In Melbourne's fast-paced property market, grabbing a great opportunity often comes down to one thing: securing fast, flexible finance. Waiting for a bank to say "yes" can mean watching that perfect deal slip through your fingers.

This is where private lending solutions in Melbourne come in. They offer a powerful alternative to the slow-moving banks, providing asset-backed loans for developers, investors, and business owners who need to act decisively. This guide is your roadmap to understanding exactly how this funding works.

Unlock Your Next Project with Private Lending

When it comes to Melbourne real estate and business, timing is everything. You might be facing a tight settlement deadline, need urgent funds for construction, or have a chance to snap up a prime development site. In these moments, traditional bank loans often move too slowly.

Bank application processes are notoriously rigid, demanding mountains of paperwork and taking weeks, or even months, for approval. It’s a major roadblock. For this reason, private lending has become a strategic financial tool, not just a last resort.

Private finance is built for situations where speed and flexibility are non-negotiable. Instead of getting bogged down in historical income documents and perfect credit scores, private lenders focus on what matters most: the value of the underlying asset, which is usually real estate. This asset-first approach allows them to make faster decisions and offer far more adaptable terms.

Who Benefits from This Approach?

This guide will cut through the financial jargon and give you clear, actionable insights into how private lending can be a game-changer for Melbourne's most ambitious players. Let’s look at who stands to gain the most:

- Property Developers: Need to secure funding for land banking, cover construction costs, or get bridging finance between project stages? A private loan can get you moving without the delays you’d expect from a major bank.

- Business Owners: You can unlock the equity tied up in your commercial or residential property to inject working capital, fund an expansion, or manage cash flow gaps—even if your income streams are complex.

- Property Investors: Got your eye on an auction purchase or facing an urgent settlement? A short-term loan lets you secure the property now and worry about refinancing with a traditional lender later.

Private lending isn't about replacing banks. It's about providing a specialised solution for those time-sensitive, opportunity-driven scenarios where conventional funding simply can't keep up.

Navigating the world of non-bank lenders requires a bit of know-how. This is where a specialist broker becomes essential, connecting you with reputable private lending solutions in Melbourne that are a perfect match for your specific needs. A good broker handles the complexities, negotiates the terms, and manages the entire process from application to settlement. They turn potential financial headaches into successful project outcomes.

Throughout this guide, we'll show you exactly how it’s done.

How Private Finance Actually Works in Melbourne

To really get your head around private lending, it helps to first think about how a traditional bank operates. A bank loan is like a rigid, pre-built highway—you either meet its exact on-ramp requirements for income, credit history, and paperwork, or you're stuck on the side of the road. There’s almost no room for negotiation or unique circumstances.

Private finance, on the other hand, is more like a custom-built bridge. It’s designed specifically to get you over a unique financial obstacle, whether that's a tight settlement deadline or a complex development project. The whole process is different because the decision-makers and their priorities just aren't the same as a bank's.

The Key Players and Their Focus

The lenders in this space are not your typical high-street banks. They are generally sophisticated investors, including:

- High-Net-Worth Individuals: Private citizens with significant capital who lend it out for a return.

- Family Offices: Private wealth management firms that look after the financial affairs of ultra-high-net-worth families.

- Investment Funds: Specialised funds that pool money from multiple investors to provide debt financing.

What unites these lenders is their core focus. They operate on an asset-first lending model. This simply means that instead of obsessing over a borrower's historical tax returns or a flawless credit score, they prioritise the quality and value of the security property.

This asset-centric approach is the engine that drives the speed and flexibility of private lending in Melbourne. The key question for a private lender isn't "Does the borrower's paperwork fit our rigid criteria?" but rather, "Is this a quality asset with a strong valuation and a clear path for loan repayment?"

This completely different perspective allows them to approve loans that banks would automatically reject. For Melbourne's property developers and business owners, this opens up a vital funding channel when traditional options are off the table.

The Anatomy of a Typical Private Loan

Because they’re designed for specific, time-sensitive purposes, private loans have a distinct structure compared to a standard 30-year bank mortgage. Understanding these features helps clarify why they’re used as a strategic tool rather than a long-term financing commitment.

Key characteristics usually include:

- Short Loan Terms: Most private loans are set up for terms ranging from six to 24 months. They are not meant to be held for decades; they are a bridge to get you to your next financial milestone.

- Interest-Only Payments: Borrowers typically only pay the interest each month, not the principal. This keeps monthly repayments lower and preserves cash flow, which is often crucial for a business or development project.

- Emphasis on the Exit Strategy: A clear and credible plan for repaying the loan at the end of the term is non-negotiable. This "exit strategy" could be refinancing with a traditional bank, selling the property, or using incoming funds from another source.

- Higher Interest Rates: The rates are higher than those of major banks. This premium accounts for the increased risk, the custom nature of the loan, and the incredible speed at which funds can be delivered—sometimes in a matter of days.

This structure is purpose-built for the dynamic nature of Melbourne's property and business sectors. It provides the capital needed to seize an opportunity quickly, with the understanding that the borrower will transition to more conventional financing once their immediate goal is achieved. It’s a model built for speed, agility, and overcoming obstacles.

Why Private Credit Is a Mainstream Funding Channel

Not so long ago, private credit was seen as a niche corner of the finance world. Today, that couldn't be further from the truth. It's now a significant and essential part of Australia's funding ecosystem—a mature, reliable source of capital for savvy developers, investors, and business owners.

This shift didn't happen by accident. It's a direct response to how traditional banks have changed their game.

Over the past decade, the major banks have steadily tightened their lending rules, especially for commercial real estate and development finance. Weighed down by heavier regulations and a lower appetite for risk, they’ve created a massive funding gap. This is the space where private credit hasn't just stepped in but has absolutely thrived, providing the liquidity the market desperately needs.

This national trend is fantastic news for Melbourne’s dynamic property market. It gives entrepreneurs and developers a powerful and accessible alternative to get their projects funded and off the ground, even when the banks say "no."

The Explosive Growth of a New Asset Class

The sheer scale of this market shift is staggering. Private credit in Australia is no longer a small-scale operation; it's a sector managing immense pools of capital. This explosive growth proves its legitimacy and staying power as a mainstream funding channel.

Recent industry data tells the story. Australia's private credit market has ballooned to an estimated AU$205 billion in assets under management. This is broken down into AU$120 billion for business-related lending—covering everything from corporate loans to SME working capital—and another AU$85 billion in commercial real estate loans. For a deep dive, check out the Australian Private Debt Market Review.

This isn't just a fleeting trend; it's a fundamental rewiring of our financial landscape. Private credit is now a cornerstone of project funding in Australia, directly fuelling economic activity and development in cities like Melbourne.

What does this influx of capital mean for you? It means more options and greater certainty. When you seek private lending solutions in Melbourne, you’re tapping into a deep and well-established market, not some fringe financial service.

Why This Matters for Melbourne Borrowers

The evolution from a niche product to a mainstream channel brings real, tangible advantages. The maturity of the private credit market has created a far more professional and structured lending environment than ever before.

For borrowers in Melbourne, this translates into several key benefits:

- More available capital: A greater supply of funds and more lenders in the market creates healthy competition. This can lead to better terms and more specialised loan products, ensuring that even large-scale construction projects have access to the funding they need outside the restrictive banking system.

- Greater reliability and professionalism: The sector's growth has attracted sophisticated institutional investors. This professionalisation brings a higher degree of reliability and transparency to the process. You can have confidence that you're dealing with established lenders who genuinely understand the nuances of the Melbourne property market.

The result is a funding ecosystem that is not only faster and more flexible but also robust and dependable, ensuring ambitious projects across the city have a viable path to completion.

Who Really Uses Private Lending in Melbourne?

When you move past the theory, you start to see where private finance truly makes a difference in the real world. In Melbourne's fast-paced property and business scene, certain challenges pop up that just can't be solved by a trip to the bank.

The typical person seeking a private loan isn't someone with bad financial habits. More often than not, they’re savvy operators caught in a timing crunch that the big banks simply aren’t built to handle. They're the developers, business owners, and investors who get it: the cost of a missed opportunity is always higher than the interest rate on a short-term loan.

Let's look at a few real-world situations where private lending solutions in Melbourne become the perfect strategic move. 🏗️

The Opportunistic Property Developer

Picture a seasoned property developer. They've just stumbled upon a prime block of land in a booming Melbourne suburb like Point Cook or Craigieburn and know it's a goldmine. The problem? Another developer is sniffing around, too.

Going to a bank means wading through months of paperwork and waiting for committee approvals. By then, the opportunity will be a distant memory. This is where private lending provides a serious competitive edge. The developer needs to lock down that site, and they need to do it now.

- The Challenge: An urgent need for cash to snap up a valuable development site before a competitor does.

- The Private Lending Solution: A short-term land bank loan is approved in under a week, secured against the property itself. This gives the developer the firepower to exchange contracts immediately.

- The Outcome: With the site secured, the developer can now manage council approvals and development plans without the pressure. They have a clear exit strategy: refinance with a traditional construction loan once the plans are rubber-stamped. Private credit was the key that unlocked the entire deal.

The Self-Employed Business Owner

Now, think of a successful Melbourne manufacturing business. The owner has a golden opportunity to buy new machinery that will boost production by a massive 40%. But their income documents are messy. Revenue is seasonal, and their latest tax return doesn't quite capture the company's recent growth spurt.

A major bank takes one look at the fluctuating income and says "no," completely ignoring the significant equity the owner has in both their factory and their home.

For the self-employed, private lending is a bridge to their own wealth. It lets them tap into the equity they've built in their properties without being forced into the rigid, one-size-fits-all income verification boxes that traditional lenders love.

This business owner used a private loan, secured against their commercial property, to get the cash injection they needed. They bought the machinery, ramped up production, and watched their profits soar. Once their next set of financials proved the uplift, refinancing back to a mainstream bank was a walk in the park.

The Strategic Property Investor

Here’s another classic scenario. A sharp property investor has just won a bidding war for a highly sought-after apartment at a weekend auction in South Yarra. They've paid the deposit but now have a nail-biting 30-day settlement deadline.

Their bank is dragging its feet on the final finance approval, putting their entire 10% deposit on the line if they can't settle in time. Walking away isn't an option—it means losing the deposit and facing potential legal action.

- The Challenge: A terrifyingly tight settlement deadline that a traditional lender just can't meet.

- The Private Lending Solution: A fast bridging loan. This type of loan is purpose-built to "bridge" the gap between buying a property and lining up long-term finance.

- The Outcome: The private loan is approved and funded in just a few days. The investor settles on time, stress-free. They can then take their time arranging a standard investment loan from their bank to pay out the bridging finance, having protected their deposit and secured a fantastic new asset.

Financing Commercial Real Estate Projects

When it comes to Melbourne's commercial real estate (CRE) scene, private lending isn't just an alternative anymore—it's become a genuine game-changer. Developers and investors are increasingly leaning on non-bank finance for everything from snapping up land and funding construction to refinancing established commercial assets. This isn't just a trend; it's a direct response to the major banks taking a big step back from the CRE market.

That retreat has left a huge funding vacuum, and private credit has stepped in enthusiastically to fill it. For Melbourne's commercial property players, this translates to fast, flexible capital that keeps projects alive and kicking, especially when the banks can't—or won't—play ball. It’s fundamentally changing how big-ticket commercial deals get across the line.

The Growing Gap in Commercial Lending

For years, if you had a commercial project, you went to a major bank. That was the default. But a perfect storm of tighter regulations and a lower appetite for risk has seen them drastically wind back their involvement, leaving many perfectly good projects stranded without a clear funding path.

Private credit has thrown a lifeline to the commercial real estate sector, stepping in where the big banks have slashed their exposure by a staggering 50% since 2009. This has opened up a massive US$33-56 billion opportunity for non-bank lenders. In fact, industry analysis suggests that by the end of the year, private credit is set to command about 16% of all CRE lending, a slice of the pie worth around US$50 billion nationwide. You can dig deeper into this market shift in this Knight Frank report on private credit growth.

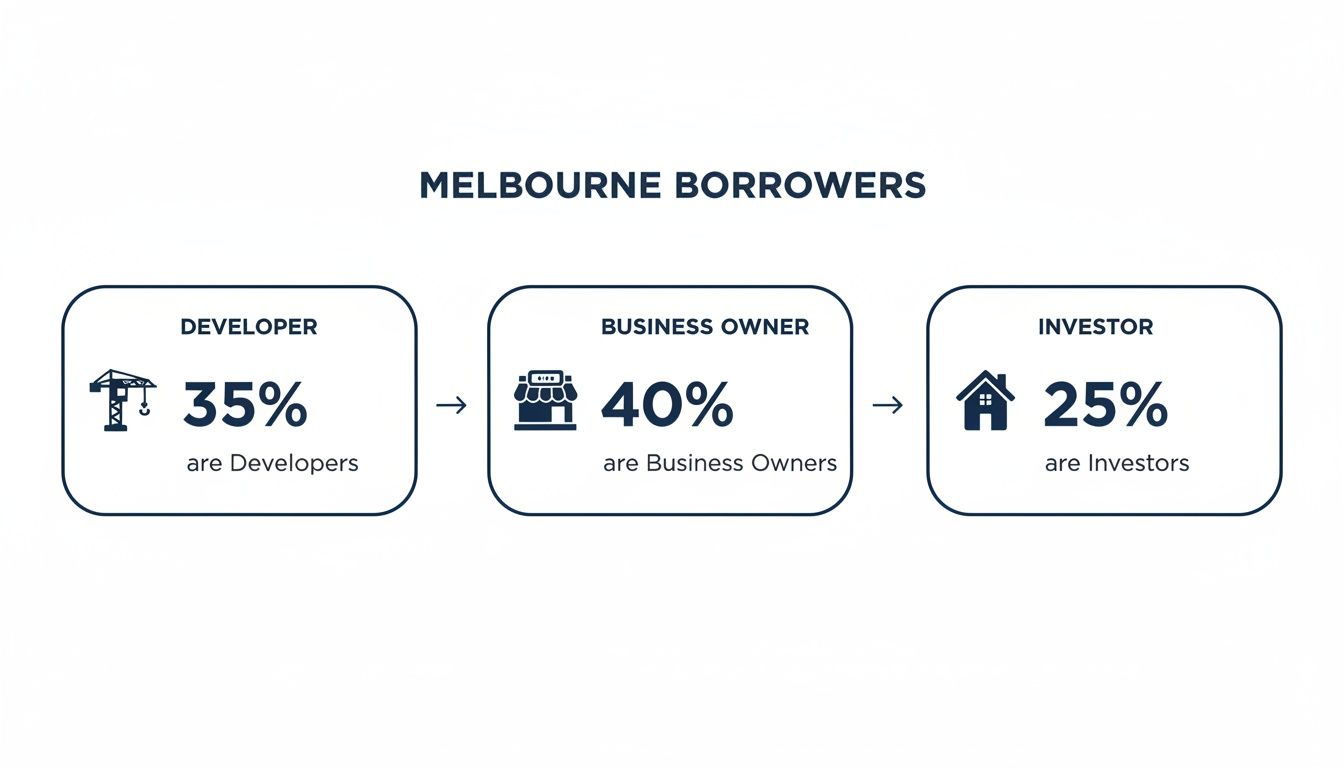

So, who in Melbourne is tapping into these specialised funding solutions?

As you can see, it’s a healthy mix. Business owners, developers, and investors are all making up a significant chunk of the demand for private lending, each with their own unique needs and timelines.

Bank vs Private Loans for Melbourne Commercial Real Estate

To really grasp the difference in practice, it helps to see the two funding options side-by-side. The choice often boils down to a classic trade-off: speed and flexibility versus cost and loan term. For many, though, the strategic upside of moving quickly with a private loan far outweighs the higher interest rate.

For a more detailed breakdown of financing options, have a look at our comprehensive guide to commercial property loans in Melbourne.

The table below cuts straight to the key distinctions.

| Feature | Traditional Bank Loan | Private Lending Solution |

|---|---|---|

| Approval Speed | Slow (typically 1-3 months) | Fast (often 1-2 weeks) |

| Documentation | Extensive financial history required | Focused on asset and exit strategy |

| Loan Purpose | Strict, often for stabilised assets | Flexible for land, construction, and bridging |

| Decision Focus | Borrower's credit and serviceability | Property value (LVR) and project viability |

| Loan Term | Long-term (5-30 years) | Short-term (6-24 months) |

| Flexibility | Rigid terms and conditions | Customised loan structures |

| Ideal For | Standard purchases of income-producing properties with ample time for approval. | Time-sensitive acquisitions, development projects, or when bank criteria cannot be met. |

The crucial takeaway here is that private lending is purpose-built for scenarios where the cost of waiting is high. Securing a prime commercial site or getting a profitable development off the ground quickly often delivers a return that makes the cost of a short-term private loan a very smart business decision.

Ultimately, private CRE finance doesn't replace bank lending; it's a specialised tool for a specific job. It provides the agility needed to seize opportunities in Melbourne's competitive commercial market, bridging the gap until a project is finished or stable enough to qualify for traditional, long-term bank funding.

Your Path to Securing a Private Loan

Diving into the world of private finance might feel like a big step, but with the right guidance, it’s a surprisingly straightforward process. Forget the long, drawn-out journey you might expect from a traditional bank. Securing private lending solutions in Melbourne is built for one thing: speed. The key is having a clear, structured game plan, which is exactly where an expert broker proves their worth.

Think of an experienced broker as your guide through the process. They simplify every stage, handle the complex details, and let you focus on your project. They take your funding needs and turn them into a compelling case that private lenders understand, creating a smooth path from your first call right through to settlement.

The entire process really breaks down into a few logical steps.

Step 1: Initial Consultation and Strategy

It all starts with a conversation. This isn't about filling in forms; it's a strategy session to map out your goals, the property details, and your required timeline. The main goal here is to get to the heart of your "why"—what opportunity are you chasing, and what does a successful outcome look like for you?

From there, your broker will outline a clear path forward. This includes pinpointing the right type of loan for your situation and, just as importantly, confirming your exit strategy. That’s your plan to repay the loan at the end of the term. This planning phase is critical for matching your needs with the perfect lender from day one. To get a better handle on this specialised field, take a look at our guide on Melbourne private lending specialists.

Step 2: Gathering the Essential Documents

You can forget the mountains of paperwork banks demand. Private loan documentation is much more streamlined because the lender’s focus is squarely on the asset, not your entire financial history. While the specifics can vary a little between lenders, you’ll generally need to provide:

- Identification: Standard proof of identity for everyone involved.

- Property Details: The contract of sale or a council rates notice for the property you’re using as security.

- A Clear Exit Strategy: Proof of how you plan to pay back the loan (this could be a refinancing offer from another lender or a sales agency agreement to sell the property).

Your broker helps you pull all this together quickly, ensuring your application is clean, complete, and ready for a fast decision.

The simplicity of the paperwork is a huge reason why private lending moves so quickly. Lenders are focused on the quality of your asset and the logic of your plan, which allows them to give you a 'yes' or 'no' in days, not drag it out for months.

The Final Steps to Funding

Once your application is in, the last few stages happen fast. Your broker takes your case to a handpicked panel of lenders who are the right fit for your scenario. They negotiate the terms on your behalf and come back to you with the best offers on the table.

After you accept a conditional offer, a sworn valuation of the security property is ordered. Assuming the valuation comes back strong, the lender issues the formal loan documents for you to sign. The final step is settlement. The funds are transferred, and you can secure your property or kick-start your project without missing a beat.

Common Questions About Private Lending in Melbourne

Let's wrap up by tackling some of the questions we hear most often. These are the practical, real-world queries that pop up when you're considering a private loan, and getting clear answers is key to feeling confident about the process.

How Quickly Can I Actually Get a Private Loan Funded?

This is where private lending really shines. While a typical bank loan can drag on for months, a private loan often settles in just a matter of days or weeks, depending on how straightforward the deal is.

In a real pinch—like when you need to secure a property at auction or meet a looming settlement deadline—funding can sometimes be organised in as little as 48 to 72 hours once the property valuation is complete. An experienced broker is your best asset here, as they have direct lines to lenders known for their speed and can push your application through to meet that urgent deadline.

Are the Interest Rates on Private Loans Always High?

Yes, private lending rates are higher than what the big banks offer. There's no getting around that. This premium covers the lender's risk and pays for the incredible speed and flexibility you get—especially when your situation doesn't fit neatly into a bank's rigid boxes.

But it's better to think of this cost as a strategic tool rather than just an expense. This type of finance allows you to jump on profitable opportunities that would otherwise be lost, like snapping up an undervalued property or funding a development that promises a huge return. These are short-term solutions, designed to be paid out or refinanced as soon as your immediate goal is achieved.

The core idea is simple: the profit you stand to make from seizing the opportunity should far outweigh the cost of the short-term finance. It’s a calculated business decision where the cost of a missed opportunity is always greater than the interest rate.

What Is the Single Most Important Factor for Loan Approval?

Without a doubt, it's the security property. The quality, location, and value of the real estate you're offering as security are everything. Private lenders work on an "asset-first" model, which means their primary concern is the Loan-to-Value Ratio (LVR) and the strength of the property itself.

This is precisely why a solid property in a good Melbourne suburb can often overcome issues that would be an instant "no" from a major bank. Things like patchy income documents or a small mark on your credit history become far less important when the real estate backing the loan is strong.

Why Is a Clear Exit Strategy So Crucial?

Your exit strategy is your plan for paying back the loan when the term is up. Because these aren't 30-year mortgages, lenders need to know—with total certainty—that you have a clear and realistic way to repay them.

Having a well-thought-out exit strategy isn't just a suggestion; it's a non-negotiable for getting approved. The most common and effective exit strategies include:

- Refinancing: Moving the loan over to a traditional bank once a project is finished or the property's value has increased.

- Property Sale: Selling the security property and using the proceeds to clear the debt.

- Business Proceeds: Using cash flow from another successful business operation or project to pay out the loan.

Ready to see how Diamond Lending can connect you with the right private lending solution for your next Melbourne project? Our team specialises in sourcing fast, flexible funding for property developers, investors, and business owners. Start your journey with a quick chat today by visiting https://diamondlending.com.au.