A business mortgage loan is essentially a home loan for your company's physical address. It’s a specialised loan that helps you buy, refinance, or even develop commercial property, whether that's an office, a warehouse, or a retail storefront.

Think of it as the ultimate strategic move: shifting from being a tenant to becoming an owner, and turning a monthly expense into a powerful asset.

Unlocking Growth with a Business Mortgage Loan

Imagine your business has been growing in a rented pot. It's done the job, but you're paying someone else for the privilege, the rent keeps climbing, and you can't really stretch out. A business mortgage is like buying your own plot of land. Suddenly, your business has solid ground to put down roots, grow without limits, and truly thrive.

Instead of your hard-earned money disappearing into a landlord's pocket, your repayments start building equity in an asset you actually own. This simple switch from renting to owning gives you stability and, most importantly, control. You can renovate, expand, or customise the space to perfectly fit your operations—all without needing a landlord's permission slip.

The Core Purpose of a Commercial Property Loan

At its heart, a business mortgage loan is a long-term financial agreement that’s secured against the commercial real estate itself. Because the property acts as collateral, it lowers the lender's risk, which often translates to better loan terms compared to unsecured business finance.

But it’s important to remember this funding is laser-focused. You can’t use it to cover payroll or buy new stock; its one and only job is to finance property.

Key uses include:

- Purchasing new premises to run your business from, like a professional office suite, an industrial warehouse, or a high-street shop.

- Refinancing an existing commercial mortgage, usually to lock in a better interest rate or tap into the equity you've built up over the years.

- Expanding your current footprint by financing the purchase of a bigger building or the unit next door to accommodate your growth.

- Developing a commercial property from scratch, which often starts as a specialised construction loan before converting to a standard mortgage once the build is complete.

Why Ownership Matters More Than You Think

Owning your commercial premises does more than just put a roof over your operations; it becomes a cornerstone of your company's financial strength. It insulates you from surprise rent hikes or the dreaded news that your lease won't be renewed. That kind of operational certainty is priceless.

And it doesn't stop there. A commercial property can even become an extra source of income. If you buy a building with more space than you need right now, you can lease out the extra offices or storefronts. This creates a brand-new revenue stream that can help pay down your mortgage and boost your bottom line.

A business-owned property is not just an expense; it's a strategic asset on your balance sheet. As you pay down the loan and the property appreciates in value, you build significant equity that can be leveraged for future business investments or expansion projects.

Ultimately, a business mortgage loan is a foundational step towards long-term stability and creating real wealth for your company. It transforms rent—one of your biggest expenses—into a powerful investment in your future. For any business owner looking to establish a permanent footprint, this is an essential tool.

Exploring Different Types of Commercial Property Loans

Navigating the world of business mortgage loans can feel a bit like choosing a vehicle for a job. You wouldn't use a sports car on a construction site, right? In the same way, the right commercial property loan has to match your business's unique circumstances, its financial story, and where you're headed.

Getting your head around the different options is the first real step to securing finance that actually works for you, not against you.

For most established businesses, the journey starts with a full-documentation (full-doc) loan. This is the traditional path, built for companies that have a solid, consistent trading history and the clean financial records to back it up.

Think of a thriving local cafe that’s been leasing its spot for years. The owners have kept meticulous books, showing steady profits and a strong financial position. A full-doc loan is the perfect fit for them to finally buy the building because they can easily hand over the tax returns, profit-and-loss statements, and balance sheets to prove they can service the debt.

Flexible Options for Non-Traditional Businesses

But what about businesses that don’t fit neatly into that traditional box? Plenty of self-employed people, freelancers, and newer companies have healthy cash flow, but they might not have two years of pristine financials ready to go. This is where more flexible solutions come into play.

Low-documentation (low-doc) loans offer a different way to prove your strength. Instead of digging through years of complex financials, lenders will look at other forms of income verification.

A low-doc loan isn't a "no questions asked" free-for-all. It's a specialist product for strong applicants whose income story is better told through documents like Business Activity Statements (BAS), a declaration from their accountant, or their business bank statements, rather than old tax returns.

This is ideal for someone like a freelance graphic designer who wants to buy a small studio. Their income is great but fluctuates with projects, so a standard tax return doesn't tell the whole story. A low-doc loan allows them to secure a mortgage by showing consistent cash flow right from their business bank accounts.

Then you have no-documentation (no-doc) loans. These are much rarer and almost always require a hefty deposit (meaning a lower Loan-to-Value Ratio, or LVR). They rely on the borrower's self-certified income declaration without needing traditional paperwork, making them a niche option for borrowers with significant equity.

Specialised Loans for Unique Projects

Beyond simply buying a property, specialised business loans are built for specific goals. One of the most common is a construction loan, designed for businesses looking to build their premises from the ground up or undertake a major renovation.

Unlike a standard mortgage where you get a lump sum, a construction loan pays out the money in stages, known as progress payments. These payments are tied to key building milestones—like laying the foundation, putting up the frame, and finishing the internal fit-out. This structure protects everyone involved, ensuring the funds are used correctly as the project unfolds.

To help you see the differences at a glance, here’s a simple breakdown of the main loan types.

Comparing Business Mortgage Loan Types

| Loan Type | Best For | Typical Documentation | Key Feature |

|---|---|---|---|

| Full-Doc Loan | Established businesses with 2+ years of clean financial records. | Full tax returns, profit & loss statements, balance sheets. | Often secures the most competitive interest rates. |

| Low-Doc Loan | Self-employed, freelancers, or businesses with irregular income. | BAS, accountant's declaration, business bank statements. | Flexible income verification for strong cash flow businesses. |

| No-Doc Loan | Borrowers with a very large deposit and non-traditional income. | Self-certified income declaration. | Minimal paperwork but requires a low LVR (high deposit). |

| Construction Loan | Building new premises or funding major renovations. | Building contracts, council plans, cost estimates. | Funds released in stages (progress payments) to match milestones. |

Choosing the right structure is about aligning the loan’s features with your business’s reality. An established retail store and a start-up construction firm have completely different needs, and thankfully, there are different tools for each job.

The Australian mortgage lending market, which includes all these options, reached an estimated AUD 383.90 billion, with conventional full-doc loans still leading the charge. Forecasts predict massive growth, with the market potentially expanding to nearly AUD 1,004.83 billion over the next decade.

Understanding where you fit in this landscape is crucial. By exploring the full range of commercial loan types, you can make a much more strategic decision for your company's future.

Qualifying for a Business Mortgage Loan

Getting a business mortgage isn't just about filling in forms. It’s about telling a clear, compelling story of your company’s financial stability. Lenders are looking for confidence and consistency, so knowing what they value is the first step to building an application that gets a 'yes'. Think of it as creating a business plan, but for your property goals.

The process goes well beyond a glance at your bank balance. Lenders dig into the complete picture—from your trading history and profitability to the personal credit standing of the company directors. Every document you provide adds another piece to the puzzle, helping them measure the risk and trust your ability to handle repayments for the long haul.

The Foundations of Lender Approval

When a lender assesses your application, they're really focused on two things: your ability to repay the loan and the quality of the property you’re offering as security. They use a few key metrics to make this call, and a strong application shows stability across the board.

Here’s what they’re looking for:

- Business Financials: Lenders will want to see at least two years of financial statements, including your profit and loss reports and balance sheets. They’re searching for a track record of consistent profits and reliable cash flow.

- Credit History: Both the business's credit file and the personal credit histories of all directors will be closely reviewed. A clean record is a powerful signal of responsible financial management.

- Director Experience: Your time and expertise in your industry really matter. A long track record gives lenders confidence that you know how to navigate market shifts and run the business successfully.

- Deposit Size: The amount of your own money you can put in directly affects your Loan-to-Value Ratio (LVR). A bigger deposit lowers the lender's risk and makes your application much stronger.

Understanding Your Loan-to-Value Ratio

The Loan-to-Value Ratio (LVR) is one of the most critical numbers in any business mortgage application. It’s a simple percentage that shows how much you’re borrowing compared to the property's value. For a lender, it's their main gauge for risk.

For example, if you're buying a commercial property valued at $1,000,000 and the lender agrees to a loan of $700,000, your LVR is 70%. That means you need to come up with a deposit of $300,000 plus extra funds to cover costs like stamp duty and legal fees.

A lower LVR (which means a larger deposit) makes your application far more attractive. Most lenders will cap commercial LVRs at around 65-80%, and this often depends on the type of property and where it is. For instance, a warehouse in a prime industrial area might get a higher LVR than a specialised rural property. Getting a solid deposit together is one of the best things you can do to boost your chances of approval and lock in better loan terms.

For a broader look at securing finance, our guide on how to get a business loan offers more context.

Navigating Common Hurdles with Confidence

Let's be realistic—not every business has a perfect, two-decade-long financial history. Lenders get this, and there are pathways for businesses in different situations. The key is to be upfront and present your case clearly.

For new businesses (trading for less than two years), lenders will lean more heavily on the directors' personal finances, their experience in the industry, and detailed financial projections. A solid business plan demonstrating a clear path to profitability becomes absolutely essential.

Self-employed applicants can hit roadblocks if their income isn't regular. This is where low-doc loan options are a game-changer, allowing you to prove your cash flow with Business Activity Statements (BAS) or bank statements instead of standard tax returns.

Even a complicated financial history or past credit issues don't have to be a deal-breaker. If you can provide a clear explanation for what happened and show that your business is now on stable ground, you can still build a powerful case for a business mortgage. In these situations, transparency is your best friend.

Understanding the True Cost of Your Loan

When you’re looking at a business mortgage, the interest rate is often the headline number that grabs all the attention. But focusing on that alone is like judging a car by its paint job—it tells you nothing about what’s really going on under the bonnet.

The true cost of your loan is a blend of upfront fees, ongoing charges, and the interest itself. Getting a handle on all these moving parts is the only way to budget properly and avoid nasty surprises down the track.

Think of the advertised interest rate as the base price. Before you even think about your first repayment, you’ll run into a series of setup costs. These are a normal part of securing commercial property and need to be paid out-of-pocket, separate from your deposit.

Peeking Beyond the Interest Rate

To get the full financial picture, you have to account for everything. Lenders all have different fee structures, and a loan that looks like a great deal on the surface can quickly become less appealing once you add up all the extras.

Common upfront fees usually include:

- Application or Establishment Fees: This is a one-off charge from the lender to get your business mortgage processed and set up.

- Valuation Fees: The lender needs an independent valuation of the commercial property to confirm what it’s worth. You’ll be the one covering the cost of this report.

- Legal Fees: There are costs from both your own conveyancer and the lender’s legal team for preparing, reviewing, and settling all the mortgage paperwork.

These initial costs can easily run into thousands of dollars, so getting a clear estimate from your lender or broker right from the start is non-negotiable for smart budgeting.

Fixed vs. Variable Rates: The Impact on Your Cash Flow

Once your loan is up and running, the interest rate becomes your biggest ongoing cost. The choice between a fixed and a variable rate directly impacts your business’s monthly cash flow and how well you can plan for the future.

A fixed interest rate locks in your rate for a set period, usually one to five years. This gives you absolute certainty. Your repayments won't change, which makes budgeting a breeze. The downside? You won’t get any benefit if market rates drop, and breaking a fixed-term loan can come with hefty fees.

On the other hand, a variable interest rate moves up and down with the market. This gives you more flexibility and the chance for your repayments to fall if rates go down. The trade-off is the lack of predictability; if rates climb, so will your repayments, putting a squeeze on your cash flow.

The decision between fixed and variable isn't just about the numbers; it's about your business's appetite for risk. A new business might value the stability of a fixed rate, while a more established company might be comfortable with the flexibility that a variable rate offers.

How Lenders Determine Your Rate

The final interest rate you’re offered isn’t just pulled out of a hat. Lenders carefully weigh up several factors to figure out how much risk your application represents. The higher they perceive the risk, the higher your interest rate will likely be.

Key things that influence your rate include:

- Loan-to-Value Ratio (LVR): A lower LVR (which means you’re putting down a larger deposit) reduces the lender's risk and usually scores you a more competitive interest rate.

- Property Type: A standard office or warehouse is generally seen as a safer bet than a highly specialised property like a petrol station or a motel.

- Business Financials: A strong history of profit and consistent cash flow proves you can handle the loan repayments, making you a much more attractive borrower.

The demand for commercial credit in Australia, including business mortgage loans, has been growing steadily thanks to positive business conditions. As lenders adjust rates on variable loans, this active market often creates competitive opportunities for savvy borrowers. You can find out more about these trends in Australian commercial credit demand on Equifax. Understanding these costs and factors is what empowers you to make a smarter financial decision for your business.

A Step-by-Step Guide to the Application Process

Applying for a business mortgage can feel a bit like putting together a complex puzzle, but it’s much simpler when you break it down into clear, manageable steps. If you know what’s coming at each stage, you can prepare properly and move through the process with confidence.

Think of it as a collaborative effort. The lender needs to build a complete picture of your business's financial health and the viability of the property you want to buy. The more organised you are, the smoother and faster the whole thing will be. Let's walk through the key milestones.

Step 1: Initial Enquiry and Pre-Approval

It all starts with a conversation. This is where you’ll chat with a lender or broker about your goals, giving them a high-level overview of your business, how much of a deposit you have, and the kind of property you’re after. From here, you can get pre-approval.

While it isn't a final guarantee, pre-approval is a seriously powerful tool. It gives you a clear budget to work with and, more importantly, shows real estate agents that you’re a serious buyer. It’s basically a conditional 'yes' from the lender, pending a full assessment and property valuation.

Step 2: Formal Application and Documentation

Once you have pre-approval, it’s time to get down to the formal application. This is the most paper-heavy part of the process, where you’ll need to supply all the financial documents we’ve already covered—tax returns, profit and loss statements, and business activity statements. The aim is to give the lender a full and accurate picture of your ability to service the loan.

Being organised here is your biggest advantage. Having all your documents ready to go can shave significant time off the assessment. A well-prepared file shows you’re professional and makes the lender's job that much easier.

Step 3: Property Valuation and Conditional Approval

After you've lodged your application, the lender will organise an independent valuation of the commercial property. This is a crucial checkpoint to confirm the property’s market value and ensure it provides enough security for the loan. The valuer will look at its location, condition, and potential rental income.

If the valuation lines up with the purchase price and your financials stack up, the lender will issue a conditional approval. This means they're happy to proceed, as long as you meet any final conditions, like taking out building insurance.

Step 4: Formal Approval and Loan Settlement

With all the conditions met, you’ll get the official thumbs-up: formal or unconditional approval. At this stage, the lender sends over the loan documents for you to sign. Your solicitor or conveyancer then works with the lender’s legal team to lock in a settlement date.

Settlement is the final piece of the puzzle. This is when the funds are transferred to the seller, and the property title is officially moved into your business's name.

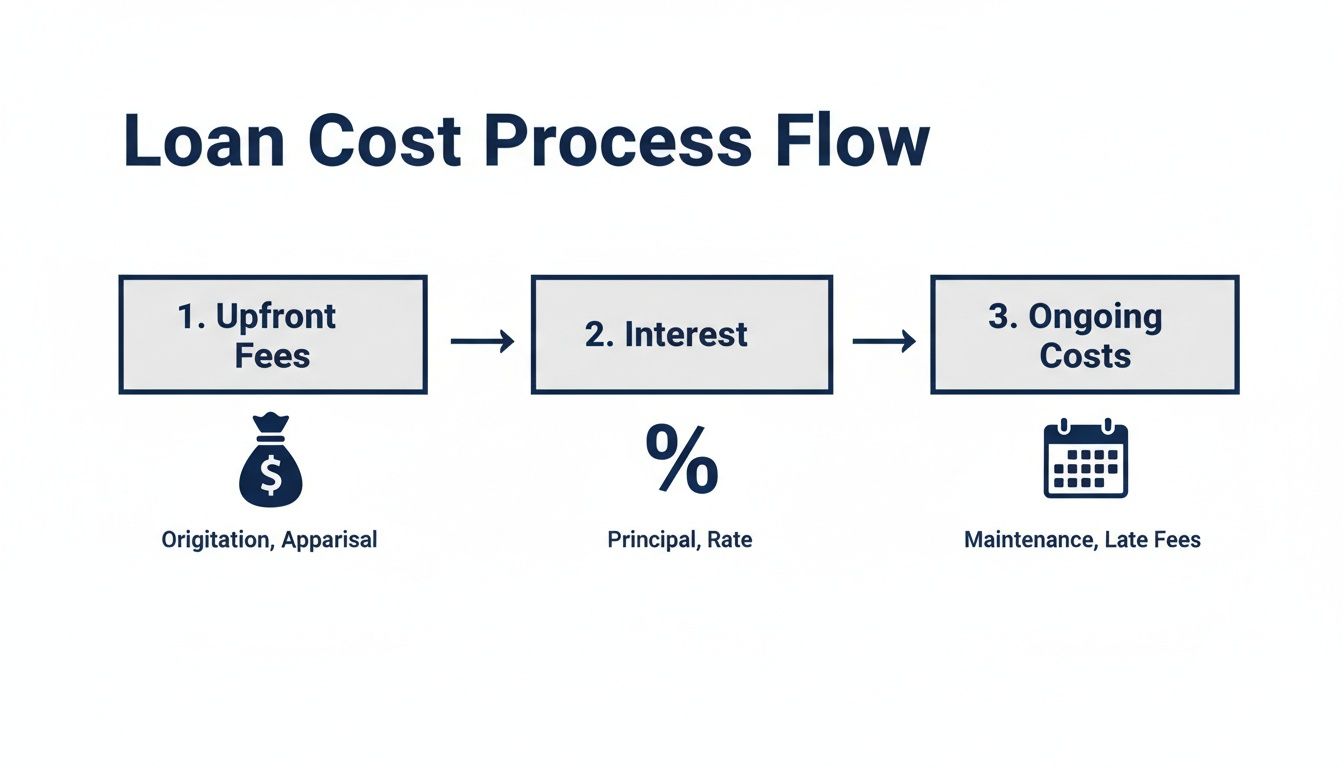

The image below breaks down the key costs you'll encounter along the way.

As you can see, there’s more to it than just the loan principal; upfront fees and ongoing costs are all part of the financial journey. With property investment becoming more popular, this process is more common than ever. In fact, new investment mortgage loans in Australia recently hit a record high, with over 57,000 commitments valued at almost $40 billion in a single quarter. You can read more about the surge in Australian investment loans to see the full picture.

How an Expert Partner Simplifies Your Journey

Navigating the world of business mortgages on your own can feel like you’re trying to find your way through a dense forest without a map. Every lender has its own unique policies, hidden requirements, and appetite for different types of deals. An expert partner, like a specialist mortgage broker, is your professional guide—clearing the path and leading you straight to your destination.

This partnership transforms a potentially stressful and time-consuming task into a streamlined, strategic process. Instead of spending weeks researching and applying to individual banks, you get immediate access to someone who already knows the entire landscape.

Gaining a Decisive Advantage

Working with a specialist gives you an insider's edge. They understand the subtle but critical differences between dozens of lenders, from the major banks to non-bank institutions and private funders who don’t even work with the public. That broad access is a game-changer.

A broker can match your unique situation—whether you’re self-employed with complex financials or need a low-doc solution—with the specific lenders most likely to say yes. They know which institutions are feeling favourable towards your industry and property type right now.

The real value of a broker is their ability to structure your application for success. They anticipate the lender’s questions, highlight your business's strengths, and package your financials in the most compelling way possible. This significantly boosts your chances of approval.

Saving Time and Reducing Stress

Beyond just finding a loan, an expert partner manages the entire process for you. They handle the tedious paperwork, chase up the lenders, and translate confusing industry jargon into plain English. That hands-on support is invaluable.

A broker's expertise doesn't just save you countless hours; it reduces the immense pressure that comes with securing a business mortgage loan. They act as your advocate and project manager, ensuring every detail is handled correctly from pre-approval all the way to settlement.

This lets you stay focused on what you do best—running your business—while they take care of the financing.

Frequently Asked Questions About Business Mortgages

Getting your head around business mortgages can bring up a few questions. To help clear things up, we’ve tackled some of the most common queries business owners have when they start looking into commercial property finance.

How Much Deposit Do I Need for a Commercial Property?

For most business mortgage loans in Australia, you'll generally need a deposit of between 20% and 35% of the property’s value. Lenders talk about this in terms of the Loan-to-Value Ratio (LVR), which for commercial real estate, they typically cap somewhere between 65% to 80%.

So, what does that look like in practice? Imagine you want to buy a warehouse for $1 million. If the lender offers you a 70% LVR, you can borrow $700,000. That means you’d need to come up with the remaining $300,000 as a deposit, plus have extra funds ready for costs like stamp duty and legal fees. The final LVR a lender will offer really depends on the strength of your application, the type of property, and their overall assessment of the risk.

Can I Use My SMSF to Buy a Commercial Property?

Yes, you absolutely can. It’s a popular strategy for business owners to buy their own premises using their Self-Managed Super Fund (SMSF). This is done through a very specific structure called a Limited Recourse Borrowing Arrangement (LRBA), which has a strict set of rules governed by the ATO.

The magic of an LRBA is in the "limited recourse" part. It means if something goes wrong and you default on the loan, the lender can only repossess the property itself. They can’t touch any of the other assets sitting in your SMSF. It’s a powerful way to build wealth inside your super, but it's also complex. Getting specialist financial and legal advice before you even think about starting is non-negotiable.

How Long Does the Approval Process Take?

From the moment you submit your application to finally settling on the property, the whole process for a business mortgage usually takes somewhere between four to eight weeks. This timeline covers a few key stages: the lender’s initial review, getting a conditional approval, the property valuation, formal approval, and then drawing up all the legal loan documents.

The biggest factor affecting the timeline is how organised you are. A clean, complete application with all the right documents from the start is the best way to avoid frustrating delays and keep the whole process moving forward.

Is a Commercial Loan Different from a Business Loan?

Yes, they are fundamentally different tools for different jobs. A business mortgage loan is a specialised type of finance used specifically to buy or refinance a physical commercial property. The property itself is the main security for the loan.

A general business loan, on the other hand, is usually for funding your day-to-day operations—things like boosting cash flow, buying stock, or paying for a marketing campaign. These loans can be unsecured or secured against other business assets like vehicles or equipment, but they aren't tied directly to a property purchase.