When you run your own business, securing a home loan can feel like navigating a maze without a map. But here’s the thing: it’s absolutely doable. The biggest challenge is proving your income when you don't have a neat and tidy payslip, but smart lenders see your entrepreneurial drive as an asset, not a roadblock. Think of this guide as your map to turning that business success into your dream home.

Your Path to a Home Loan as a Business Owner

Applying for a home loan as a business owner is definitely a different ball game compared to the standard process for PAYG employees. Lenders look at your financial story through a unique lens, focusing on consistency and profitability over time, not just a simple fortnightly salary. This means a bit more paperwork, sure, but it doesn't make the path harder—it just means preparation is everything.

The old idea that self-employed borrowers are a higher risk is being turned on its head. In fact, many business owners have stronger financial profiles. Recent industry analysis shows that while 77% of all home loan borrowers have 'excellent' credit scores, that number actually climbs to 80% for investors—a group packed with entrepreneurs using property to build wealth. You can read more about home loan market trends on mpamag.com.

Understanding the Lender's Viewpoint

To get approved, you need to think like a lender. They're looking for one thing above all else: a stable and reliable income stream that can comfortably handle a mortgage for the long haul. For an entrepreneur, this means presenting your business's financial health in a clear, compelling story.

Your job is to replace the certainty of a payslip with the undeniable evidence of a profitable, well-managed business. This is all about showcasing consistent revenue, controlled expenses, and a clean financial history.

What This Guide Covers

We’ve put this guide together to break down everything you need to know. We’ll walk you through the key differences in how lenders will assess your application and what you can do to put your best foot forward. You'll learn about:

- The different types of home loans out there, from full-doc to low-doc options.

- The essential documents you’ll need to build a rock-solid application.

- Powerful strategies to maximise your borrowing capacity and get more from your loan.

- A step-by-step roadmap to navigate the application process smoothly from start to finish.

Ever felt that your business is kicking goals, but the banks just don't seem to get it when you apply for a home loan? You're not alone. It all boils down to how lenders see risk, and for them, predictability is king.

Think of it this way: a standard PAYG employee's income is like a dripping tap – consistent, reliable, and easy to measure. It lands in their bank account every fortnight, regular as clockwork. For a lender trying to forecast your ability to pay a mortgage for the next 30 years, that’s a dream scenario.

A business owner's income, on the other hand, is more like a powerful river. It ebbs and flows with seasons, project cycles, and how much you reinvest for growth. While it might be much larger overall, its variability makes lenders nervous. They need to be sure that a dry spell won't leave you unable to make your repayments.

The Core Concept of Serviceability

At the heart of any loan application is a simple idea called serviceability. It’s the lender’s math for working out if you can comfortably afford—or 'service'—the loan repayments without putting yourself under financial stress.

They aren't just looking at your headline revenue. They dive deep into your net profit, after you’ve paid all your business expenses and the tax man has taken his cut. What’s left is what they consider your real capacity to repay a loan.

This is where it gets tricky for entrepreneurs. One stellar year of profit, while great for you, might not be enough to convince a bank. They're far more interested in seeing a consistent and stable track record over time.

Lenders are really just trying to answer one question: "Can we count on this person's income to cover the mortgage every month for the next three decades?" Your job is to build an application that screams a confident "yes".

To get that confidence, they’ll typically average out your income from your last two tax returns. This process smooths out the impressive peaks and the worrying troughs, giving them what they see as a more realistic, conservative view of your long-term earnings. It’s a frustrating process, especially if your business is young and growing fast, but it’s a non-negotiable part of their assessment.

Understanding Lender Concerns

If you want to build a rock-solid application for home loans for business owners, you need to get inside a lender’s head and understand what keeps them up at night. Their caution isn't personal; it’s just business.

Here are the specific things a credit assessor will be scrutinising:

- Fluctuating Revenue: Unlike a salary, your income can have big swings from one month to the next. They need to be sure a slow quarter won't derail your ability to pay the mortgage.

- Business Expenses and Debts: They’ll look closely at any existing business liabilities, like equipment finance or overdrafts. These commitments affect your overall financial picture and reduce the funds available for a home loan.

- Industry and Market Stability: The sector you operate in matters. A business in a historically stable industry might be viewed more favourably than one in a new, unproven, or volatile market.

- Cash Flow Management: This is huge. Demonstrating that you manage your business’s cash flow effectively is critical. A history of healthy, consistent bank balances is one of the most powerful pieces of evidence you can provide.

Once you know what they’re worried about, you can tackle their concerns head-on. Instead of just throwing a pile of numbers at them, you can craft a story that shows your business is stable, well-managed, and has a reliable financial future. This turns their risk assessment from a hurdle into your opportunity to shine.

Decoding Your Loan Options: Full Doc vs Low Doc

When you're running your own business, the path to a home loan isn't a straight line. It's more like a highway with different on-ramps, each designed for a specific financial journey. Getting your head around the options is the first step to making sure your application is built for success from the get-go.

The two main routes you'll come across are Full-Documentation (Full Doc) and Low-Documentation (Low Doc) loans. These aren't just different labels for the same thing—they represent two fundamentally different ways of proving your income to a lender.

The Gold Standard: The Full Doc Loan

A Full-Documentation loan is the classic, most traditional type of home loan. It’s the lender's preferred method and usually comes with the most competitive interest rates on the market. It gets its name because it requires you to lay all your financial cards on the table, typically covering the last two full financial years.

To go down this path, you'll need to provide a comprehensive set of documents, including:

- Complete personal and business tax returns for the past two years.

- The matching Notices of Assessment from the ATO.

- Detailed business financials, like Profit & Loss statements and Balance Sheets.

For business owners with a well-established company and squeaky-clean, up-to-date records, a full-doc loan is the perfect fit. It gives the lender a crystal-clear, verifiable picture of your long-term profitability and stability. This level of proof lowers their perceived risk, and they reward these applications with their sharpest rates and best loan features.

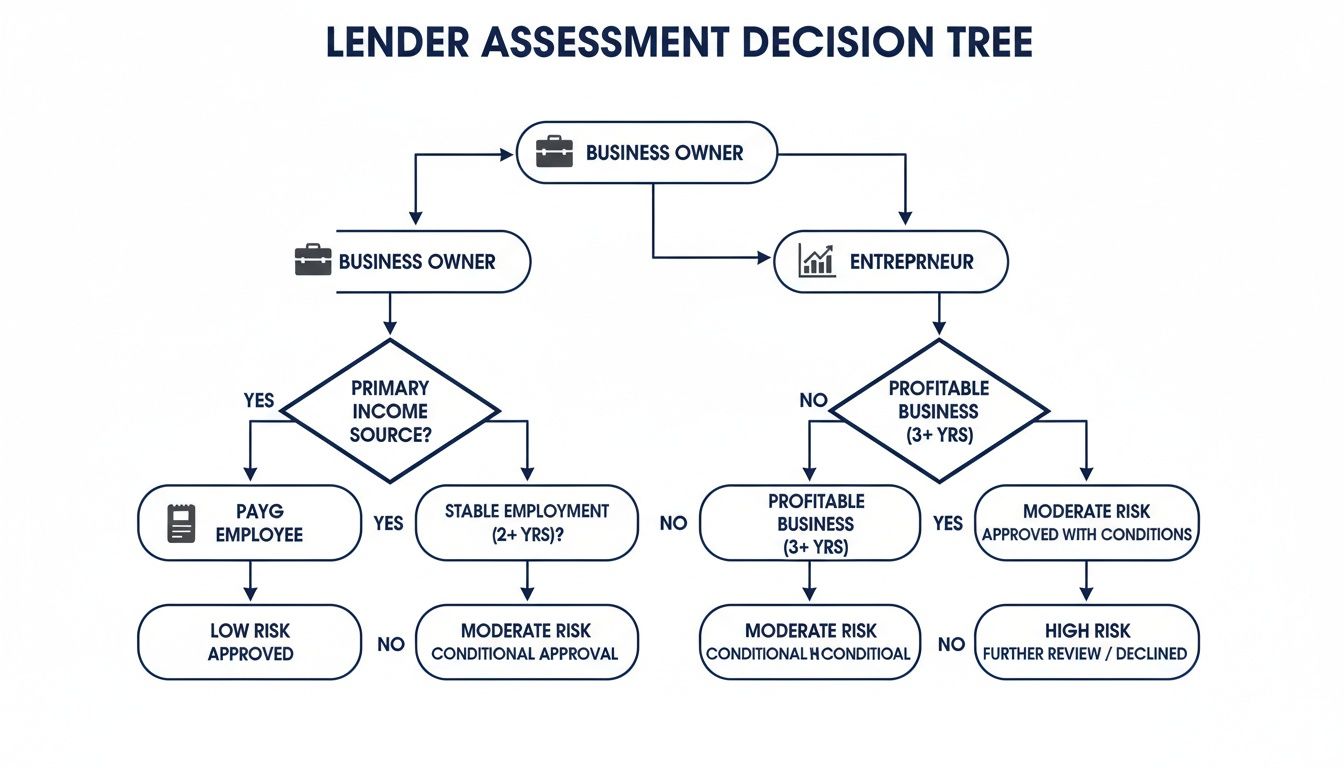

This decision tree below shows how lenders start their assessment, separating standard PAYG applicants from entrepreneurs who need a different kind of evaluation.

As the visual shows, while everyone starts with the same goal—a loan—the journey for a business owner immediately branches off, demanding a more specialised look at their unique financial setup.

The Flexible Alternative: The Low Doc Loan

But what if your business is still in its early days? Or maybe your income is complex and doesn't fit neatly into a two-year tax return box? This is exactly where a Low-Documentation loan shines. It's a common myth that 'low doc' means 'no doc'—nothing could be further from the truth.

A low-doc loan isn’t about having no documents; it’s about using alternative documents to prove your income when standard tax returns aren't suitable or don't tell the full story.

This option is tailor-made for entrepreneurs whose businesses are in a high-growth phase or whose income streams are less conventional. Instead of focusing solely on past tax returns, low-doc loans let you verify your earnings using other strong financial indicators that reflect your current reality.

To help clarify the differences, here's a quick comparison of the two main loan types for business owners.

Full Doc vs Low Doc Home Loans: A Comparison for Business Owners

| Feature | Full-Doc Loan | Low-Doc Loan |

|---|---|---|

| Primary Documents | Two years of tax returns and financials. | BAS, business bank statements, or accountant's letter. |

| Ideal For | Established businesses with a long, stable history. | Newer or growing businesses with complex income. |

| Interest Rates | Typically lower, most competitive rates available. | Usually slightly higher to offset perceived risk. |

| Application Process | Standard, data-driven assessment. | More flexible assessment, focusing on current cash flow. |

With a low-doc loan, you'll generally need to provide documents like your Business Activity Statements (BAS) for the last 12 months, recent business bank statements showing consistent cash flow, or a verification letter from your accountant. For a deeper dive, you can read our comprehensive guide on low-doc loans for freelancers and business owners. This flexibility is a game-changer for the modern entrepreneur.

What About No-Doc Loans?

You might also hear whispers about No-Documentation (No-Doc) loans. It's important to know these are highly specialised and very rare products in today's market. They are almost never used for buying a family home and are typically reserved for sophisticated property investors who can secure the loan entirely against existing property equity, without needing to prove their income at all.

For most business owners looking for a home, the real choice is between a full-doc and a low-doc loan.

Interestingly, despite the extra hoops to jump through, business owners often aim higher. Data from the Australian Bureau of Statistics shows self-employed borrowers request an average home loan of $616,000. That's significantly more than the $540,000 average for full-time employees, showcasing the ambition and confidence that entrepreneurs bring to the property market.

Preparing Your Essential Application Documents

When you're a business owner applying for a home loan, you're not just filling out forms. You're essentially building a business case for yourself. The goal is to curate a financial story that proves your business isn't just a passion project—it's a reliable, income-generating asset. Getting your documents sorted is the single most important step in this entire process.

Lenders need to see a complete and consistent picture of your financial health, and each document you provide adds a crucial piece to that puzzle. Think of your tax returns as the backbone of your story, proving a stable income trend over time.

This preparation is all about presenting your business in its best light, showing its true strength and long-term viability. It’s about moving beyond a simple profit number to demonstrate sound financial management.

The Core Financial Documents

For any business owner chasing a home loan, some documents are simply non-negotiable. They form the foundation of your application, giving lenders the hard data they need to assess what you can realistically borrow. While the specifics can vary a little between lenders, this checklist covers the absolute essentials.

Here’s what you’ll need to pull together:

- Two Most Recent Tax Returns: You’ll need both your personal and your business tax returns. Lenders use these to track your income over a 24-month period, averaging the figures to establish a conservative but reliable earnings baseline.

- ATO Notices of Assessment: These are the official documents from the Australian Taxation Office confirming they've processed your returns. They act as independent validation for the income figures you've declared.

- Business Financial Statements: This means your Profit & Loss (P&L) statements and Balance Sheets for the last two years. The P&L shows your profitability, while the Balance Sheet gives a clear snapshot of your company’s assets and liabilities.

These core items paint a clear, historical picture of your business's performance. For a full-doc loan, they are the primary evidence used to calculate your serviceable income.

Proving Your Business Identity and Operations

Beyond your financial history, lenders also need to know that your business is a legitimate, actively trading entity. These next documents establish your business's identity and operational status, giving the lender complete confidence in its authenticity.

You will need to provide:

- ABN and/or ACN Registration: Proof of your Australian Business Number (ABN) or Australian Company Number (ACN) is the first step to verifying that your business is officially registered and above board.

- Business Activity Statements (BAS): Your last four quarters of BAS are especially vital for low-doc loan applications. They offer a much more current view of your business's turnover, acting as recent, real-time proof of income.

- Business Bank Statements: Lenders will often ask for the last six months of your business bank statements to see your cash flow in action. Consistent deposits and a healthy operating balance are powerful signs of a well-run business.

Together, this paperwork creates a comprehensive file that leaves no room for a lender to doubt your business's legitimacy or its financial standing.

Strengthening Your Case with Supplementary Evidence

A standard application tells a lender what your business has done in the past. But to build an undeniable case, you can provide extra evidence that paints a picture of a strong and stable future. This is your chance to go the extra mile and really stand out.

Think of supplementary documents as the supporting characters in your financial story. They add depth, context, and forward-looking confidence that your core financials might not fully capture on their own.

Consider adding these powerful extras to your application file:

- An Accountant's Letter: A signed letter from your accountant can verify your income and confirm the financial health of your business. This adds a powerful layer of professional validation to your claims.

- Proof of Consistent Savings: Showing a strong savings history demonstrates financial discipline. It's a massive green flag for lenders, proving you can manage money effectively.

- Long-Term Client Contracts: If your business relies on a few key clients, providing copies of long-term contracts can prove the stability of your future income stream.

- A Detailed Business Plan or Forecast: This is particularly useful for newer businesses. A well-researched forecast can help a lender understand your growth trajectory and future earning potential.

By proactively providing this extra information, you answer potential questions before they're even asked. This thoughtful approach shows lenders you're organised, transparent, and a low-risk applicant, massively improving your chances of securing one of the best home loans for business owners on the market.

Strategies to Maximise Your Borrowing Power

Getting a home loan when you're self-employed isn’t just about ticking boxes to meet the minimum criteria. It's about building the strongest possible case for yourself—showing the lender a clear and confident picture of your financial health. This is where you can really take control of the outcome.

Many entrepreneurs don't realise their taxable income—the figure they’ve worked so hard to minimise—doesn't tell the whole story. With the right strategies, you can unlock the hidden borrowing potential that lenders might otherwise miss.

Unlocking Your True Income With Add-Backs

One of the most powerful tools in your kit is the concept of add-backs. Think of these as legitimate business expenses that a lender can add back to your net profit when assessing your income. It's like showing them the money that’s still working for your business, even after you've claimed it as a deduction.

These are some of the most common add-backs:

- Depreciation: The decline in value of your business assets (like a company car or equipment) is a paper expense, not actual cash leaving your account. Lenders can add this figure back to your income.

- One-Off Expenses: Did you have a major, non-recurring purchase last year, like a huge equipment upgrade? That can often be excluded from the regular expense calculation.

- Additional Superannuation Contributions: Any voluntary contributions you've tipped into your super above the compulsory amount can often be added back to your serviceable income.

- Interest on Business Loans: In some cases, the interest you've paid on existing business debts can be included back into your income assessment.

By working with a broker who knows the ins and outs of these add-backs, you can present a much healthier income figure, which directly translates to a bigger borrowing capacity.

Clean Up Your Debts and Credit File

Your existing financial commitments play a massive role in how much a lender will offer you. Every dollar you owe somewhere else is a dollar they assume you can't put towards a mortgage.

Before you even think about applying, focus on these key areas:

- Reduce High-Interest Business Debts: Start paying down credit cards, overdrafts, and other costly business loans. This lowers your total liabilities and instantly improves your debt-to-income ratio.

- Lower Credit Card Limits: This is a big one. Lenders often assess 3% of your total credit card limit—not your balance—as a monthly expense. Dropping the limits on cards you don't really use can give your borrowing power an immediate boost.

- Review Your Credit Report: Pull your credit file and check for any errors, defaults, or late payments. Cleaning this up before a lender sees it prevents unnecessary red flags and shows you’re a reliable borrower.

A clean financial slate is your strongest negotiating tool. It demonstrates discipline and reduces the lender’s perceived risk, making them more confident in approving a larger loan amount.

The property market is already reflecting the financial muscle of entrepreneurs. Investor lending, often driven by business owners, recently outpaced owner-occupier growth. In just one quarter, new investor loan commitments shot up by 13.6% in number and 17.6% in value, proving just how significant business owners are in the market. You can read more about the growth of investor lending in The Adviser.

Separate Your Finances and Time Your Application

Clarity is king. Lenders get nervous when personal and business finances are a tangled mess. Keeping separate bank accounts for business revenue and personal spending makes their job easier—and your application stronger. It gives them a crystal-clear view of your true income and expenses.

Timing is also everything. The absolute best time to apply for a home loan is right after you've lodged a strong tax return showing solid profitability. This gives the lender the most current, compelling evidence of your business's health and success.

By planning ahead, you can align your application with your peak financial performance, dramatically increasing your chances of getting that 'yes'. To see how these strategies could impact your numbers, it's worth playing around with the right tools. You can learn more about how to use borrowing power calculators in Australia in our detailed guide.

Your Step-By-Step Application Roadmap

Navigating the home loan journey as a business owner can feel like a maze, but it’s far more manageable when you have a clear roadmap. Think of it less as a sprint and more as a well-planned expedition. Following a structured process ensures all your hard work preparing your financials pays off, building a compelling story for lenders.

This is where all your preparation comes together. With the right guidance, the entire process—from that first thought of buying to getting the keys on settlement day—can be surprisingly straightforward. A specialist broker acts as your project manager, keeping the lenders, accountants, and conveyancers all on the same page and moving in the right direction.

Phase 1: Initial Strategy and Assessment

Before you even start scrolling through property listings, the first step is to sit down and map out a strategy. This initial chat with a specialist mortgage broker is all about getting a crystal-clear picture of your financial position, your business structure, and exactly what you want to achieve. It’s a deep dive into your world to figure out the smartest way forward.

This phase is all about:

- Defining Your Goals: Are you buying your first home, upgrading the family nest, or snapping up an investment property? Getting specific here is key.

- Calculating Your True Borrowing Power: We’ll analyse your business financials, hunt for legitimate income add-backs, and give you a realistic estimate of what you can actually borrow. No guesswork.

- Choosing the Right Loan Path: Based on your paperwork and business history, we’ll determine if a full-doc or low-doc loan is the right fit for you.

Phase 2: Document Collection and Application Structuring

Once the strategy is locked in, it’s time to gather the evidence to back it up. This is where we collect all the documents we've talked about and arrange them to tell your financial story in the best possible light. It’s not about dumping a pile of paperwork on a lender’s desk; it’s about curating a narrative that screams financial stability.

The quality of your application is directly tied to the quality of your preparation. A well-organised, comprehensive file answers a lender's questions before they even ask them, making their job—and your approval—a whole lot easier.

Your broker will be your guide, making sure every detail, from your tax returns to your BAS statements, aligns perfectly with what the lender needs to see. This careful prep work dramatically cuts down delays and gives your approval odds a serious boost.

Phase 3: Lender Selection and Submission

With a polished application ready to go, the next move is finding the right lender. This is a huge advantage of working with a broker—we have access to a wide range of lenders, including specialists who genuinely understand the ins and outs of self-employed income.

The final steps on your journey look like this:

- Lender Matching: Your broker plays matchmaker, pairing your unique financial profile with the lenders most likely to say "yes" on great terms.

- Application Submission: Your completed application is formally submitted to the lender's credit team for assessment.

- Negotiation and Approval: We’ll handle any questions from the lender, clarify any points, and work to secure that formal loan approval for you.

- Settlement: This is the home stretch. The legal work is finalised, funds are transferred, and you officially get the keys to your new property. ✅

Of course. Here is the rewritten section, crafted to sound like an experienced human expert and match the tone of the provided examples.

Common Questions from Business Owners

Even with a clear plan, getting a home loan when you're self-employed throws up a lot of questions. Your situation is unique, and you need straight answers to move forward with any real confidence. We hear these queries all the time from entrepreneurs just like you.

How Long Do I Need to Be in Business to Get a Home Loan?

This is usually the first question on every new business owner's mind. For a standard, full-doc home loan, most banks want to see a minimum of two years of trading. This gives them two full tax returns to look over, which helps them get comfortable with your income and its consistency.

But don't panic if your business is still fresh. Some specialist lenders are a lot more flexible and might look at your application with as little as 12 months on your ABN. This usually means you’ll be looking at a low-doc home loan, where they verify your earnings using different paperwork.

The real key is to show you have a solid business with consistent cash flow. Lenders will want to see things like:

- Business Activity Statements (BAS): Your last four quarters give a great, up-to-date picture of your turnover.

- Business Bank Statements: A good six to twelve months of statements can prove a healthy and regular flow of income.

- An Accountant's Letter: A simple letter from your accountant confirming your earnings and future profitability can go a long way.

Can I Use My Business Income to Buy an Investment Property?

You absolutely can. Using your business success to start building a property portfolio is a classic wealth-creation strategy that thousands of Aussie entrepreneurs rely on. The process for getting an investment loan isn't all that different from buying a place to live in.

The big advantage here is that lenders will also factor in the potential rental income from the property you're buying. They'll add this expected rent to your business earnings when they do their sums, which can give your borrowing power a serious boost.

Lenders often look very favourably on business owners who are also property investors. It signals you're financially savvy and focused on building assets—two massive green flags for any borrower.

How Do My Business Debts Affect My Home Loan Application?

Your business debts are a massive piece of the puzzle. Lenders need a completely transparent look at all your financial commitments—both personal and business—to get an accurate picture of your ability to handle a new mortgage.

Things like equipment finance, outstanding business loans, and company credit card balances are all crunched into your debt-to-income (DTI) ratio. This number tells the lender how much of your income is already spoken for, helping them figure out if you can genuinely afford to service a new home loan.

The best move you can make is to pay down or consolidate any high-interest business debts before you even think about applying. Cleaning up these liabilities improves your DTI ratio, strengthens your financial profile, and shows the lender you’re a responsible manager of your finances.

Navigating the world of home loans for business owners is a different ball game. At Diamond Lending, our specialist brokers live and breathe the financial world of entrepreneurs. We know how to build an application that gets a "yes." Start your journey with a personalised assessment today.