Securing a home loan when you run your own business can feel like chasing a moving target. In Australia, self-employed borrowers have three main pathways: standard, low-doc and no-doc home loans. Getting to grips with these options is your first step to a successful application.

Navigating Self Employed Home Loans In Australia

Lenders treat irregular earnings like sudden downpours—it’s much safer when you’re prepared. That means thorough, well-organised documentation is non-negotiable.

- Standard Loans demand full tax returns, Notices of Assessment and bank statements.

- Low-Doc Loans accept BAS and an accountant’s letter but come with higher interest rates.

- No-Doc Loans require minimal paperwork in exchange for larger deposits and tighter conditions.

Comparison Of Loan Types For Self Employed

Here’s a side-by-side overview to help you weigh up the options:

| Loan Type | Income Evidence | Application Time | Typical Interest Rates | Ideal For |

|---|---|---|---|---|

| Standard | Full-doc: tax returns, NOA, bank statements | 4–6 weeks | 5.00%–6.00% | Established businesses |

| Low Doc | BAS, accountant letter | 2–4 weeks | 6.50%–7.50% | Newer ventures |

| No Doc | Bank statements only | 1–3 weeks | 7.50%–9.00% | Limited records |

As you can see, documentation, turnaround times and interest rates all shift depending on which loan suits your circumstances best.

Key Policy Updates

Self-employment income climbed 5.5% to $29.5 billion in March 2025, and owner-managers now make up 14% of the workforce. At the same time, Westpac’s move to a one-year income assessment has halved the paperwork burden—fueling a 30% surge in self-employed borrowing last year. Read more about these changes on Westpac’s site: Westpac.

Mortgage Definition Screenshot

Below is a standard mortgage entry from Wikipedia, showing how lenders explain security and repayment terms in everyday language.

Why Specialist Brokers Matter

Complex tax records can look like a puzzle to lenders. That’s where brokers come in:

- They translate tangled financials into clear, lender-friendly narratives.

- They manage document flows, keep in touch with banks and chase approvals.

- They uncover policy quirks and lender preferences you might never see alone.

Start your journey with Diamond Lending’s team and turn those confusing statements into a smooth approval process.

What’s Next

In the next chapter, you’ll learn to:

- Organise tax returns and BAS statements so they pack maximum punch.

- Calculate your exact borrowing capacity with real-world examples.

- Explore refinancing and construction loan pathways tailored to your business.

Proceed to the next chapter now and get your application on the right track.

Choosing The Right Loan Type

Think of picking a home loan as choosing the best tool for a DIY project: the wrong one can set you back weeks or cost you extra thousands. For self-employed borrowers in Australia, it’s not just about the headline rate—it’s about matching the loan to where your business is at and what paperwork you can pull together.

Below, we unpack full-doc, low-doc and no-doc loans in plain English, comparing margins, timeframes and fees so you know exactly what to expect.

- Full-Doc Loans deliver the lowest margins but demand a full suite of documents—tax returns, Notices of Assessment and bank statements. Perfect if you’ve got at least one year of clean financial records.

- Low-Doc Loans ask for Business Activity Statements (BAS) and an accountant’s letter instead of full tax returns, trading off a slightly higher margin for paperwork flexibility. Great for newer ventures showing two quarters of steady cash flow.

- No-Doc Loans rely mainly on bank statements and minimal paperwork. You’ll get a faster answer, but expect steeper rates and generally need a larger deposit.

Real World Comparison

Imagine a café owner with two years of stable profit. They could lock in a 5.10% full-doc rate and pay very little upfront. On the flip side, a freelance consultant who only has recent BAS records might choose a low-doc option to move in faster, even if the margin is a touch higher.

For a deeper dive, see our guide on low-doc loans for freelancers and business owners:

Low-Doc Loans Explained For Freelancers And Business Owners

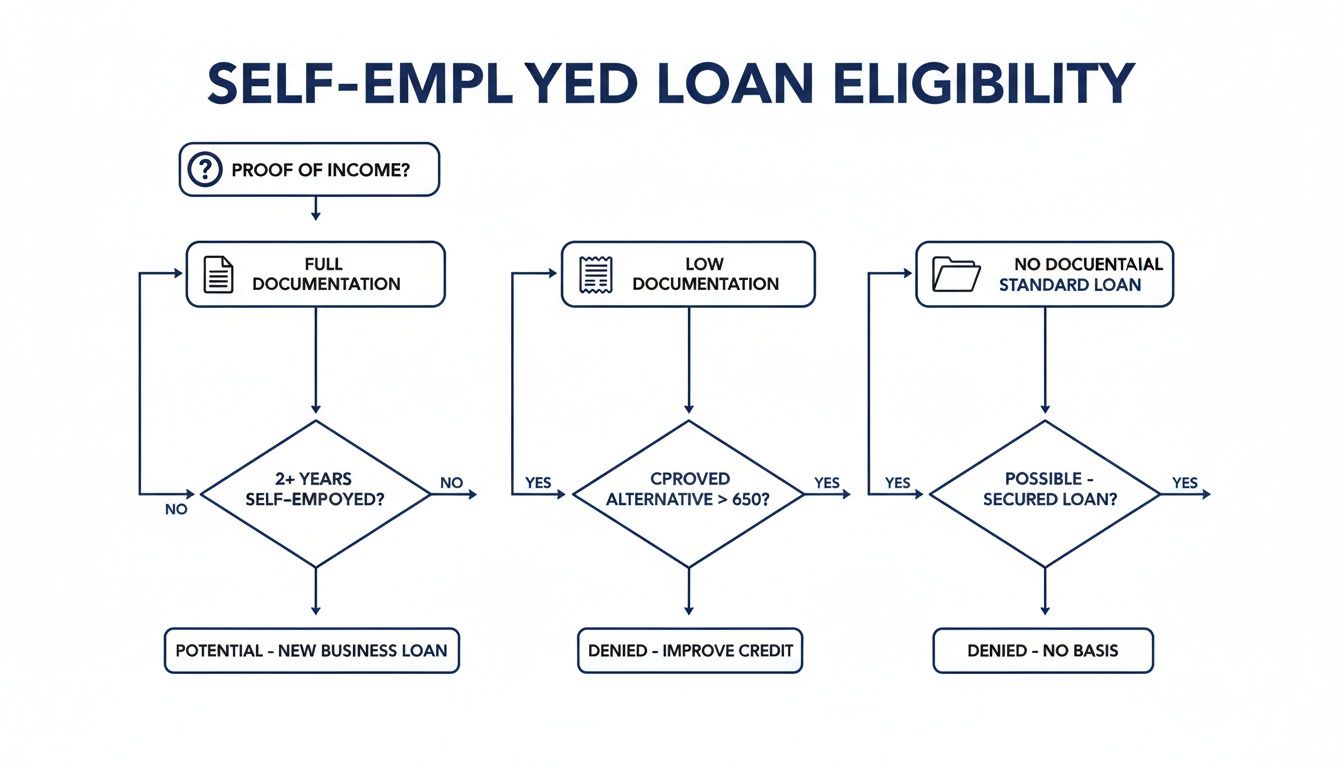

Here is a decision tree infographic that lays out proof requirements and loan pathways for self employed borrowers.

This infographic visualises how proof of income directs you to a full-doc, low-doc or no-doc loan based on your documentation.

Comparing Lender Margins

Margins tend to climb as documentation requirements ease. Here’s a quick comparison:

| Loan Type | Margin (%) | Application Fee |

|---|---|---|

| Full-Doc | 1.50 | $0 – $600 |

| Low-Doc | 1.75 | $600 – $1,200 |

| No-Doc | 2.00 | $1,200 – $1,800 |

- A larger deposit can lower your margin or lift your loan-to-value ratio.

- Consider each lender’s timeline against your project deadlines—delays can cost more than a slightly higher rate.

Approval Timelines And Fees

Here’s what to expect on timing and fees:

- Full-Doc Loans usually take around 4–6 weeks thanks to ATO checks and extensive paperwork.

- Low-Doc Loans often settle in 2–4 weeks, with an application charge of $600 – $1,200.

- No-Doc Loans can close in 1–3 weeks, though establishment fees tend to sit between $1,200 – $1,800.

“Choosing the loan type that fits your documentation speed and cash flow is crucial,” warns a senior broker at Diamond Lending.

Building A Decision Framework

Use this four-step checklist to guide your choice:

- Document Inventory: Do you have one or two years of finalised tax returns, or just BAS?

- Margin Match: Align your business history with the rate you can comfortably service.

- Timeline Needs: Will waiting 4–6 weeks derail your plan, or can you afford a faster but pricier option?

- Deposit Power: Remember, a bigger deposit can compensate for higher margins and fees.

This approach helps you cut through the jargon and pick the right loan product without surprises.

Choosing With Confidence

Securing the loan that fits your documentation and cash flow is a bit like planning a DIY build properly—you save time, reduce stress and avoid unexpected costs. Keep your focus on interest-rate margins, application fees and how quickly each option can settle, and you’ll be in the driver’s seat of your own borrowing journey.

Organising Your Income Documents

Putting together your tax and business records often feels like solving a jigsaw without the picture on the box. Think of each form as a puzzle piece you need to slot into place. In this guide, we’ll map out the paperwork every self-employed borrower in Australia must gather for a home loan application that sails through with minimal hiccups.

First, gather your tax returns and Notices of Assessment for at least one financial year. These documents act like your official scorecard, showing declared profits and your overall tax position.

Next, pull in your BAS statements for the last 12 months. These month-by-month snapshots reveal your GST obligations and PAYG instalments, giving lenders a clear view of how money moves through your business.

Here’s a concise checklist of core documents:

- Tax Returns and Notices of Assessment to confirm annual profit.

- BAS Statements from the past year, detailing GST and PAYG payments.

- Profit & Loss Summaries with one-off expenses added back.

- Bank Statements covering the last 6 months of transactions.

- Trust Deeds or rental schedules if you receive rental income.

Grouping Multiple ABNs

If you juggle several businesses under separate ABNs, merge them into one coherent story. Rather than sending multiple packets of papers, create a summary table that lists each ABN, its annual turnover and main expense category. This approach cuts down lender confusion and speeds up assessments.

| ABN | Annual Turnover | Primary Expense |

|---|---|---|

| 12 345 678 | $120,000 | Supplies |

| 87 654 321 | $90,000 | Contractor Fees |

Crafting an Accountant’s Letter

Think of an accountant’s letter as your financial interpreter. A crisp, one-page note can preempt questions and streamline the process. Ask your accountant to:

- Confirm average net profit after add-backs

- Detail any one-off deductions

- Project expected income for the coming year

Back these figures with our income annualisation calculator. A well-structured letter can reduce lender queries by up to 40%, according to senior brokers at Diamond Lending.

Digitising and Naming Files

Once your paperwork is ready, scan everything into PDF format—this ensures clarity and compatibility. Then, name each file so its contents and date are obvious at a glance.

- Use a format like

P&L_ABN2024.pdffor profit and loss statements - Prefix dates:

2024-07_NOA.pdffor Notices of Assessment - Keep file sizes under 5 MB to ease emailing

- Maintain an index spreadsheet linking filenames to document types

This digital library setup slashes email back-and-forth and lets lenders find exactly what they need instantly.

Presenting Rental and Investment Income

Rental income can boost your borrowing power—by 5%–10% when properly documented. Treat it as a separate income stream:

- Tenancy agreements with tenant names, addresses and lease dates

- Rent ledgers showing monthly deposits and any arrears

- Maintenance logs and expense breakdowns

Highlight net rental profit on your summary sheet to showcase extra cash flow.

Final Document Checklist

Before you hit send, run through this checklist like a pre-flight safety check:

- Tax returns and Notices of Assessment for all entities

- BAS statements and profit & loss summaries

- Bank statements showing cash inflows and outflows

- Accountant’s letter confirming income details and add-backs

- Trust deeds or rental schedules if applicable

- Cover sheet and index spreadsheet for easy reference

Double-check filenames, content and dates. A neat, organised package means fewer queries and faster approval.

Next, we’ll dive into estimating your borrowing capacity using real-world examples and clear tables.

Estimating Your Borrowing Capacity

Planning a home loan can feel a bit like plotting a GPS route—you need a clear sense of the journey ahead. Lenders, in essence, run a serviceability check to make sure your income can comfortably cover repayments.

They examine three core pieces of the puzzle:

- Net Income: What remains after tax and essential expenses.

- Living Cost Benchmark: Typically $2,000–$3,000 per month for a solo borrower.

- Stress-Test Buffer: An extra +2.5% margin to guard against future rate hikes.

At first glance, the maths can seem intimidating. In reality, lenders apply a straightforward formula:

Serviceable Loan = Net Income × Serviceability Factor − Living Costs

As your net income grows, so does your potential borrowing power. A few minutes with a simple spreadsheet is all it takes to map out where you stand.

The screenshot above comes from Diamond Lending’s online serviceability calculator for self-employed applicants. You’ll see fields for net profit, living expenses and buffer rates—change one number, and the estimate updates instantly.

Tip Try splitting your loan into variable and fixed portions. That can lower the overall buffer impact on repayments.

At an annual income of $100,000, many lenders allow around 70% loan-to-income. Bump your earnings to $150,000, and you could support up to $700,000 in borrowing under typical policies.

Estimated Borrowing Capacity Examples

Here’s a snapshot of how borrowing power shifts under standard serviceability rules:

| Annual Income | Monthly Repayments | LVR | Estimated Loan Amount |

|---|---|---|---|

| $80,000 | $800 | 80% | $320,000 |

| $120,000 | $1,200 | 85% | $510,000 |

| $200,000 | $2,000 | 90% | $900,000 |

These figures give you a ballpark to work from when planning your next steps.

By combining business and rental income, you might nudge these numbers higher. Switching to principal-only repayments on one slice of the loan can also reduce the buffer requirement.

Diamond Lending’s calculators pull in living expense data straight from the Australian Bureau of Statistics, so you won’t spend hours hunting down benchmarks.

Optimization Lower assumed living expenses when you share costs in a joint application.

With these insights, you can tailor your home loan strategy to fit your self-employed profile.

Applying Your Estimates

Plug your own figures into an online calculator to reveal your likely borrowing range. Follow these simple steps:

- Step 1 Enter net and add-back income for the past financial year.

- Step 2 Select living expenses based on household size.

- Step 3 Apply a +2.5% stress-test buffer.

- Step 4 Review your estimated loan range and fine-tune assumptions.

These actions turn abstract formulas into clear, actionable forecasts for self-employed borrowers across Australia.

Insight A slightly higher buffer rate can reduce your maximum loan by up to 10%, but it adds a crucial safety margin.

Knowing your limits in black and white helps you avoid unwelcome surprises when the application lands on a lender’s desk. Pre-calculating your capacity also saves time and positions you as a well-prepared borrower.

Armed with these numbers, you’re ready to partner with a broker and lock in the right offer.

Up next, we’ll tackle common documentation roadblocks and show how to overcome them efficiently.

Estimate now using Diamond Lending’s borrowing power calculator on their website. Your numbers give you credibility with lenders from the very first conversation.

Handling Documentation Roadblocks

Self-employed borrowers often bump into paperwork snags that stall their home loan applications. Fluctuating profits, missing documents or unexplained expenses can leave lenders scratching their heads.

Here’s how you can turn each of those hurdles into a clear advantage.

Averaging Income Over Variable Years

Income swings are like waves on the beach—they need a bit of smoothing. If you’ve had a standout year followed by a quieter one, show lenders a two-year average to illustrate stable earnings.

- Gather your net profit from the last two financial years.

- Calculate a monthly average to demonstrate consistency.

- Highlight any one-off deductions or add-backs so nothing is misleading.

Tip: Using an average can boost perceived stability by up to 20% in lenders’ eyes.

Smooth averages give lenders confidence and can fast-track your approval.

Forecasts For New Businesses

Starting out? You won’t have years of tax returns, but forecasts can bridge that gap. Picture a café that’s been trading for six months— a three-year profit forecast, backed by an accountant’s letter, can satisfy most lenders.

- Draft a concise profit forecast for the next 12 months.

- Ask your accountant for a declaration to endorse those numbers.

- Include a breakdown of costs and expected revenue growth.

These three steps can transform a thin file into an application that shines.

Structuring Director Guarantees With Trusts

Trust structures add a layer of complexity, but a director’s guarantee brings accountability into focus. Essentially, you’re promising to cover any shortfall on behalf of the trust.

- Provide a signed director guarantee document.

- Explain trust deed terms in plain English.

- Supply a summary table of beneficiaries and income streams.

“A clear guarantee can reduce lender queries by 30%,” notes a Diamond Lending specialist.

A concise guarantee plus a straightforward summary turns a tangled trust into a lender-friendly package.

Common Missteps And Financial Housekeeping

Even small oversights can derail your application. Keep an eye out for:

- Missing invoices from irregular clients.

- Unrecorded credit-card debts lurking off the balance sheet.

- Unlabelled bank transactions that look suspicious.

Housekeeping tips to prevent delays:

- Reconcile invoices monthly and save them as clearly labelled PDFs.

- List all credit facilities in a single liabilities summary.

- Create an indexed cover sheet to guide lenders through your documents.

A simple index and consistent file naming can shave days off your approval timeline.

Turning Documentation Challenges Into Approval Strengths

Think of documentation hoops like fallen trees on a hiking trail—with the right tools, you clear them out. A pre-submission check is your machete.

- Run a full document audit checklist two weeks before lodgement.

- Simulate lender queries by reviewing each file for clarity.

- Schedule a broker review to catch gaps and polish your story.

Expert Insight: A proactive checklist can reduce approval delays by up to 50%.

With these steps, you turn potential snags into undeniable wins—and get your home loan across the line faster.

Exploring Refinancing And Construction Loans

As soon as your initial home loan is in place, two paths emerge: refinancing for equity release, or tapping into construction finance to build from scratch.

Refinancing isn’t just about chasing a lower rate. It’s how you can consolidate higher-interest debts, unlock cash for a renovation, or reset your borrowing costs once your property has grown in value.

Construction loans, on the other hand, rely on staged progress payments tied to builder milestones and periodic valuations.

Lenders calculate equity release by projecting your home’s post-renovation value and often apply interest capitalisation to cover costs until completion.

- Refinance Path: Trim your rate, roll high-rate credit card debt into your mortgage, tap into renovation funds

- Construction Loan: Drawdowns at key stages, builder inspections, structured payouts

- Equity Release: Up to 80% LVR based on the after-works valuation

- Progress Stages: Typically five drawdowns aligned with builder milestones

How Refinancing Works

Market rates dip, you’ve banked equity—or both. That’s your cue to refinance. Imagine moving from 5.50% to 4.20%; over a 25-year term, you could save tens of thousands.

It’s also a chance to roll high-rate credit card debt into your mortgage, simplifying repayments and reducing total interest.

“A well-timed refinance turned my renovation dream into reality,” shares a Diamond Lending client.

Process Steps For Construction Financing

- Submit your detailed building plans and signed contracts to the lender.

- Arrange a pre-construction valuation and agree on a drawdown timetable.

- Release funds in stages as each milestone is completed.

- Organise independent inspections to trigger the next payment.

This step-by-step approach keeps nasty cashflow surprises at bay.

Consider an interest-only option during construction to ease early expenses—though expect a slightly higher rate. Working with a quantity surveyor and syncing to your builder’s schedule ensures each drawdown meets security checks.

Negotiate terms carefully and align valuations to your build phases. That way, you’ll maintain momentum and stay in control of costs.

Choosing between a straight refinance or a full construction loan often comes down to your cashflow and timeline. For instance, you might refinance to free up $100,000 before engaging builders.

- Tip 1: Lock in an interest-only period for renovations

- Tip 2: Schedule valuations just before drawdowns

- Tip 3: Review your loan contract for any exit fees

A crystal-clear inspection report can speed up drawdowns and cut delays.

“Treat drawdowns like timed water taps; delivering funds at the right moment keeps your build nourished,” advises a Diamond Lending expert.

Armed with these insights, you can plan your refinance or construction loan with confidence.

- Book a free 15-minute call with Diamond Lending

Start your journey with a free chat today.

Real Life Case Studies And Common Questions

Real-world stories often bring the loan process to life for self-employed borrowers in Australia.

For instance, a freelance graphic designer in their first year of business had only limited tax history. They pulled together four BAS statements, a profit & loss summary and an accountant’s letter. To smooth out uneven payments, they also provided six months of bank statements showing consistent client deposits.

The result? That low-doc application went from lodgement to conditional approval in just three weeks.

“Having clear BAS records and a precise accountant’s letter cut lender queries in half.”

Key Steps for a Smooth Low-Doc Application:

- Gather one year of BAS and a concise profit & loss summary.

- Request an accountant’s letter that explains income fluctuations.

- Provide six months of bank statements with deposits labelled clearly.

Case Study Summaries

| Borrower | Loan Type | Key Documents | Approval Timeline |

|---|---|---|---|

| Graphic Designer (1 year) | Low Doc | BAS, Accountant Letter, Bank Statements | 3 Weeks |

| Tradie (3 years) | Full Doc | Tax Returns, BAS, Trust Deeds, P&L | 5 Weeks |

This snapshot shows how different document kits line up with varying loan pathways.

Tradie Uses Trust Accounting

Another borrower—a tradie with three years of trading under their belt—opted for a full-doc home loan. They combined rental income held in a trust with business profits. Their application package included:

- Two years of finalised tax returns

- Trust deeds and beneficiary schedules

- Profit & loss reports and Notices of Assessment

Working alongside a broker, they added back depreciation and one-off expenses. That move lifted their LVR by 10% and wrapped up approval in just five weeks.

- Compile two years of finalised tax returns.

- Include trust deeds and beneficiary schedules.

- Craft an accountant’s letter to clarify all add-backs.

Expert Insight: Clear trust summaries can reduce approval delays by 30%.

Common Questions Answered

These FAQs clear up the most frequent queries from self-employed applicants:

How long to be self-employed before applying?

Most lenders look for one to two years of trading history. However, a one-year low-doc path is possible with strong BAS records and a detailed accountant’s letter.

What documents prove income best?

The strongest evidence includes individual tax returns, BAS, profit & loss summaries and a concise accountant’s letter.

Can I include a spouse’s income?

Absolutely. A joint application can boost your borrowing power—as long as both parties supply full income records.

What if my tax returns show a loss?

Lenders will ask for forecasts and an accountant’s explanation. You can also offset dips with robust bank statements or a larger deposit.

These examples and answers give you a clear roadmap for preparing a home loan application as a self-employed borrower in Australia.

Use these insights to work closely with a broker, refine your documents and secure the right loan.