it needs to compete and grow.

Navigating the Application and Documentation Process

Applying for vehicle and equipment finance can sometimes feel like you’re trying to solve a puzzle, but once you understand the steps, it’s far more straightforward. The whole point of the application is to give the lender a clear picture of your business's financial health, making sure the loan structure is a good fit for your ability to make repayments.

It all starts with getting your paperwork together. For businesses that have been around for a while, this usually means a 'full-doc' application, which is just industry-speak for providing a complete financial snapshot. It might sound like a lot, but it’s a standard process that paves the way for a smooth approval.

What Lenders Look for in a Full-Doc Application

A full-documentation, or full-doc, application is the traditional path to getting financed. It’s all about using detailed financial records to prove your income and show that your business is stable. Think of it as telling your company's complete financial story.

Lenders will ask for a standard set of documents to review your application. Having these ready to go can seriously speed things up.

Key documents usually include:

- Recent Financial Statements: Your Profit & Loss statement and Balance Sheet are crucial here, as they show your business's profitability and overall net worth.

- Up-to-Date Tax Returns: It’s standard to provide both personal and business tax returns for the last one or two financial years.

- Business Activity Statements (BAS): Lenders use your recent BAS submissions to help verify your reported business turnover.

This information gives the lender confidence that your business generates enough consistent income to comfortably handle the new loan repayments. While it’s a thorough check, it’s the most direct way to lock in competitive terms if you have your paperwork in order.

Low-Doc and No-Doc Solutions for Modern Businesses

But what happens if your financial records aren't so black and white? For sole traders, new businesses, or self-employed professionals, coming up with two years of squeaky-clean financials isn’t always realistic. This is where low-doc and no-doc vehicle and equipment finance options are an absolute game-changer. 🛠️

It's important to know that these aren't "no-questions-asked" loans. They are simply more flexible solutions that use different ways to verify your income. Lenders get it—a strong, profitable business isn't always reflected in a neat set of tax returns.

Low-doc finance isn’t about hiding information; it’s about presenting your financial strength in a different way. It’s a practical solution for businesses whose story isn’t told through standard paperwork.

Instead of tax returns, a lender might look at:

- Business Bank Statements: Typically 6 to 12 months' worth to show a steady flow of cash.

- An Accountant’s Letter: A signed declaration from your accountant confirming your income.

- Recent BAS Lodgements: A great way to provide a snapshot of your recent turnover.

These options open up a path to finance for businesses that are otherwise healthy and successful. For a deeper dive into the different loan pathways available, check out our guide on how to get a business loan. This flexibility is vital in Australia's dynamic market, where affordability is everything. For example, used vehicles captured a massive 66.13% of the automotive financing market as businesses looked for more cost-effective solutions. You can read the full analysis from Mordor Intelligence to learn more about this trend.

Pathways for Applicants with a Challenging Credit History

A few bumps in your credit history don’t have to be a dead end. While a perfect credit score is always nice, many specialist lenders are willing to look at the bigger picture and offer 'second-chance' financing.

Your financial past is part of the story, but lenders are often just as focused on your future potential. They’ll assess the overall strength of your application, looking for positive signs that can balance out a less-than-perfect credit score. Your story doesn't have to be perfect to get the assets your business needs.

Several things can strengthen your application, even with past credit issues:

- A Solid Deposit: Putting down a larger deposit reduces the lender's risk and shows you’re serious about the purchase.

- A Quality Asset: Financing a high-quality, in-demand vehicle or piece of equipment gives the lender strong security.

- Demonstrated Repayment History: If you can show you've managed other financial commitments well, it builds a lot of confidence.

- A Clear Explanation: Being upfront about past credit issues and explaining what happened can often work in your favour.

Ultimately, getting your application across the line is about presenting the strongest possible case for your business. With the right guidance, you can find a lender whose criteria match your unique circumstances, helping you secure the funds needed to drive your business forward.

How to Choose the Right Lender and Secure the Best Deal

Getting a 'yes' from a lender is one thing, but getting the right finance deal for your business is something else entirely. It’s easy to get drawn in by the lowest interest rate, but that number rarely tells the whole story. The best deal is the one that actually fits your cash flow, supports your tax strategy, and helps you hit your long-term goals.

Making a smart decision means looking past the headline rate to understand the total cost of the loan. This includes establishment fees, ongoing account charges, and how any balloon or residual payment is structured at the end. A few seemingly small fees can really add up over the life of a loan.

Banks vs Specialist Brokers

When you need finance, your first instinct might be to walk into your local bank branch. It's familiar, but it's also incredibly limiting. Your bank can only offer you its own products, which might not be the most competitive or suitable for what you need—especially if you're after a low-doc solution.

This is where partnering with a specialist finance broker changes the game completely. A broker isn’t a salesperson for one institution; they're your advocate in the market. Their entire job is to navigate the complex lending landscape for you and find the perfect match for your business.

Using a specialist broker gives you access, expertise, and negotiation power you simply can't get on your own. They translate your unique business scenario into a compelling application that the right lenders will want to fund.

This kind of expert guidance is priceless, especially for more complex situations. If you're a new business, have a few bumps in your credit history, or need a low-doc equipment loan, a good broker knows exactly which lenders specialise in these areas. This saves you from firing off multiple applications that could actually damage your credit score.

Key Advantages of Using a Broker

- Massive Lender Access: A broker like Diamond Lending works with dozens of banks and non-bank lenders. This gives you a bird's-eye view of the market’s best offers, all in one place.

- Serious Negotiation Power: Brokers handle a huge volume of loans, giving them the leverage to negotiate for better interest rates and more flexible terms on your behalf.

- Solutions That Actually Fit: They have the expertise to match your unique financial story—like needing flexible repayments or a low-doc application—with the product that makes the most sense.

Critical Questions to Ask Your Lender or Broker

To feel truly confident in your decision, you need to ask the right questions. Being prepared helps you compare offers properly and avoid nasty surprises down the track. Think of this as your final checklist before signing anything. ✅

- What is the total cost of the loan? Get a full breakdown, including all establishment fees, ongoing charges, and any other hidden costs.

- Are there penalties for early payout? If you have a great year, you might want to clear the debt early. Make sure you know if it's going to cost you.

- Can we customise the repayment schedule? For businesses with seasonal cash flow, like in agriculture or tourism, matching payments to your busy periods can be a massive relief.

- What happens at the end of the loan term? Clarify your options for any balloon or residual payment. Can it be refinanced if needed?

- How is the interest rate structured? Is it fixed for the whole term, or is it a variable rate that could creep up later on?

By asking these questions and weighing up your options, you can lock in a vehicle and equipment finance deal that doesn't just get you the asset you need—it acts as a smart, strategic building block for your business's future.

Your Asset Finance Questions, Answered

Stepping into the world of vehicle and equipment finance can feel a little complex. To make things clearer, we've put together straightforward answers to the questions we hear most often from Australian business owners just like you.

Can I Claim the Instant Asset Write-Off With Equipment Finance?

Yes, you often can—it just depends on the finance structure you choose. If you go with a product where you take ownership of the asset from day one, like a Chattel Mortgage, you're generally able to claim government incentives like the instant asset write-off.

This is a huge win for your tax planning, allowing you to claim an immediate deduction for the business portion of the asset's cost. On the other hand, for finance leases where the lender technically owns the asset, you'll typically claim the lease payments as a tax deduction instead. It's always a good idea to chat with your accountant to make sure your finance choice lines up perfectly with your tax strategy.

What Is a Balloon Payment and Is It a Good Idea?

Think of a balloon payment (sometimes called a residual) as a lump-sum payment you agree to make at the very end of your loan term. The main benefit? It makes your regular monthly repayments much lower, which is fantastic for keeping your business cash flow healthy.

When the loan term ends, you’ve got options. You can pay out the balloon and own the asset outright, refinance the balloon amount into a new loan, or simply trade the asset in. It’s a powerful tool for businesses wanting to minimise monthly costs or for those who plan to upgrade their gear every few years anyway. The only catch is making sure you've planned for that final payment.

A balloon payment is a strategic lever to improve your month-to-month cash flow. By deferring a portion of the asset's cost to the end of the term, you make the finance more affordable during its working life.

Can I Get Finance for Both New and Used Equipment?

Absolutely. Financing used vehicles and equipment is incredibly common, and lenders are well set up for it. For many businesses, it’s a smart, cost-effective way to get the tools you need without the brand-new price tag.

Lenders might have a few conditions for used goods, like a maximum age for the asset by the time the loan term finishes. This is where a good broker really shines—they know exactly which lenders have flexible policies for older or more specialised used assets, saving you the runaround.

Does Applying for Asset Finance Hurt My Credit Score?

Every time you formally apply for finance, it creates what’s known as a hard inquiry on your credit file, which can nudge your score down a little temporarily. This is why shotgunning applications to multiple lenders at once isn't a great strategy.

Working with a broker helps you avoid this. We can assess your situation against our whole panel of lenders with an initial soft check, which doesn't impact your score. We then submit a single, formal application to the lender who is the best fit, which minimises hits to your credit file while giving you the strongest chance of approval.

Ready to secure the assets your business needs to grow? The team at Diamond Lending has access to a wide panel of lenders and the expertise to find the right vehicle and equipment finance solution for you. Start your journey with a quick assessment today.