A machinery finance broker is essentially your business's secret weapon for getting the funding you need for essential equipment. They act as a specialist guide, connecting you to a whole network of lenders to find the best possible deal on financing for assets like excavators, tractors, or manufacturing machinery.

What a Machinery Finance Broker Actually Does

Think of a machinery finance broker like a real estate buyer's agent, but for business equipment. Instead of you spending countless hours approaching different banks and lenders one by one—and filling out endless forms—a broker does all the heavy lifting for you. They live and breathe the world of asset finance.

Their first job is to get a handle on your business, its specific needs, and your financial situation. From there, they tap into their established relationships with a wide panel of lenders—including the major banks and specialist non-bank institutions you've probably never heard of—to source the most suitable and competitive finance options available.

Your Advocate in the Lending Market

A broker doesn't just find loans; they champion your application. They know exactly what each lender is looking for and how to present your business in the best possible light, which massively boosts your chances of getting a "yes". This is especially valuable for self-employed individuals or businesses that don't neatly fit the rigid criteria of the big banks.

A great broker saves you more than just money on interest rates. They save you time, reduce the stress of complex paperwork, and unlock funding opportunities you likely wouldn't find on your own.

Essentially, they handle the entire process from the first enquiry right through to settlement. This frees you up to acquire the critical assets you need for growth without draining your precious cash reserves. Their real value is in simplifying a complex process, providing expert guidance, and delivering financial solutions that are actually aligned with your operational goals.

By partnering with a machinery finance broker, your business gains:

- Access to More Lenders: They connect you to a diverse market well beyond just the big four banks.

- Expert Negotiation: Brokers work on your behalf to secure better rates and more favourable terms.

- Time-Saving Convenience: They manage the paperwork and application process, letting you focus on running your business.

- Specialised Knowledge: They understand the nuances of financing different types of machinery across all sorts of industries.

Decoding Your Machinery Finance Options

When you're looking to fund new machinery, the world of finance can feel a bit like a foreign language. You'll hear terms and see structures that aren't always crystal clear, which is exactly where a machinery finance broker steps in. Think of us as your translator—we clarify the options so you can choose the right path for your business's growth and cash flow.

Let's break down the most common products you'll come across in Australia. Each one is built differently, and that affects everything from who actually owns the equipment to how it appears on your balance sheet. Getting your head around these differences is the key to matching your finance with your long-term business goals.

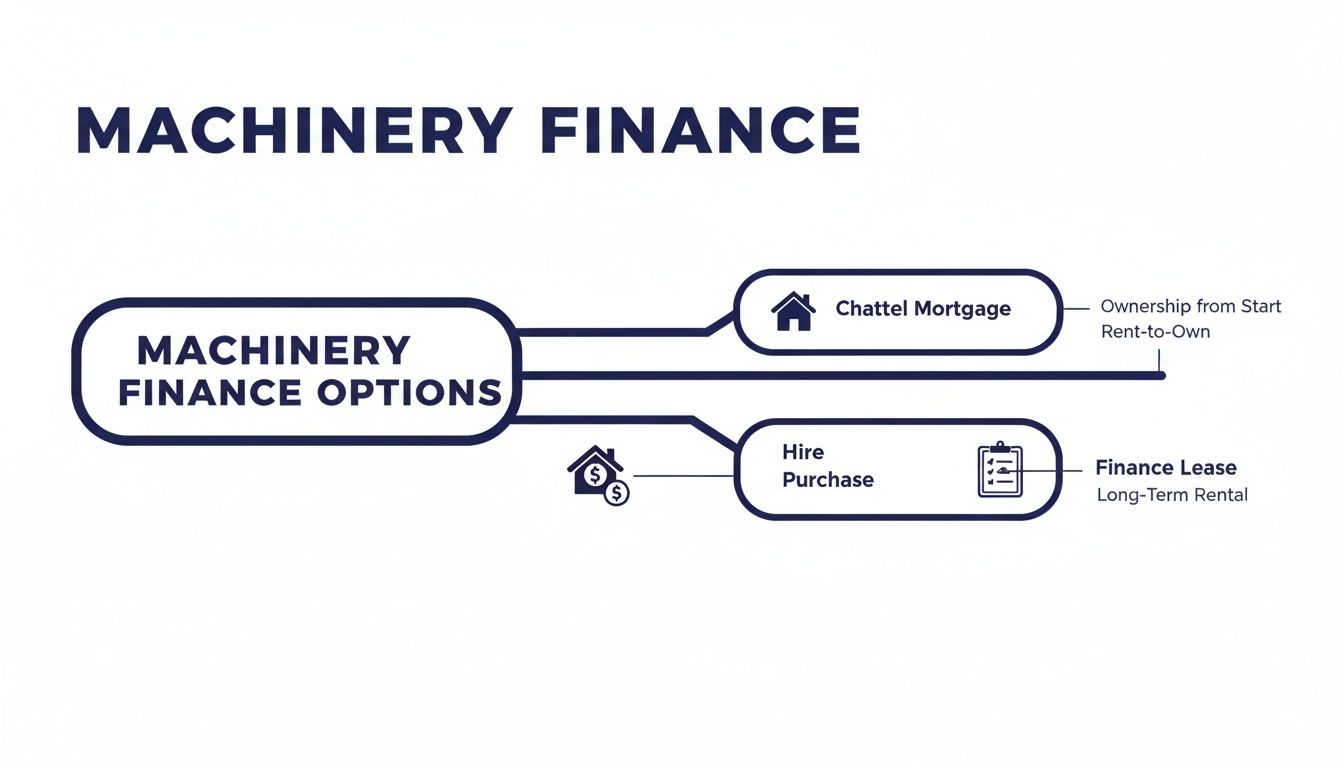

Chattel Mortgage

A chattel mortgage is probably the most straightforward and popular option, and for good reason. It works a lot like a traditional home loan, but for a business asset instead of a house. Your business buys and takes ownership of the machinery from day one, and the lender simply takes a mortgage over that equipment as security.

This structure is a favourite among Australian businesses because it offers some powerful advantages:

- You Own It Immediately: The asset goes straight onto your balance sheet from the get-go.

- Serious Tax Perks: If you're registered for GST, you can often claim the entire GST portion of the purchase price back on your next Business Activity Statement (BAS).

- Claim Depreciation: As the owner, you can claim depreciation on the asset, and the interest you pay on the loan is also a tax deduction.

Hire Purchase

A hire purchase is best understood as a 'rent-to-own' model. With this arrangement, the finance company buys the machinery you need on your behalf. Your business then hires it from them for a fixed term, making regular payments along the way.

Once you make that final payment, the ownership of the asset officially transfers to you. It's a great option for businesses that want a simple and direct path to ownership without having to find a huge amount of capital upfront.

A hire purchase is brilliant for preserving your working capital. It spreads the cost over time, giving you full use of the equipment while you pay it off, with the clear goal of owning it at the end.

Finance Lease

A finance lease is essentially a long-term rental agreement. The lender buys the equipment and then leases it to your business for an agreed-upon period in return for regular rental payments. The key difference from a hire purchase is that you don't automatically own the gear at the end of the term.

Instead, when the lease ends, you usually have a few choices. You can pay a final residual amount to take ownership, trade it in for a newer model, or simply extend the lease. This gives you fantastic flexibility, especially if your business needs to regularly update its equipment to stay ahead of the competition.

For a deeper dive, you can explore more about our specific vehicle and equipment finance solutions.

Comparing Machinery Finance Options at a Glance

Choosing between these options can feel complex, but seeing them side-by-side makes the core differences much clearer. This table breaks down how each type of finance impacts ownership, your GST claims, and your balance sheet.

| Finance Type | Ownership | GST Claim | Balance Sheet Impact |

|---|---|---|---|

| Chattel Mortgage | You own the asset from day one. | Claim the full GST on the purchase price upfront (on your next BAS). | The asset and the corresponding loan (liability) appear on your balance sheet. |

| Hire Purchase | The lender owns the asset until the final payment is made. | Claim GST on each rental payment, not the full purchase price at once. | The asset may not be listed on your balance sheet until ownership transfers. |

| Finance Lease | The lender owns the asset throughout the lease term. | Claim GST on each rental payment. | The asset is treated as an operating expense, keeping it off your balance sheet. |

Ultimately, the 'best' option isn't one-size-fits-all. A Chattel Mortgage is often ideal for long-term assets you intend to keep, while a Finance Lease provides flexibility for equipment that needs frequent upgrading. A Hire Purchase offers a simple, structured path to ownership. A good broker will walk you through these nuances to find the perfect fit for your specific business needs.

The Strategic Advantage of Using a Broker

Deciding between your bank and a machinery finance broker might feel like just another item on your to-do list, but it's a choice that can seriously impact your business's bottom line. Working with a broker gives you a powerful strategic edge that goes far beyond simply getting a loan approved.

When you walk into your bank, you're limited to their menu of products—that's it. A broker, on the other hand, opens up an entire marketplace of lenders. This includes the big banks, but also specialist non-bank lenders who live and breathe specific industries like construction, transport, or agriculture and often have far more flexible lending criteria. This access is the key to finding a finance solution that actually fits your business, not the other way around.

Think of a broker as your expert negotiator. They're in your corner, fighting for better interest rates and more favourable terms. They know the market inside out and understand how to package your application to make it attractive to the right lenders, a skill that can save you thousands over the life of the loan.

Maximising Your Approval Odds and Saving Precious Time

One of the biggest headaches for any business owner is the mountain of paperwork and confusing application processes that come with finance. A good broker takes that entire burden off your shoulders, managing the documents and liaising with lenders for you. This frees you up to do what you do best—run your business.

Here’s a real-world scenario we see all the time: a growing construction company needs a new excavator to start a major project. Their bank of 10 years says 'no' because their income has fluctuated recently. Instead of hitting a dead end, they call a machinery finance broker. The broker connects them with a specialist lender who gets the project-based nature of construction. The result? They get a 'yes' in under 48 hours.

This is where a broker’s value truly shines. They dramatically boost your chances of getting approved, especially if you’re self-employed and need a low-doc option that traditional banks often shy away from.

The main finance structures a broker can help you sort through are illustrated below.

Each of these structures—Chattel Mortgage, Hire Purchase, and Finance Lease—has unique benefits, and a broker’s job is to match the right one to your business goals and cash flow. In Australia, the farm and construction machinery wholesaling sector is forecast to hit $21.9 billion by 2025, even with recent dips in demand. For SMEs trying to grow in this environment, a broker is an indispensable partner for navigating the financial landscape. You can dig deeper into the trends shaping the machinery wholesaling industry to see why sharp financing is so critical.

Your Step-by-Step Application Journey with a Broker

Navigating the world of machinery finance can feel like a maze of lender jargon and endless paperwork. But when you work with a broker, that complex journey turns into a clear, manageable roadmap.

Think of your broker as the project manager for your funding. They guide you from that first phone call right through to settlement, making sure you know exactly what’s happening and what’s needed next. It’s a structured process designed to get you the keys to your new asset as efficiently as possible.

Let's walk through the typical stages you can expect.

Stage 1: The Initial Discovery Call

It all starts with a simple conversation. This first call isn’t a formal application; it’s a strategic chat about your business, your goals, and the specific equipment you’ve got your eye on.

Your broker will want to understand your operations, get a feel for your financial position, and learn what you’re hoping to achieve with the new machinery. The goal is to build a complete picture of your needs, which allows them to start matching you with the right lenders and products from their network. This foundational step ensures the entire process is aligned with your business from day one.

Stage 2: Gathering Your Documentation

Once your broker understands what you need, it’s time to gather the paperwork. This is where having a broker in your corner really pays off. Instead of guessing what a lender wants, you get a clear, simple list of exactly what’s required, cutting out the frustrating back-and-forth.

For a standard application, you’ll generally need:

- Business Identification: Your Australian Business Number (ABN) and company details.

- Financial Records: This could be your recent financial statements, tax returns, or Business Activity Statements (BAS).

- Director Identification: Standard personal ID for the company directors.

- Asset Details: A quote or invoice for the machine you want to buy.

This is also where a broker’s ability to find low-doc solutions becomes a game-changer. If you’re self-employed and don't have perfect, up-to-date financials, a good broker knows which specialist lenders can help. They can build a strong case with alternative documents—something most major banks simply won't do.

Stage 3: Lender Selection and Settlement

With your application ready to go, your broker gets to work. They’ll submit your file to a shortlist of the most suitable lenders—the ones who understand your industry and are keen to fund your type of asset. This is where their expertise truly shines. 🤝

They use their industry relationships to negotiate competitive rates and favourable terms on your behalf.

Once the offers are in, your broker will present the best options, breaking down the pros and cons of each so you can make an informed choice. After you’ve given the green light, they handle all the final paperwork, coordinating with the lender and the equipment supplier for a smooth settlement. The funds are paid, and you can take delivery of your new machinery, ready to put it to work.

How to Choose the Right Finance Broker

Picking the right machinery finance broker isn't just about finding someone who can get you a loan. It's about finding a partner who genuinely gets your industry and knows what you're trying to achieve with your business. Let's be honest, not all brokers are built the same, so asking the right questions from the get-go is critical.

Your first step should be to properly vet them. Start by digging into their direct experience with your specific field, whether that's construction, transport, agriculture, or manufacturing. A broker who lives and breathes your industry will already understand the cash flow cycles and operational headaches you deal with, which is a massive advantage when they're pitching your application to lenders.

Key Questions to Ask a Potential Broker

Treat your first conversation like an interview—because it is. A quality broker won't just welcome your questions; they'll have clear, confident answers ready to go. Here are the essentials you need to cover:

- What's your experience in my industry? A broker specialising in construction equipment knows exactly which lenders love financing excavators and cranes. Likewise, a transport specialist will have deep connections with funders who really understand the trucking business. You want a specialist, not a generalist.

- How big and diverse is your lender panel? A great broker will have a wide range of lenders on their books, from the major banks to non-bank specialists and even private funders. This diversity is your ticket to better rates and more flexible loan structures.

- Can you give me examples of successful low-doc applications you've handled? This question is a big one, especially if you're self-employed or your financials are a bit complicated. Their answer will tell you everything you need to know about their expertise in getting tricky applications across the line. You can learn more about how an asset finance broker navigates these situations in our detailed guide.

What a Strong Answer Looks Like

A confident broker does more than just list their services; they show you their value. They should be able to talk about specific industry trends and what lenders are looking for right now, proving they have their finger on the pulse. For example, recent analysis from 2025 showed that cautious decision-making among Aussie SMEs was driving the need for brokers who could secure funding that preserved cash flow. The report also confirmed that the construction and transport sectors are still the top users of asset finance, and a knowledgeable broker will know these market dynamics inside and out. You can read the full report on the top industries benefiting from asset financing in 2025.

Ultimately, you’re looking for a strategic partner, not just someone to process paperwork. A great broker will ask you as many questions as you ask them. They’ll dig deep to understand your business before they even think about recommending a solution. That collaborative approach is the hallmark of a broker who is truly invested in seeing you succeed.

A Real-World Broker Success Story

It’s one thing to talk about the benefits of using a machinery finance broker, but seeing how it works in the real world truly brings their value to life. Let’s walk through the journey of ‘Coastline Haulage,’ a small but growing logistics company based in Queensland.

Coastline Haulage was staring at a massive opportunity: a major new contract that would practically double their revenue overnight. The only hurdle? They needed to add a new prime mover to their fleet, and they needed it yesterday. Their first port of call was their long-term business bank, where they naturally expected a simple approval process.

What they got instead was a hard no.

The bank’s rigid, by-the-book credit assessment couldn’t see past their fluctuating income statements—a completely normal part of life in the transport industry. For Coastline Haulage, this wasn't just a minor hiccup; it was a potential deal-breaker that could cost them a game-changing contract.

The Broker Intervention

Feeling cornered, they reached out to a specialist machinery finance broker. The broker instantly got it. He understood the seasonal, project-based nature of the logistics game and knew that historical financials only told half the story.

Instead of just submitting the same old paperwork, the broker built a compelling case for the lender. He highlighted the strength of the new contract, the business's solid operational history, and painted a clear picture of future profitability.

He skipped the major banks altogether and went straight to a specialist lender known for their deep expertise in transport finance. This lender understands the industry's unique cash flow cycles and was completely comfortable with a low-doc application.

Within a few short days, the broker had secured an approval with competitive terms. The finance was settled, Coastline Haulage bought the prime mover, and they were on the road, fulfilling their new contract. This is a perfect example of how a good broker can turn a flat-out 'no' into a major business expansion.

In a tough economic climate, this kind of expert guidance is more critical than ever. With equipment and machinery investment in Australia falling 2.5% in the first quarter of 2025, businesses need a savvy partner in their corner. A skilled broker acts as a financial lifeline, securing vital asset finance that keeps your working capital free for growth. To dig deeper into the numbers, check out the latest Australian industry indicators and capital expenditure trends.

Your Machinery Finance Questions Answered

Even with a clear plan, it's natural to have a few questions before you dive in. Getting finance for your business is a big decision, and you want to be sure you're on the right track.

Think of this section as a quick chat with an expert. We’ll tackle the most common questions we hear from business owners every day, giving you the straightforward answers you need to move forward with confidence.

Can I Still Get Machinery Finance if I Have Bad Credit?

Yes, it’s absolutely possible. While a major bank might see a blemish on your credit file and automatically say no, a specialist broker knows that your credit score is only one part of the story.

We work with a network of non-bank and specialist lenders who look beyond the numbers. They’re more interested in the bigger picture: your recent cash flow, how long you've been in your industry, and the real value of the machine you want to buy. A good broker knows exactly how to frame your application to highlight these strengths, connecting you with a lender who understands your situation and is ready to back you.

How Long Does It Actually Take to Get Approved?

This is one of the biggest advantages of using a broker—speed. When all your documents are ready to go, a straightforward application can often be approved in as little as 24 to 48 hours.

Of course, more complex situations, like a massive funding request or a low-doc application for a self-employed contractor, might take a bit longer. But your broker's job is to chase everything up, make sure your application is perfect from the start, and get it in front of the right person to avoid any unnecessary hold-ups.

The key difference between secured and unsecured funding is collateral. Nearly all machinery finance is secured, meaning the equipment itself acts as security for the loan. This lowers the risk for the lender, which in turn results in more competitive interest rates for your business.

Unsecured loans are much riskier for lenders because there's no asset tied to them, and that's why they come with much higher interest rates. They’re rarely a sensible choice for buying valuable equipment. Your broker will almost always steer you towards a secured option like a Chattel Mortgage or Hire Purchase, as they’re built specifically for buying assets and offer far better value.

Ready to get the right equipment to drive your business forward? The expert team at Diamond Lending is here to navigate the entire process for you, finding the most competitive and suitable finance solution for your needs. Start your journey with a quick, no-obligation chat today.