Diving into the world of commercial property finance can feel like a huge undertaking, but landing the right loan is absolutely achievable once you understand what lenders are actually looking for. At their core, commercial property loan requirements in Australia boil down to three things: your financial strength, the property’s viability, and your credibility as a borrower.

Think of this guide as your roadmap to a successful application.

Your Guide to Securing Commercial Property Finance

Applying for a commercial property loan is a bit like pitching to a business partner. You’re not just asking for money; you’re presenting a compelling case that shows the investment is sound and that you’re a reliable partner capable of managing it. Lenders aren’t just looking at numbers on a page—they’re assessing risk and potential from every angle.

The whole process is designed to build confidence. A lender needs to be completely certain you can meet your repayment obligations and that the property itself is a valuable, secure asset. This guide is here to demystify those requirements, breaking them down into clear, manageable concepts.

The Core Pillars of Assessment

To kick things off, lenders will evaluate your application based on a few fundamental pillars. These really form the foundation of their entire decision-making process.

- Your Financial Position: This covers both your business and personal financial history. Lenders want to see clear evidence of stability, responsible credit management, and that you have sufficient cash or equity on hand.

- The Property's Potential: The commercial property itself is a massive part of the equation. Its location, type, condition, and, most importantly, its income-generating potential will be scrutinised.

- Your Credibility and Experience: Your track record matters. If you have previous experience in business or property investment, it can seriously strengthen your application.

A well-prepared application tells a story of stability and foresight. It shows not just that you can afford the loan now, but that you have a solid plan for managing the asset long into the future.

We’ll explore each of these elements in much more detail. But first, let’s get a quick high-level overview.

The table below gives you a snapshot of the key requirements you'll encounter. Use it as a handy reference point as we dive deeper into each component, getting you ready to move forward with total confidence.

Key Commercial Loan Requirements at a Glance

Here’s a quick summary of what Australian lenders typically assess when you apply for a commercial property loan.

| Requirement Category | What Lenders Look For | Typical Benchmark |

|---|---|---|

| Eligibility & Credit | Clean credit file, stable business history (e.g., ABN registered for 2+ years). | Good to Excellent credit score (650+). |

| Documentation | Tax returns, business financials (P&L, Balance Sheet), ATO records, personal ID. | 2 years of financial statements. |

| Deposit (LVR) | The amount of your own capital contributed towards the purchase. | 60-80% LVR (Loan-to-Value Ratio). |

| Serviceability (DSCR) | Proof the property’s income (or your business income) can cover the loan repayments. | DSCR of 1.25x or higher. |

| Security & Valuation | An independent valuation of the property confirming its market value and suitability. | Valuation must support the purchase price. |

| Experience & Credibility | Your background in property investment or running a similar business. | Relevant industry experience is highly valued. |

This table provides a great starting point, but the real magic is in the details. Understanding why lenders ask for these things is the key to building a bulletproof application.

The Five Pillars of Commercial Loan Eligibility

Imagine you’re pitching a major project to a new business partner. You wouldn’t just show them the final blueprint. You’d have to prove your own credibility, the financial health of your current operations, and the long-term viability of the venture itself. Securing finance for a commercial property follows the exact same logic.

Lenders in Australia don’t just look at one part of your application; they assess it based on five core pillars. Each pillar tells a different part of your financial story. A strong application shows stability across all five, turning a sceptical lender into a confident financial partner. Getting your head around these pillars is the first real step to mastering the commercial property loan game.

Pillar 1: The Borrower Profile

Before a lender even glances at your business figures or the property details, they start with you. Your personal financial history and professional background are the bedrock of their assessment. They need to see a proven track record of responsible financial management.

This means a deep dive into your credit history. A clean credit file, free from defaults or late payments, signals reliability. Lenders also place huge value on experience; if you have a background in managing businesses or owning investment properties, it gives your application a massive credibility boost.

Think of your borrower profile as your financial CV. It’s your chance to prove you’re a low-risk individual with the discipline and experience to manage a significant commercial debt.

Pillar 2: Business Financial Health

If you're buying a property to run your business from (an owner-occupier loan) or using business income to service the debt, the financial health of your company is non-negotiable. This pillar is all about historical performance and future stability. Lenders want to see consistent profits and healthy cash flow.

Typically, they’ll ask for at least two years of financial statements, including Profit and Loss (P&L) statements and Balance Sheets. These documents prove that your business is not just ticking over but generates enough surplus income to handle new debt. A strong, upward trend in revenue is one of the most powerful indicators you can provide.

Pillar 3: Property Suitability

The property itself is a critical piece of the puzzle. It’s the primary security for the loan, so lenders will scrutinise its value, type, and location to make sure it’s a sound investment. A formal valuation from an approved, independent valuer is a mandatory part of this process.

Lenders will assess several key property characteristics:

- Location: Is it in a high-demand metro area or a quiet regional town? Prime locations with low vacancy rates are always preferred.

- Property Type: A standard office, warehouse, or retail space is generally seen as lower risk than a specialised asset like a hotel or a petrol station.

- Lease Profile: For investment properties, the strength of existing tenants and the length of their leases (known as the WALE or Weighted Average Lease Expiry) are vital signs of income security.

Pillar 4: Your Equity Contribution

This pillar is all about what you bring to the table. Lenders need to see that you have "skin in the game," which is measured by your deposit or equity contribution. This is shown as the Loan-to-Value Ratio (LVR), a simple calculation comparing the loan amount to the property's value.

A lower LVR (meaning a bigger deposit) reduces the lender's risk and makes your application far more attractive. While some lenders might stretch to an 80% LVR for prime properties, a more common benchmark for commercial loans is between 60% and 70%. This shows you have the financial capacity to contribute a serious amount of your own capital.

Pillar 5: Proven Serviceability

Finally, and most importantly, is serviceability. This is your proven ability to meet the loan repayments, month in and month out, without stress. Lenders need absolute confidence that the income generated—either by your business or the property itself—can comfortably cover the debt.

They measure this using the Debt Service Coverage Ratio (DSCR), which we'll break down in a later section. In Australia's commercial property market, standards are selective. For investors, lenders often demand LVRs of 60-70% and proof that net operating income can cover the debt by 125-150%. Banks are increasingly favouring premium assets with low vacancy rates, showing just how much property quality impacts your application's success. You can explore more about what these trends mean for the Australian commercial property market.

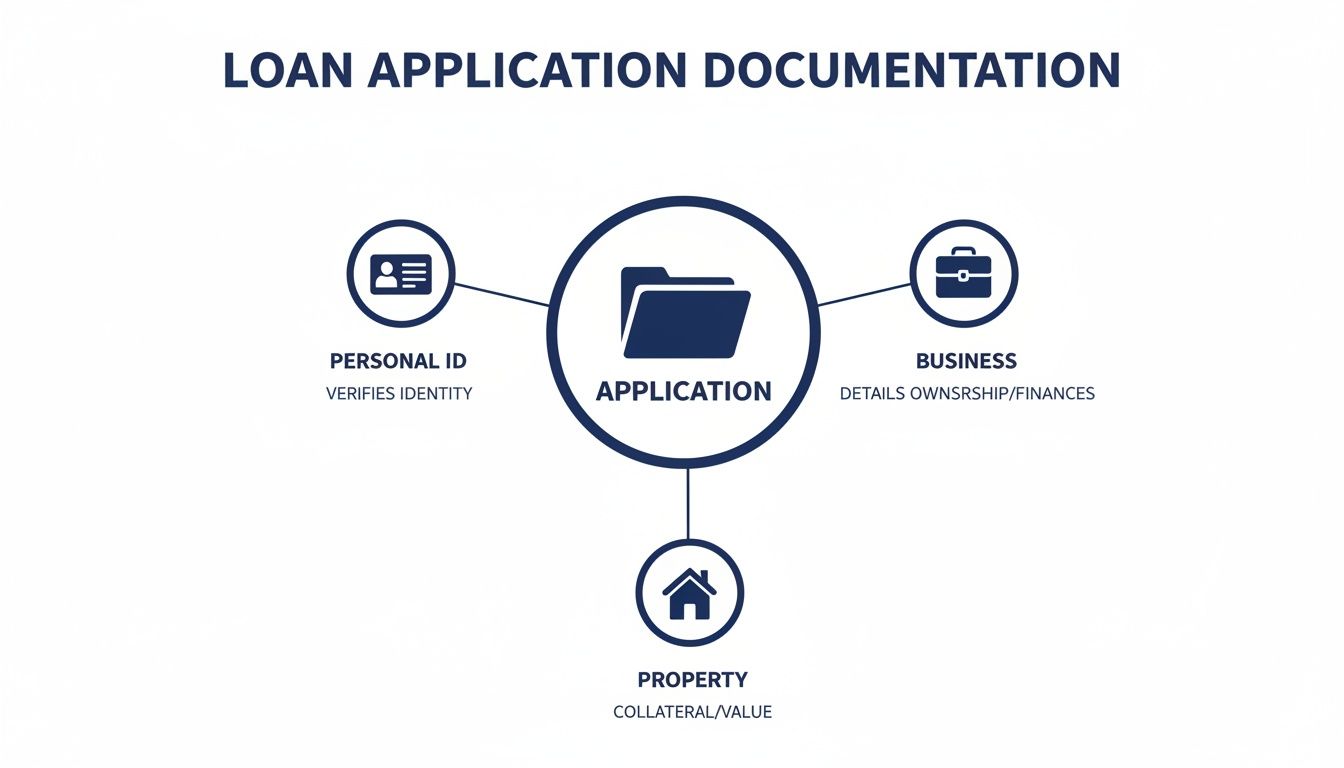

Getting Your Paperwork Together: The Essential Document Checklist

Alright, let's move from theory to action. It’s time to gather your documents. Think of this less like a chore and more like building your case. You're telling a story to the lender—a story about your financial reliability and business savvy. Every document you provide is a piece of evidence that proves you're a good bet.

Being organised here isn't just a good look; it saves you time and headaches. A clean, complete application shows the lender you're serious and professional, which can seriously speed up the approval process.

Who Are You? Personal and Business ID

First things first, the lender needs to know exactly who they're dealing with. This is the baseline check that confirms the identity of everyone involved and the legal structure of your business. The application can't go anywhere without it.

You’ll need to have these ready:

- Photo ID: A current driver’s licence or passport for all company directors, trustees, or individuals on the loan.

- Business Details: For a company, this means your ACN (Australian Company Number) and the trust deed if you're using a trust structure. If you’re a sole trader, you'll just need your ABN (Australian Business Number).

This step is all about making sure the contract is with the right legal entities. It’s a simple but non-negotiable part of the process.

Proving Your Financial Track Record

This is the heart of your application. Here, you lay out your financial health for the lender to see. They're looking for a clear history of your income, expenses, assets, and liabilities to see a stable and profitable track record.

The key documents lenders will ask for include:

- Tax Returns: Be prepared with your last two financial years of both personal and business tax returns.

- Financial Statements: You'll also need the last two years of Profit & Loss (P&L) statements and Balance Sheets for your business.

- ATO Records: An up-to-date statement from the Australian Taxation Office (ATO) portal is a common request to show you don't have any outstanding tax debts.

These documents are more than just numbers on a page. They tell the story of your business's journey. A solid history of profit and keeping things clean with the ATO builds a massive amount of trust with any lender.

Information on the Property Itself

Once the lender is comfortable with you and your business, their attention turns to the property you want to buy. The property is the ultimate security for the loan, so they’ll scrutinise its value and its ability to generate income.

Get these property-specific documents ready:

- Contract of Sale: The fully executed contract that details the purchase price and any conditions of the sale.

- Lease Agreements: If it's an investment property, the lender needs copies of all current lease agreements to verify the rental income you’ve declared. A simple rental schedule summarising the tenants, lease terms, and income is also incredibly helpful.

This information gives the lender what they need to do their own homework, which always includes ordering an independent valuation to confirm the property is worth what you’re paying.

What if You’re Self-Employed? Navigating Low Doc Loans

What happens if you're self-employed and don't have two years of squeaky-clean financials? This is exactly where low documentation (low doc) loans come into play. They’re designed for borrowers who have a strong income, but it just doesn't show up neatly on a standard tax return.

Instead of full financials, low doc lenders can accept other forms of proof:

- Business Activity Statements (BAS): Your last 12 months of lodged BAS are a great way to show consistent business turnover.

- An Accountant's Letter: A signed letter from your accountant confirming your income can be a powerful piece of evidence.

- Business Bank Statements: Providing six to twelve months of statements that show regular cash flow is another common alternative.

Low doc loans are a crucial option for entrepreneurs and self-employed professionals, acknowledging that a successful business doesn't always fit into a bank's standard paperwork box.

Understanding Serviceability and LVR Calculations

Once your paperwork is in, a lender’s attention snaps to two numbers that really decide your fate: the Loan-to-Value Ratio (LVR) and the Debt Service Coverage Ratio (DSCR).

Forget the jargon for a second. These are the core metrics that tell a lender how much you can borrow and how much confidence they can have in your deal. Getting your head around these is non-negotiable if you want to structure a successful application.

Think of it like this: LVR is your entry ticket—it proves you have enough skin in the game. DSCR is the endurance test—it proves your investment can actually pay its own way over the long haul.

All the documents you pull together—from your driver's licence to your business financials—are just ingredients for these two critical calculations. This diagram shows how it all fits together.

As you can see, every piece of information connects to build the complete financial picture the lender needs to see.

Decoding the Loan to Value Ratio

The Loan-to-Value Ratio (LVR) is a simple but powerful measure of risk. It just shows how big your loan is compared to the property's market value.

Formula: Loan Amount / Property Value = LVR

A lower LVR means you’re putting in more of your own money, which makes any lender breathe a lot easier. It massively reduces their exposure if things go sideways.

For example, if you want to borrow $700,000 for a warehouse valued at $1,000,000, your LVR is 70%. This means you're fronting a 30% deposit of $300,000. Most commercial lenders in Australia draw the line at around 65-70% LVR for standard properties. For more specialised assets like a motel or childcare centre, they'll likely pull that back to 50-60%.

Want to see how different LVRs and loan terms could impact your repayments? Have a play with our commercial property loan calculator.

The All-Important Debt Service Coverage Ratio

While a good LVR gets you in the door, the Debt Service Coverage Ratio (DSCR) is what truly sells your deal. This metric shows whether the property can generate enough income to cover its own loan repayments.

A strong DSCR proves the investment is financially viable on its own two feet.

Formula: Net Operating Income (NOI) / Total Annual Debt Service = DSCR

Your Net Operating Income (NOI) is all the cash the property brings in (like rent) after you subtract its running costs (like rates, insurance, and maintenance). Your Total Annual Debt Service is simply the total of your principal and interest payments for the year.

Lenders see a DSCR of 1.25x or higher as the gold standard. It means for every $1.00 of debt, the property is generating $1.25 in net income. That extra 25% is the cash flow buffer that gives them comfort.

How Lenders Stress-Test Your Application

Lenders are paid to be cautious. They won't just look at whether you can afford the loan at today's interest rates; they'll stress-test your application to make sure you can handle future bumps in the road.

This is a critical hurdle to clear, and they do it in two main ways:

- Applying an Interest Rate Buffer: They'll run the numbers on your repayments using an interest rate that’s 2-3% higher than the actual rate on offer. This is to ensure you don’t fall over if rates rise.

- Shading Rental Income: Lenders will often "shade" or discount the property's rental income by 10-20% in their calculations. This builds in a buffer for potential vacancies or a tenant falling behind on rent.

This careful approach is standard practice. Right now, you’ll find most lenders capping LVRs at 65-70% for quality commercial deals, with a laser focus on keeping that DSCR above 1.25x. To get across the line, borrowers need to come armed with a solid valuation and prove the property has strong rental yields to meet these tough but necessary criteria.

Comparing Your Lender Options: Banks vs. Non-Banks vs. Private Lenders

Choosing a lender for your commercial property isn't just about chasing the lowest rate; it's about finding a financial partner who actually understands your specific scenario. The Australian lending landscape is a lot bigger than just the big four banks. Each type of lender has its own unique appetite for risk, approach to paperwork, and level of flexibility.

Figuring out these differences is the key to knowing where your application will not only be accepted but genuinely welcomed.

The Big Banks: The Traditional Route

For many borrowers, the major banks are the first port of call. It makes sense. They're known for their conservative, risk-averse approach, which can translate into sharp interest rates if you fit their mould perfectly.

Think straightforward applications for standard properties, like a warehouse or office in a metro area. If you’ve got a long, stable trading history, spotless tax returns for the last two years, and a perfect credit file, a major bank can be a fantastic option.

The problem is, their policies are often rigid and unforgiving. Their credit models are built on black-and-white rules, leaving little room for nuance. This is where many self-employed borrowers, businesses with fluctuating income, or anyone buying a unique property type hit a brick wall. This is exactly where the other lenders step in.

The Rise of Non-Bank Lenders

Over the last decade, non-bank lenders have become a serious force in commercial finance, offering a more flexible, common-sense alternative to the big banks. Because they're regulated differently, they can assess applications on a case-by-case basis. They don't just feed your numbers into a computer; a real person looks at the whole story.

This means they’re often a much better fit for:

- Self-employed applicants who might not have two years of squeaky-clean tax returns.

- Borrowers with a few minor credit blemishes in their past that don't reflect their current situation.

- Investors purchasing specialised properties like pubs, service stations, or childcare centres that banks often shy away from.

Yes, their interest rates might be a fraction higher to account for this tailored risk assessment, but their ability to understand and solve complex financial puzzles is invaluable. They’re experts at crafting solutions where a traditional bank would have simply said "computer says no."

The right lender isn't always the biggest one. It's the one whose lending appetite and policies align perfectly with your financial story and investment goals.

When Private Lenders Are the Answer

Private lenders operate in a completely different world. They provide short-term, solution-focused finance for situations that are either too complex or too urgent for anyone else.

Think of them as the special forces of finance. You bring them in when speed and certainty are everything—like securing a property at a snap auction, funding a development when your bank pulls out, or bridging a gap between buying and selling.

Their commercial property loan requirements are less about your historical paperwork and almost entirely about the strength of the asset. They focus heavily on the property's value and, most importantly, your exit strategy. How are you going to pay them back? Usually, it's by refinancing to a traditional lender once the situation has stabilised or by selling the property.

This incredible flexibility comes at a price, with higher interest rates and fees. But for the right deal, they provide a vital pathway to funding that would otherwise be impossible. Understanding the diverse commercial property loans in Melbourne can help local investors see just how these different lender types cater to the city's fast-moving market.

To make it easier to see where you might fit, here’s a clear breakdown of what to expect from each.

Commercial Lender Comparison

This table gives you a snapshot of the typical requirements and characteristics of the main lender types in the Australian commercial property space.

| Lender Type | Typical LVR | Documentation | Best For | Interest Rate |

|---|---|---|---|---|

| Major Banks | Up to 75% | Full financial statements, two years of tax returns, clean credit history. | Low-risk borrowers with standard properties and perfect documentation. | Most Competitive |

| Non-Bank Lenders | Up to 70% | More flexible; can use BAS, accountant letters, or bank statements. | Self-employed, unique property types, or those with minor credit issues. | Competitive |

| Private Lenders | Up to 65% | Minimal focus on income history; primarily based on asset value and exit strategy. | Urgent funding, development projects, or complex scenarios requiring speed. | Higher |

As you can see, the "best" lender is entirely relative. It all comes down to aligning your personal circumstances, the type of property you're buying, and your overall goals with the lender who is best equipped to support them.

Your Next Steps to a Successful Loan Application

Knowing the theory behind commercial property loan requirements is a great start, but turning that knowledge into a successful application is where the real work begins. It’s time to shift from learning to doing.

Let's be clear: a well-prepared and strategically guided application has a much higher chance of success. The goal here is to walk into your commercial property purchase with confidence and a clear plan. By taking a few deliberate steps now, you can sidestep common pitfalls and build a compelling case for any lender, whether it’s a major bank or a specialist non-bank.

Create Your Action Plan

Before you even think about speaking to a lender, the most powerful move you can make is to get your own house in order. Being proactive not only speeds things up but also shows lenders you’re an organised and serious borrower.

Start by pulling together the key documents we’ve covered. This isn't just a paper-shuffling exercise; it’s about looking at your information through a lender's eyes.

- Organise Your Financials: Get your last two years of business tax returns, plus your company’s profit and loss statements and balance sheets.

- Verify Your Position: Pull a copy of your credit file to check for errors and make sure your ATO obligations are completely up to date. No surprises.

- Summarise Your Story: Write a brief summary of your business experience and what you plan to do with the property. This narrative gives crucial context to all the numbers.

Seek Professional Guidance Early

Trying to navigate the maze of commercial finance on your own can be tough. Bringing a finance broker on board early isn't a last resort—it's a strategic advantage. An experienced broker is your advocate, framing your application in the best possible light.

"Begin the process with your lender early and ensure it aligns with your current and future business needs and goals."

This is crucial advice. A good broker can help you figure out your true borrowing power, spot potential red flags in your application before a lender does, and match you with the right lender whose policies actually fit your situation. This step alone can save you from the frustration of applying to lenders who were never going to say yes in the first place.

Take the First Step Today

You now have a solid understanding of what it takes to get a commercial property loan. The next logical move is to take that first, decisive step. A simple conversation can clarify exactly where you stand and set you on the right path.

Whether you're ready to apply now or just want to explore your options, a quick 15-minute chat with an expert can provide huge clarity. At Diamond Lending, we can assess your situation, answer your specific questions, and map out a clear strategy to help you nail your commercial property goals.

Got Questions About Commercial Loans? We've Got Answers.

When you're diving into the world of commercial property, a few key questions always come up. Here are some straightforward, no-jargon answers to the things we hear most often from our clients.

What’s the Minimum Deposit for a Commercial Property Loan in Australia?

As a general rule, you should plan for a deposit of at least 30% of the property's value. This means you'll be borrowing 70% of the value, which lenders refer to as the Loan-to-Value Ratio (LVR).

But this isn't set in stone. The final number really depends on the lender and what kind of property you’re buying.

If you're looking at something more specialised, like a pub or a childcare centre, lenders see more risk. Because of that, they'll likely ask for a bigger deposit, sometimes as high as 40-50%. On the flip side, if you're buying a standard office or warehouse in a major city and your application is rock-solid, some lenders might stretch to an 80% LVR. That means you'd only need a 20% deposit.

How Do Lenders Figure Out My Borrowing Power for a Commercial Loan?

It all comes down to one thing: can the property's income comfortably cover the loan repayments? Lenders measure this using a key metric called the Debt Service Coverage Ratio (DSCR). The formula is simple: it's your Net Operating Income (NOI) divided by your total yearly loan repayments.

Most lenders want to see a DSCR of at least 1.25x. In plain English, this means your net income needs to be 25% higher than your loan payments. They’ll pore over your business financials and the property's income projections, then "stress-test" those numbers to see if you could still make repayments if interest rates were to rise. That final, stress-tested figure determines how much you can borrow.

Your borrowing power isn't just a number; it's a reflection of the lender's confidence in your investment's ability to generate sufficient cash flow to comfortably meet its financial obligations, even in a changing economic climate.

Can I Get a Commercial Property Loan with Bad Credit?

Yes, you absolutely can. However, your journey will look a little different. Forget the major banks; your best bet will be with specialist non-bank or private lenders who are more flexible.

These lenders are less focused on a past mistake and more interested in the story behind it. They'll want to see that whatever caused the credit issue is resolved and that your financial situation is back on track.

Be prepared for stricter terms. You'll likely need a larger deposit (meaning a lower LVR) and will face higher interest rates to balance out the lender's risk. This is where a good finance broker is worth their weight in gold. They have direct lines to lenders who specialise in credit-impaired commercial finance and know exactly how to navigate their unique requirements.

Ready to turn your commercial property goals into reality? The team at Diamond Lending has the real-world experience to guide you through every stage, from figuring out your borrowing power to locking in the right finance for your unique situation. Book a quick, no-obligation chat with our specialists today and walk away with a clear action plan.