Securing a commercial property loan in Melbourne is a completely different ball game compared to a standard home loan. We're talking about specialised finance to buy, develop, or refinance buildings used for business—assets like offices, warehouses, and retail shops. Lenders aren't just looking at your payslip; they're laser-focused on the property's income potential and the strength of your business case.

Your Guide To Melbourne's Commercial Property Finance

Welcome. This is your essential guide to navigating Melbourne’s dynamic and often complex commercial property finance market. We’ve designed this for ambitious business owners, savvy investors, and seasoned developers who want to capitalise on the real opportunities out there. The Melbourne market is robust, especially in resilient sectors like industrial real estate, but cracking the lending world is crucial to your success.

We’re here to cut through the jargon and show you what’s really happening behind the scenes. From understanding which lenders have an appetite for certain deals to knowing which financial product actually fits your goals, clarity is everything. This guide will walk you through the different financing paths available, whether you're buying your first warehouse or refinancing a large-scale portfolio.

Why Specialist Guidance Is Crucial

The road to securing commercial finance can be a minefield. Lenders assess these applications with a completely different lens than residential mortgages, placing a heavy emphasis on factors unique to commercial assets.

They zoom in on a few key areas:

- Property Type and Location: An industrial warehouse in Truganina is a world away from a retail space in the CBD. Lenders have very specific preferences and risk models for different postcodes and property classes.

- Lease Strength and Tenant Quality: The income stream is king. Lenders will scrutinise every detail of your leases, the financial stability of your tenants, and the vacancy rates in the surrounding area. A long-term lease to a national brand? That’s gold.

- Your Financial Position and Experience: Lenders need to see more than just your ability to service the debt. They want a strong business case, healthy financials, and proof that you have relevant experience in managing commercial properties.

Navigating the world of commercial property loans in Melbourne isn't just about chasing the lowest rate. It's about structuring the deal correctly to align with your business goals, satisfy the lender's (often unwritten) rules, and set your investment up for long-term success.

Charting Your Course

This is where working with a specialist broker gives you a critical edge. An expert who lives and breathes this stuff understands the nuances of each lender’s policies. They know how to translate your financial situation into a compelling application that gets a "yes." A good broker turns a complicated, often stressful process into a clear, actionable strategy.

Our goal is to give you the confidence and knowledge to make sharp, informed decisions in Melbourne’s competitive market. By the end of this guide, you'll have a clear roadmap—from choosing the right loan type to understanding every associated cost and avoiding the common pitfalls we see every day.

Let’s get started.

Choosing The Right Commercial Loan For Your Goals

Picking the right loan for your Melbourne commercial property is about much more than just chasing a low interest rate. The loan's structure needs to be a perfect match for your strategy. A warehouse for your own business has completely different needs than a multi-tenanted office building for an investment portfolio. Get it wrong, and you could face serious cash flow headaches and even miss out on future opportunities.

Unlike the one-size-fits-all world of residential mortgages, commercial property loans in Melbourne are built around the specific asset and your financial story. Getting your head around the key differences is the first step to making a smart, powerful decision.

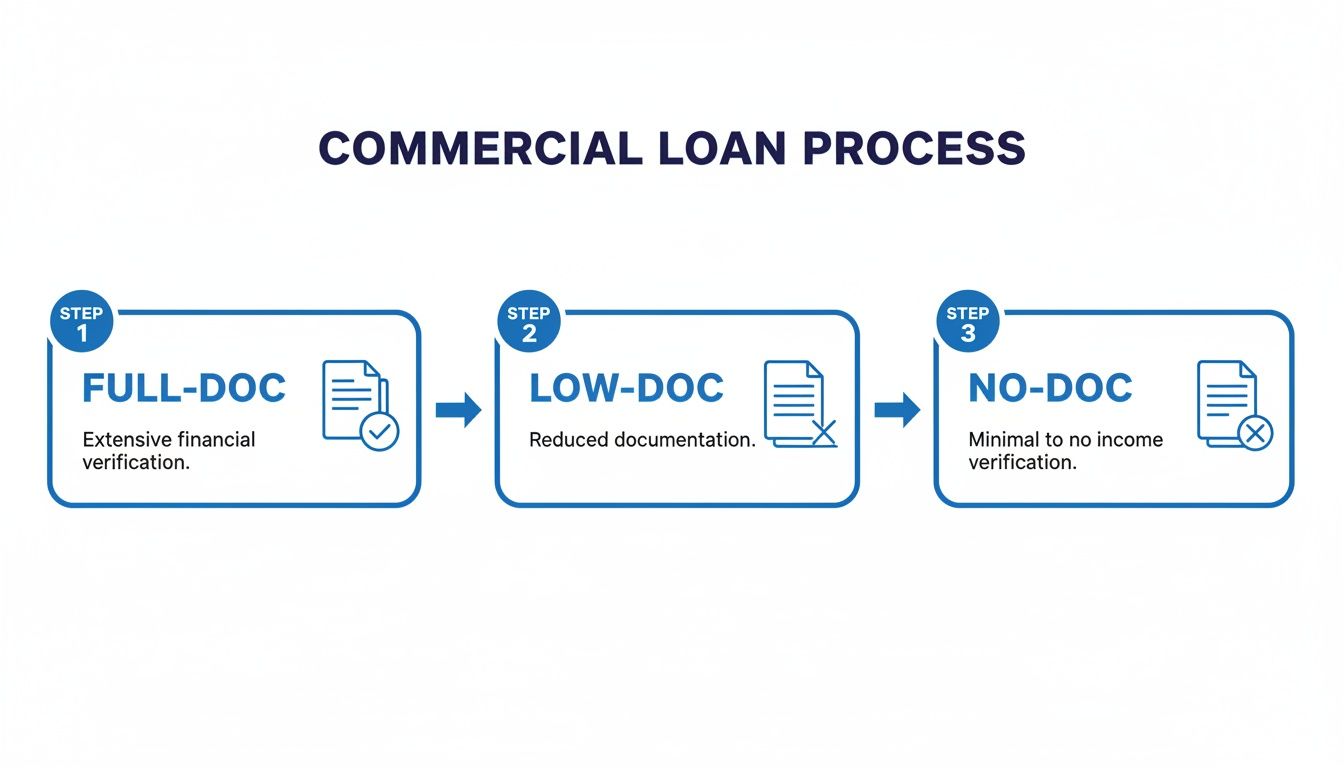

Full Documentation Loans: The Traditional Path

A full-doc loan is what most people think of when they hear "commercial finance." It's designed for established businesses and borrowers who can provide a complete financial picture to prove their income and ability to service the debt. Think two years of business and personal tax returns, detailed financial statements, and BAS statements.

Lenders love full-doc applications because they offer a crystal-clear view of a borrower's financial health, which naturally lowers their risk. The reward for this transparency? You’ll generally get access to more competitive interest rates and higher Loan to Value Ratios (LVRs), sometimes up to 80% for a standard commercial property. It’s the ideal route for businesses with a solid, consistent trading history.

Low Documentation Loans: For The Self-Employed

But what if your tax returns don't tell the full story? This is a reality for countless self-employed people, contractors, and businesses with complex or rapidly growing income streams. That’s where a low-doc loan provides a vital alternative, letting you secure finance without the traditional mountain of paperwork.

Instead of full tax returns, a low-doc application usually relies on things like:

- An accountant's declaration of your income

- Business Activity Statements (BAS) from the last 12 months

- Recent business bank account statements

A low-doc loan isn't a "shortcut" for people who can't afford finance. It's a specialist solution for borrowers who are in a strong financial position but whose income is just difficult to prove with standard PAYG-style paperwork.

Lenders get it—a new business or a recent growth spurt won't always show up accurately in historical tax documents. While you might see slightly higher interest rates or lower LVRs (typically around 65-70%) to balance the lender's risk, these loans give many of Melbourne’s most dynamic entrepreneurs the access to capital they need. For a deeper look into how these mortgages work for businesses, you can explore our guide on business mortgage loans to see how they can support your growth.

Bridging Finance: Seizing Opportunities Quickly

Picture this: you've found the perfect commercial property at auction, but your current place hasn't sold yet. In Melbourne's fast-moving market, hesitation means missing out. This is exactly where a bridging loan steps in. It provides the short-term capital you need to "bridge" the gap between buying a new property and selling an existing one.

These are short-term, interest-only loans, usually for up to 12 months. They give you the power to act decisively and lock down a valuable asset without being held hostage by the timing of another sale. The rates are higher than long-term finance, but their strategic value in a competitive bidding war is massive.

Comparing Commercial Loan Types For Melbourne Borrowers

The right loan structure is completely dependent on your unique situation, your goals, and your financial paperwork. A quick comparison helps show which path might be the best fit for your Melbourne property ambitions.

| Loan Type | Best For | Typical LVR Range | Key Feature |

|---|---|---|---|

| Full-Doc Loan | Established businesses with complete financial records and a strong trading history. | 70% – 80% | Offers the most competitive interest rates and highest borrowing capacity due to lower perceived risk. |

| Low-Doc Loan | Self-employed borrowers, new businesses, or those with fluctuating or hard-to-verify income streams. | 65% – 70% | Provides crucial flexibility by accepting alternative income verification documents like BAS or an accountant's letter. |

| No-Doc Loan | Sophisticated investors with significant assets where the loan is assessed purely on the property's rental income. | Up to 65% | Requires no income verification from the borrower; approval is based solely on the asset's ability to service the debt. |

| Bridging Loan | Investors and business owners who need to purchase a new property before selling their existing one. | Varies (Asset-dependent) | A short-term solution (6-12 months) that provides the speed and certainty needed to secure time-sensitive deals. |

Ultimately, the best commercial property loans Melbourne lenders have on offer are the ones matched correctly to your goals, your numbers, and the asset itself. Once you understand these core differences, you can start identifying the financial product that will not just secure the property, but empower your long-term success.

Mastering the Loan Application and Documentation

When it comes to securing commercial property finance in Melbourne, your success hinges on meticulous preparation. Honestly, getting all your documents in order before you even think about lodging an application can shave weeks off the process and save you a world of stress.

Whether you're a sole trader or a company director, lenders will scrutinise your numbers from every angle. Understanding what they need upfront—from your ABN/ACN details to rental income forecasts—is the first real step in a smooth approval journey.

The process generally follows one of three documentation pathways, depending on your situation and the lender you're working with.

As you can see, a Full-Doc loan requires the most exhaustive evidence. At the other end, a No-Doc loan relies more on asset values and existing rent rolls to speed things up, which is a great option for certain types of investors.

Getting Your Documentation Checklist Ready

The best way to start is by organising your paperwork into three piles: who you are, what you earn, and what you’re buying.

- Identity documents: Certified driver’s licence, passport, or birth certificate.

- Financial records: The last two years of business tax returns, BAS statements, and profit and loss statements.

- Property contracts: The signed contract of sale, a current valuation (if you have one), lease agreements, and rental schedules.

Keep in mind that different borrowers need slightly different checklists. A self-employed consultant, for example, will likely need a declaration from their accountant, whereas an established company will provide fully audited accounts and confirmation of their ABN/ACN registrations.

A simple pro tip? Store everything in a secure cloud folder with clear labels. Naming files by date and type makes sharing with your broker a breeze and dramatically reduces the risk of sending the wrong version.

Navigating the Pre-Approval Phase

Once your documents are sorted, your broker can lodge a pre-approval application. This isn't a final 'yes', but it's a provisional green light from the lender that shows your borrowing capacity and flags any potential gaps before you start seriously hunting for a property.

Here's how it usually unfolds:

- Your broker lodges the application with the lender and pays any upfront application fees.

- The lender reviews your credit history, asset position, and income documents.

- A conditional approval letter is issued, outlining your maximum borrowing power and any conditions.

- Pre-approval typically lasts for 90 days, giving you a solid window to negotiate a purchase with confidence.

Lenders can be particular. Some non-bank lenders are happy with digital copies, while major banks might still insist on certified hard copies. Your broker will know which is which.

While pre-approval doesn’t lock in the loan, it gives you the confidence to bid at auction or make a firm offer. It’s also the perfect time to double-check that all your information is current and correct.

Understanding Formal Approval and the Settlement Timeline

With pre-approval sorted and a contract signed, you kick off the formal approval process. This is where the lender does their deeper due diligence.

The final leg of the journey looks like this:

- A formal property valuation and legal checks are scheduled.

- The lender’s underwriting team reviews every single document in detail.

- A final loan offer is issued, specifying the interest rate, fees, and final conditions.

- You sign the loan documents and return them within the required timeframe.

- A settlement date is booked, and your conveyancer handles the release of funds.

From signing the contract to getting the keys, it's wise to budget for 4 to 8 weeks. This can vary depending on the lender's workload and the complexity of the property. Little things like zoning issues or environmental clearances can cause delays, so if your site needs a council report, get that process started early.

Coordinating your solicitor, broker, and conveyancer is crucial here. A well-aligned team prevents last-minute hurdles that could push out your settlement date.

Tips to Avoid Common Delays

Nine times out of ten, delays are caused by missing or mismatched figures. It's so important to cross-verify your BAS against your bank statements and ensure your accountant’s declaration lines up perfectly with your ATO records.

A few more tips from the frontline:

- Use consistent formatting on spreadsheets and statements.

- Label every file clearly with the date, document type, and your name.

- If you have large, one-off expenses in your financials, highlight and explain them.

- Provide a concise cash flow projection for any expected rental income.

- Let your broker know immediately if your business or personal circumstances change.

“Doing a thorough document audit with a client right at the start recently cut their approval time by three weeks. It makes all the difference.” – Sarah, Senior Broker at Diamond Lending.

Tracking Your Application’s Progress

Once lodged, it’s not uncommon for lenders to request extra information via your broker. Staying on top of these requests is key to preventing nasty surprises as settlement approaches.

- Check in with your broker for updates from the lender's portal.

- Schedule a quick weekly call with your broker to review the status and any outstanding items.

- Keep a simple tracker with condition deadlines and notes.

- Action any requests for signed documents immediately to minimise back-and-forth.

This proactive approach means you’re always on the front foot. A well-managed application almost always closes faster and with fewer headaches. This is where having a broker like Diamond Lending in your corner really pays off—we organise your entire file, chase up the lender, and act as your single point of contact. It makes the whole process feel seamless and keeps your application top-of-pile.

Finding Your Ideal Lender in Melbourne

Choosing a lender for your commercial property loan in Melbourne is one of the most critical decisions you'll make. This isn't just about getting the funds; it’s about finding a genuine financial partner whose risk appetite, policies, and loan structures line up with your specific investment or business goals.

The commercial lending landscape is far more varied than residential finance, with each type of lender bringing something different to the table.

The good news? The appetite for good commercial deals is strong. Commercial property lending across Australia has roared back, surging 9.4% year-on-year by the June quarter of 2025. This tells us that lenders are actively looking to fund quality assets and well-prepared borrowers. You can find out more about the resilience of the Australian commercial real estate market to get the full picture.

Understanding the key players—banks, non-bank lenders, and private funders—is the first step to making a smart choice.

Traditional Banks: The Major Players

When most people think of a loan, they picture the 'Big Four' or other established banks. For commercial property, they are often the first port of call because they can offer highly competitive interest rates, especially if you have an existing business relationship with them.

They’re a great fit for straightforward, low-risk applications where everything is neat and tidy.

But their biggest strength—size and scale—can also be their greatest weakness. Banks operate with very rigid, standardised credit policies. If your application doesn't tick every single box on their checklist, you’ll likely get a swift 'no', even if the deal itself is rock-solid.

Here’s what to expect from a bank:

- Strict Criteria: They heavily favour borrowers with perfect credit, consistent income documented through full financials, and properties in prime locations with strong, long-term leases.

- Slower Turnaround Times: Be prepared for a bureaucratic process. The multiple layers of assessment and credit committees mean things can move slowly.

- Lower Risk Appetite: Banks are generally more conservative with Loan to Value Ratios (LVRs) and often shy away from specialised assets like petrol stations or childcare centres without a mountain of supporting evidence.

Non-Bank Lenders: The Flexible Alternative

Non-bank lenders have become a powerful force in Melbourne's commercial finance scene, offering a crucial alternative for borrowers who don't fit the banks' narrow mould. Funded by wholesale markets or private investors, these lenders have the agility to assess deals on their individual merits.

This flexibility is a lifeline for so many excellent borrowers—think self-employed individuals with fluctuating income, recent startups, or investors eyeing a property with a short lease or a bit of vacancy. They are skilled at looking beyond a tax return to understand the real story.

A non-bank lender's approach is often more pragmatic. They focus on the strength of the asset and the borrower's overall financial story, rather than just ticking boxes on a rigid policy checklist.

While their interest rates might be slightly higher than a major bank's, their ability to get a deal approved makes them an invaluable partner for many seeking commercial property loans in Melbourne. They often provide quicker decisions and more creative structures, like capitalised interest periods or tailored repayment plans.

Private Lending: Speed and Certainty

Private lending occupies a unique and vital niche in the commercial finance world. It’s the ultimate asset-based solution. Here, the loan is secured almost entirely against the value of the property, with much less focus on the borrower's income or credit history. These loans are funded by private individuals or investment syndicates.

This makes private funding the perfect solution for:

- Time-Sensitive Deals: When you need to settle in days, not weeks, a private lender can move with incredible speed.

- Complex Scenarios: Think urgent debt consolidation, unfinished construction projects, or situations where traditional lenders simply won’t even look.

- Asset-Rich, Cash-Poor Borrowers: If your wealth is tied up in property and you need short-term liquidity, private finance is the most direct route.

The trade-off for this speed and flexibility is cost. Interest rates and establishment fees are significantly higher than bank or non-bank options. For this reason, private finance is best seen as a strategic, short-term tool—a bridge to get you to a more conventional, long-term solution once your situation has stabilised.

Think of it as a powerful problem-solver for when timing is everything. A specialist broker at Diamond Lending can help you work out if this is the right strategic move for your situation.

Understanding The True Cost Of Your Commercial Loan

When you’re looking at commercial property loans in Melbourne, it’s easy to focus on the headline interest rate. But that's only part of the story. To really get a handle on your financial commitment, you have to dig deeper into the total cost of the loan, which is packed with fees and variables that can seriously impact your budget.

Getting this right from the start means no nasty surprises down the track. A clear-eyed view of all the expenses lets you plan accurately and ensures your investment is sustainable from day one.

The Role Of Loan To Value Ratio (LVR)

The Loan to Value Ratio (LVR) is a cornerstone metric in the world of commercial lending. Put simply, it’s the percentage of the property's value a lender is willing to finance, with the rest coming from you as a deposit. Unlike residential loans where 80% or even 90% LVRs are common, commercial lending is a more conservative game.

Here’s what you can generally expect:

- Up to 70% LVR for standard commercial properties like offices or warehouses in prime Melbourne spots.

- Around 60-65% LVR for more specialised assets, such as serviced apartments or properties with unique zoning.

- Lower LVRs of 50-60% for assets that lenders see as higher risk, like vacant land or a pub.

A lower LVR means you need a larger deposit, but it also reduces the lender's risk. The upside? This can often lead to a more favourable interest rate. It's a trade-off between your initial cash outlay and your ongoing loan costs.

If a lender does agree to stretch to a higher LVR, they might ask for Lenders Mortgage Insurance (LMI). This is a one-off insurance premium that protects the lender—not you—if you can’t make your repayments. While it helps you secure a loan with a smaller deposit, it adds a significant upfront cost to your purchase.

Deconstructing Interest Rate Structures

Beyond the rate itself, how your interest is structured has a massive impact on your cash flow. You'll typically come across three main types: variable, fixed, and interest-only.

- Variable Rate: The interest rate moves up and down with the market. This gives you flexibility and potential savings if rates fall, but it also carries the risk of higher repayments if rates go up.

- Fixed Rate: Your rate is locked in for a set period, usually 1 to 5 years. This delivers certainty for your budget but means you won't benefit if market rates drop.

- Interest-Only: For a set term, your repayments only cover the interest, not the principal loan amount. This maximises your cash flow in the short term, which is why it's popular with investors and developers who plan to sell or refinance.

Choosing the right structure is all about your strategy. An owner-occupier might prefer the stability of a fixed rate, while an investor planning to renovate and sell would find an interest-only period far more beneficial.

Don't Overlook The Upfront Fees

The expenses that often catch borrowers by surprise are the various setup fees. These can add up fast, so it's vital to factor them into your initial budget.

Key fees you need to account for include:

- Application Fee: An upfront charge from the lender just for processing your application.

- Valuation Fee: The cost of an independent valuer assessing the property's market worth. This can range from $2,000 to $5,000+, depending on how complex the property is.

- Legal Fees: Both your solicitor and the lender's will have fees for handling the contracts and settlement.

- Stamp Duty: This is usually the biggest upfront cost, calculated as a percentage of the property’s purchase price.

For a clearer picture of these expenses, our property buying cost calculator can help you estimate the total funds you'll need.

In Melbourne's bustling commercial property scene, the industrial sector is showing impressive stability. As of March 2025, yields are holding firm at 6.00% for prime industrial assets and 6.75% for secondary ones, reflecting sustained investor appetite. This market stability makes precise budgeting even more critical.

By understanding every component of the loan's cost, you move from just getting finance to making a truly informed financial decision. A good broker can help you compare loan products holistically, ensuring you choose a solution that's not just affordable today but profitable for years to come.

Answering Your Top Questions on Melbourne Commercial Loans

Even seasoned investors have questions when it comes to commercial property finance. It’s a different beast to residential lending. To give you total clarity, here are some straight answers to the most common queries we get from our Melbourne clients. Think of it as your final checklist before you dive in.

Can I Use My SMSF to Buy a Commercial Property?

Yes, absolutely. Using your Self-Managed Super Fund (SMSF) to buy a commercial property is a powerful and popular strategy, especially for business owners looking to purchase their own premises. It's a smart way to build your retirement nest egg, as your business pays rent directly into your super fund.

But be warned: the rules are incredibly strict. The loan has to be set up under a Limited Recourse Borrowing Arrangement (LRBA). This is non-negotiable, as it protects the other assets in your super fund if things go wrong. Lenders have very specific criteria for SMSF loans, and getting the structure right from day one is critical.

How Much Deposit Do I Really Need for a Commercial Loan?

This is the million-dollar question, and the answer is nearly always, "it depends." Forget the 20% deposit that's common in the residential world; that's rarely enough for a commercial property.

As a general rule, you should plan for a deposit of at least 30% for a standard commercial property in Melbourne.

- For more specialised assets like childcare centres or service stations, lenders will likely ask for 40%, sometimes even 50%.

- A larger deposit doesn't just get you across the line—it strengthens your application and can unlock more competitive interest rates.

Your deposit shows you have skin in the game and reduces the lender's risk, making it one of the most important parts of your application.

How Long Does the Approval Process Take?

Patience is a virtue in commercial finance. The timeline can vary wildly depending on the lender and how complex your deal is. It's certainly not as quick as your typical home loan.

As a rule of thumb, it’s wise to allow between 4 to 8 weeks from submitting your formal application to settlement. The major banks often take longer because of their multiple layers of approval, whereas non-bank and private lenders can sometimes move much faster for the right kind of deal.

Most delays come down to two things: incomplete paperwork or a complex property valuation. Being organised from the get-go is the single best way to keep things moving forward.

What Happens if My Property Is Vacant?

An empty property means no rental income, and that naturally makes lenders nervous. But it's not an automatic deal-breaker. If you're buying a vacant commercial asset, you’ll just need to present a much stronger business case.

Lenders will want to see:

- A rock-solid financial position, proving you can cover the loan repayments for a period without any rent coming in.

- A clear, well-researched strategy for securing a tenant, backed up by market data on local vacancy rates and potential rental yields.

- A larger deposit to help offset their increased risk.

Ultimately, you need to show them a clear and believable path to profitability. That's the key to getting a loan approved for a vacant property.

Ready to take the next step? The team at Diamond Lending has the specialist expertise to structure the right commercial finance for your Melbourne property goals. Book a no-obligation 15-minute call today to discuss your scenario and get expert advice tailored to you.