For Australian entrepreneurs, sole traders, and contractors, proving your income for a home loan can feel like an uphill battle. Traditional lenders often require two full years of tax returns and comprehensive financial statements, a rigid hurdle that doesn't always reflect the dynamic nature or true profitability of a successful business. This documentation gap can unfortunately stall property ambitions, leaving many self-employed individuals feeling locked out of the market.

This is precisely where low documentation (low doc) home loans come in. They offer a flexible and accessible pathway to property ownership by using alternative income verification methods, such as BAS statements, an accountant's letter, or business bank statements. But with a growing market full of specialist lenders and products, how do you navigate the options to find the right fit for your unique financial situation?

This comprehensive guide cuts through the complexity. We are diving deep into the best low doc home loans Australia has to offer, providing a clear and detailed roundup of top-tier options. We will explore leading non-bank lenders, specialist brokers like Diamond Lending, and powerful comparison platforms. For each provider, we’ll outline their key features, eligibility criteria, typical Loan-to-Value Ratios (LVRs), and potential fees, giving you the actionable insights needed to make a confident and informed decision. Forget the endless paperwork and frustrating application processes; it's time to find a home loan that truly understands and supports your business.

1. Diamond Lending

Best for: A guided, full-service brokerage experience for self-employed borrowers

Diamond Lending secures its position as a standout choice by acting as a specialist intermediary rather than a direct lender. For self-employed individuals, business owners, and property developers navigating the often-complex world of alternative documentation loans, this distinction is crucial. Instead of being limited to a single institution's rigid policies, Diamond Lending provides access to a broad panel of major banks and non-bank lenders, effectively unlocking a wider range of the best low doc home loans Australia has to offer. This model is built to find a 'yes' by matching a borrower's unique financial situation to the lender most likely to approve it.

The platform excels in delivering a human-led, consultative process from start to finish. It bypasses the impersonal, algorithm-driven pre-approvals common elsewhere, beginning instead with a 15-minute discovery call with a specialist. This initial conversation allows the team to understand the nuances of your income, business structure, and property goals, ensuring the subsequent application is positioned for success. This high-touch support continues through document guidance, pre-approval, and final settlement, significantly reducing the administrative burden and stress for time-poor professionals.

Why Diamond Lending Stands Out

What truly sets Diamond Lending apart is its deep specialisation in complex lending scenarios combined with its extensive market access. Many mainstream banks are hesitant to proactively offer low-doc solutions, often burying them in policy exceptions. Diamond Lending brings these options to the forefront, leveraging strong relationships with lenders like Commonwealth Bank, ANZ, Westpac, NAB, and Macquarie, alongside flexible non-bank partners. This dual access means they can cater to a diverse clientele, from a sole trader with irregular income seeking their first home to a seasoned developer financing a new construction project.

Furthermore, the brokerage integrates practical tools and ancillary services to provide a holistic solution. Their website features a suite of calculators (borrowing power, stamp duty, and repayment) that empower borrowers to conduct initial due diligence. By also facilitating connections for home insurance, they streamline the entire property acquisition journey, allowing clients to consolidate their lending and protection needs through a single, trusted point of contact.

Expert Insight: The primary advantage of using a specialist brokerage like Diamond Lending is policy navigation. Each lender has unique criteria for accepting alternative income verification. A broker who understands these intricate differences can save you from failed applications that negatively impact your credit file, directing you straight to the lenders best suited for your specific documentation.

Key Features and Offerings

- Specialist Low-Doc and No-Doc Pathways: Expert guidance on preparing and presenting alternative income verification documents, such as BAS statements, accountant's letters, or bank statements.

- Extensive Lender Panel: Direct access to major banks and non-bank financial institutions, enabling genuine side-by-side loan comparisons to secure competitive rates and terms.

- End-to-End Human Support: A guided process from the initial 15-minute phone call to settlement, minimising complexity for the borrower.

- National Coverage: While headquartered in Melbourne, the team offers both in-person and remote consultations to service clients across all Australian states and territories.

- Integrated Financial Tools: Free online calculators for borrowing power, stamp duty, and repayments help with initial financial modelling.

Pros & Cons

| Pros | Cons |

|---|---|

| ✅ Specialist support for self-employed and complex applications that many banks won't proactively offer. | ❌ No standard interest rates or brokerage fees are published online; costs depend on the lender and must be clarified upfront. |

| ✅ Wide lender panel allows for tailored recommendations and competitive comparisons. | ❌ As a broker, approval timelines and final decisions are subject to the policies of third-party lenders. |

| ✅ A guided, human-led process reduces stress and the risk of application errors. | ❌ The final loan product and its features are determined by the lender, not the brokerage itself. |

| ✅ National coverage and integrated insurance partnerships create a streamlined, one-stop-shop experience. |

Website: https://diamondlending.com.au

2. Liberty Financial — Low Doc Home Loans

Liberty Financial has carved out a significant niche in the Australian lending market as a leading non-bank lender, particularly for borrowers who don't fit the traditional mould. Their website offers a dedicated and transparent portal for self-employed individuals searching for some of the best low doc home loans in Australia. Unlike many competitors who keep their cards close to their chest, Liberty’s platform is refreshingly upfront, providing clear details on features, maximum Loan-to-Value Ratios (LVRs), and loan terms before you even start an application.

This direct approach demystifies the low doc process. The website clearly outlines its flexible income verification methods, allowing applicants to use Business Activity Statements (BAS), bank statements, or a declaration from their accountant instead of providing full tax returns. This flexibility is a game-changer for business owners with complex or fluctuating income streams.

Key Features and Offerings

Liberty Financial stands out by combining the flexibility of a specialist lender with the product features typically associated with major banks. Their transparent product pages detail offerings for both owner-occupiers and investors, a crucial distinction for portfolio builders.

- Flexible Income Verification: Choose from 12 months of BAS, six months of business bank statements, or an accountant's declaration.

- High LVR and Loan Amounts: Borrow up to 85% of the property's value, with loan sizes ranging from a modest $50,000 to a substantial $8,000,000.

- Full-Featured Loans: Gain access to a 100% offset account (linked to a Visa debit card), free online redraw facilities, and the ability to split your loan into different portions.

- Broad Loan Options: The platform details options for principal and interest or interest-only repayments, fixed or variable rates, and impressively long loan terms of up to 40 years.

Using the Liberty Financial Platform

The website is designed for user clarity. You can easily navigate to the "Low Doc Home Loans" section, where products are laid out with their starting rates, comparison rates, and key features. While the application can be initiated online, Liberty also promotes its network of "Liberty Advisers," offering a hybrid digital-and-human approach.

Pro Tip: Use the website to familiarise yourself with the product features and LVR caps first. Then, when you engage with a broker or a Liberty Adviser, you can have a much more specific and productive conversation about how your financial documents align with their best-suited product.

Pros & Cons

Pros:

- Exceptional Transparency: The website publicly lists LVRs, loan features, and comparison rates, which is uncommon in the specialist lending space.

- Rich Feature Set: Access to a genuine offset account and loan splits provides a level of financial flexibility often missing from other low doc products.

- Investor-Friendly: Dedicated low doc options are available for property investors.

Cons:

- Variable Pricing: The advertised "rates from" are indicative; your final interest rate will be determined by your specific application, LVR, and credit assessment.

- Non-Bank Offset: While the offset facility is a major plus, it's important to note that deposits held with non-bank lenders like Liberty are not covered by the Australian Government's Financial Claims Scheme (FCS).

Website: https://www.liberty.com.au/home-loans/low-doc-home-loans

3. Bluestone Home Loans — Alt‑Doc

Bluestone has established itself as a premier specialist lender in Australia, championing a flexible, case-by-case approach for borrowers outside the prime lending space. Their website is a valuable resource for self-employed individuals, clearly outlining their "Alt-Doc" pathway, which is their term for low doc lending. The platform moves beyond rigid algorithms, emphasising its human-centric underwriting process designed to understand the real financial story of a business owner.

This philosophy is reflected in the website’s content, which openly discusses options for those with complex income or credit blemishes. Bluestone’s platform details its multiple income verification methods, including Business Activity Statements (BAS), business bank statements, or a letter from an accountant. This flexibility makes them a strong contender for some of the best low doc home loans in Australia, especially for entrepreneurs whose financials don't fit neatly into traditional boxes.

Key Features and Offerings

Bluestone's strength lies in its tailored solutions and willingness to assess applications on their individual merits. The website provides a helpful rates and fees guide specifically for self-employed applicants, offering a degree of transparency that builds confidence.

- Flexible Income Verification: Applicants can evidence their income using 12 months of BAS, six months of business bank statements, or a formal accountant's letter.

- High LVR and No LMI: Borrow up to 90% of the property value on certain loan tiers without paying Lenders Mortgage Insurance (LMI), although a risk fee may apply instead.

- Full-Featured Loans: Options for offset accounts are available, providing a valuable tool for reducing interest payments.

- Tolerance for Credit Issues: The platform acknowledges that financial setbacks happen and shows a willingness to consider applicants with past credit impairments.

Using the Bluestone Home Loans Platform

The Bluestone website serves as an informational hub, detailing its product philosophy and requirements. While you can find indicative rates and product information, the primary call to action is to connect with an accredited mortgage broker. Their model is heavily broker-supported, leveraging professionals to package and present complex applications effectively.

Pro Tip: Before speaking to a broker, use the "Solutions for Self-Employed" section on the Bluestone website to understand their verification options. This allows you to gather the right documents (e.g., your last four BAS) and have a more productive initial discussion with your broker.

Pros & Cons

Pros:

- High LVR Potential: The ability to borrow up to 90% LVR with alt-doc verification is a significant advantage for borrowers with a smaller deposit.

- No LMI: Replacing LMI with a risk fee can simplify costs and is a key feature of their product structure.

- Multiple Evidence Options: The clear acceptance of BAS, bank statements, or an accountant's letter provides excellent flexibility.

Cons:

- Indicative Pricing: The published rates are a guide; your final rate will be risk-based and may include loadings for factors like interest-only terms or loan size.

- Broker-Led Process: Direct applications are not the standard pathway, which means working through a mortgage broker is a necessary step for most borrowers.

Website: https://bluestone.com.au/solutions/self-employed/

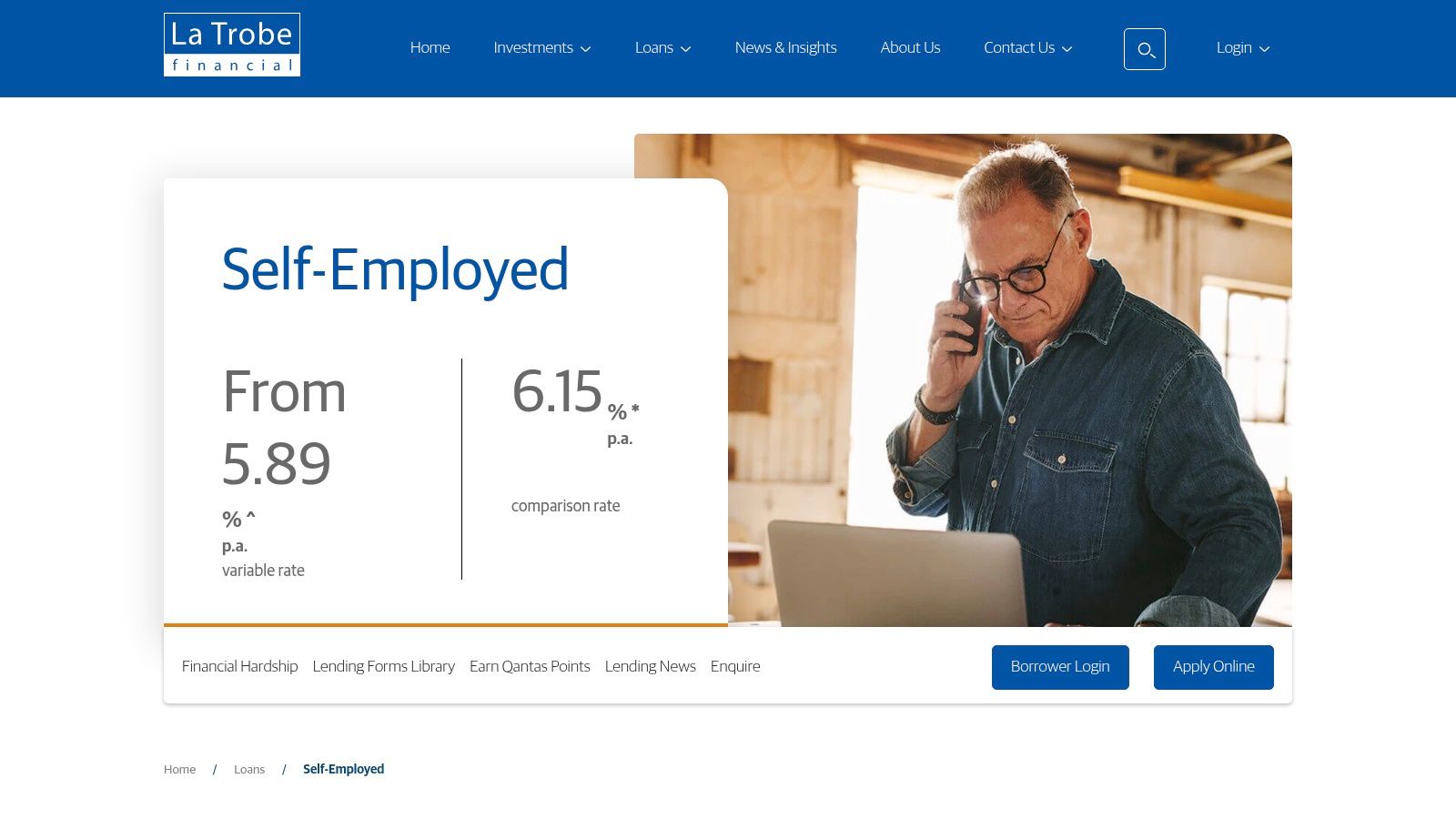

4. La Trobe Financial — Self‑Employed “Lite Doc”

La Trobe Financial is a seasoned player in the Australian specialist lending market, offering a well-defined alternative for self-employed borrowers through its trademarked "Lite Doc" home loan. Their website clearly segments its offerings, making it straightforward for business owners to find a pathway to finance without traditional income documentation. Rather than hiding behind broker-only access, the platform provides public-facing details on its Lite Doc product, including starting interest rates and specific income verification requirements, which is a major confidence booster for applicants researching their options.

This clarity demystifies what is often a complex process. The website details how applicants can use documents like Business Activity Statements (BAS), trading statements, or a formal letter from their accountant to prove their income. This targeted approach is ideal for established business owners who may not have up-to-date tax returns but can easily provide alternative evidence of consistent business turnover.

Key Features and Offerings

La Trobe Financial’s strength lies in its experienced-backed, clearly defined product for the self-employed. The website lays out the core features that differentiate its Lite Doc offering, ensuring borrowers know what to expect from the outset.

- Alternative Income Verification: Use 12 months of BAS, six months of business trading statements, or an accountant's letter to verify your income.

- Published Rates and LVRs: The website is transparent about its starting variable rates (example from 6.09% p.a.) and allows borrowing up to 80% of the property's value.

- No LMI Required: A significant advantage is that Lenders Mortgage Insurance (LMI) is not required on their Lite Doc loans up to the specified 80% LVR limit.

- Large Loan Potential: The platform caters to a wide range of needs, supporting substantial maximum loan sizes, subject to the LVR and property location.

- Direct and Broker Access: You can make an enquiry directly through the website to speak with a lending consultant or access their products via a finance professional.

Using the La Trobe Financial Platform

The website is designed for easy navigation, with a dedicated "Self-Employed Loan" page that outlines the differences between their Full Doc and Lite Doc products. This side-by-side comparison helps users quickly determine their eligibility and understand the trade-offs. The clear calls-to-action guide you towards making an online enquiry, connecting you with an internal consultant who can discuss your specific financial situation. For a deeper understanding of the documents required, you can explore our guide which explains what freelancers and business owners need to prepare.

Pro Tip: Review the "Key Facts Sheet" available for the Lite Doc product on their website. This document provides a comprehensive breakdown of potential fees, charges, and loan terms, helping you calculate the total cost of the loan beyond just the interest rate.

Pros & Cons

Pros:

- Clear Product Segmentation: The distinction between Full Doc and Lite Doc products is exceptionally clear, with transparent criteria listed online.

- Deep Specialist Experience: As a national lender, La Trobe Financial has extensive experience in the specialist lending space, including low doc home loans.

- No LMI on Lite Doc: Avoiding LMI on loans up to 80% LVR can result in substantial savings for the borrower.

Cons:

- Lower Max LVR: The 80% LVR cap on Lite Doc loans is lower than some non-bank competitors who may offer up to 85% or higher.

- Application Fees Apply: Be aware of establishment or application fees (which can start from around $995), and be sure to factor these into your overall loan cost comparison.

Website: https://www.latrobefinancial.com.au/lending/self-employed-loan/

5. Pepper Money — Alt‑Doc

Pepper Money is a major non-bank lender in Australia that has embraced the modern, regulated landscape of specialist lending. Their website serves as both an educational hub and a direct portal for their "Alternative Documentation" (Alt-Doc) home loans. This approach is crucial, as Pepper Money clearly explains the shift away from old "no-doc" practices to the current, more responsible Alt-Doc framework, helping self-employed borrowers understand their obligations under the National Consumer Credit Protection (NCCP) Act.

This focus on education and compliance makes their platform a valuable resource. It demystifies what is possible in today's market, providing a clear pathway for business owners who may not have two full years of tax returns. A key differentiator for Pepper is their flexibility around business history, often considering applicants with ABN/GST registration as short as six months, a feature that sets them apart from more conservative lenders.

Key Features and Offerings

Pepper Money’s strength lies in its risk-based assessment, allowing it to cater to a broad spectrum of self-employed borrowers, from near-prime to specialist credit profiles. Their website outlines a clear alternative to the rigid documentation requirements of mainstream banks.

- Modern Alt-Doc Pathway: Adheres strictly to NCCP guidelines, using income evidence like BAS, business bank statements, or an accountant's letter.

- Flexible ABN/GST History: Unlike many lenders who demand a two-year history, Pepper may consider businesses operating for as little as six months.

- Broad Product Suite: Offers a range of home loan products for different needs, including purchasing, refinancing, and cash-out for business purposes.

- Educational Resources: The website's help centre provides up-to-date, regulator-aligned guidance on the current low-doc and alt-doc landscape.

Using the Pepper Money Platform

The Pepper Money website is structured to guide users from understanding the product to starting an application. The "Help Centre" is an excellent starting point for anyone confused about the terminology of low doc versus alt-doc. From there, users can explore product details before connecting with a Pepper Money accredited broker to proceed. This broker-centric model ensures applicants receive tailored advice. You can see how this flexibility helps real borrowers by reading this detailed low doc case study.

Pro Tip: Use the educational articles on Pepper’s site to understand what kind of income evidence you'll need to prepare. Having your BAS or business bank statements organised before you speak to a broker will significantly speed up the application process.

Pros & Cons

Pros:

- Excellent for New Businesses: Their willingness to consider applicants with short ABN/GST histories opens doors for newer, successful businesses.

- Strong Educational Focus: The platform provides clear, compliant information, which builds trust and helps borrowers understand the process.

- Well-Established Specialist: As a well-known non-bank lender, they have a national distribution network and a trusted reputation in the broker community.

Cons:

- No True "No-Doc" Loans: In line with regulations, all applicants must provide alternative evidence of income; there are no "no questions asked" options.

- Risk-Based Pricing: Your final interest rate and applicable fees are heavily dependent on your risk grade and LVR, which can be higher than standard bank loans.

Website: https://www.peppermoney.com.au/lending/help-centre/getting-started/low-down-on-low-doc-home-loans

6. Finder — Low‑Doc Home Loans (comparison platform)

Finder is one of Australia's largest and most recognised comparison websites, and its dedicated section for low doc home loans serves as an excellent starting point for self-employed borrowers. Rather than being a direct lender, Finder acts as a marketplace, aggregating and presenting loan options from a wide range of banks and non-bank lenders. This provides a valuable bird's-eye view of the market, allowing you to compare some of the best low doc home loans in Australia in a single, user-friendly interface.

The platform is particularly useful for an initial market scan. It demystifies the landscape by laying out key metrics like interest rates, comparison rates, and fees in a consistent format. This side-by-side view helps you quickly shortlist potential lenders before diving deeper into the specifics of their application processes or engaging with a broker.

Key Features and Offerings

Finder’s strength lies in its data aggregation and educational content, which is tailored to help self-employed individuals understand their options. The platform clearly explains the concept of alt-doc lending and why true no-doc loans are generally not available for consumer lending under Australian credit laws.

- Filterable Comparison Tables: Easily sort and filter low doc loan products by variable rates, fees, features, and other crucial metrics to narrow down your search.

- Editorial Explainer Content: The site features extensive guides and articles explaining how low doc loans work, what income verification is required, and tips for applying.

- Regularly Updated Information: The comparison pages are frequently updated to reflect the latest rates and product offerings from lenders, ensuring the data is timely.

- Direct Lender Links: Once you identify a suitable product, you can use the 'Go to site' button to navigate directly to the lender's website to begin an application or find more information.

Using the Finder Platform

The website is designed for simplicity. You can quickly access the low doc loans page and immediately see a table of available products. The filters allow you to customise the results based on your needs, such as property value and deposit amount. Each listing provides a snapshot of the loan, including revert rates and key features, saving you the time of visiting multiple lender websites.

Pro Tip: Use Finder as your research launchpad. Identify two or three promising lenders from the comparison table, then visit their websites directly or discuss them with a mortgage broker. This ensures you verify the specific details and understand any nuances not captured in the summary table.

Pros & Cons

Pros:

- Broad Lender Coverage: See a wide array of products from different lenders in one place, making initial comparisons fast and easy.

- Helpful Explainer Content: The platform provides valuable educational resources targeted at self-employed borrowers, clarifying complex lending terms.

- Easy-to-Use Interface: The consistent data layout and filtering options make it simple to compare key loan metrics side-by-side.

Cons:

- Potential for Bias: Search results and listings may prioritise commercial partners or promoted placements, so it's not always an exhaustive, neutral list.

- Incomplete Market View: Not every low doc home loan product available in Australia will be featured on the site, so it shouldn't be your only source of research.

Website: https://www.finder.com.au/home-loans/low-doc-loans

7. InfoChoice — Low‑Doc Home Loans (comparison platform)

InfoChoice serves as a valuable research hub for borrowers navigating the specialised world of low doc home loans in Australia. Rather than being a direct lender, it's a comprehensive comparison website that aggregates offers from a wide array of banks, non-bank lenders, and credit unions. Its strength lies in combining educational resources with powerful comparison tools, allowing self-employed individuals to survey the market from a single, well-organised platform.

The platform demystifies complex topics by providing a dedicated Low-Doc category page filled with clear definitions, guides on borrowing caps, and notes on potential fees. This approach empowers users with foundational knowledge before they even begin comparing rates. InfoChoice often includes smaller, lesser-known lenders that might not appear on larger comparison sites, offering a broader and more diverse view of the market.

Key Features and Offerings

InfoChoice stands out by equipping users with both the information and the tools needed to make an educated decision. It acts as a starting point to identify potential lenders that align with a borrower's specific financial situation.

- Dedicated Low-Doc Category: A specific section of the site focuses solely on low doc products, complete with detailed FAQs and explainer content.

- Frequently Refreshed Rate Tables: The platform provides regularly updated comparison tables and "lowest-rate" round-ups, giving users a current snapshot of the market.

- Sorting and Filtering Tools: Users can easily narrow down their options by filtering loans based on interest rates, LVR, and specific features like offset accounts or redraw facilities.

- Access to Niche Lenders: The site often features smaller lenders and credit unions, providing a more comprehensive market overview than some of its larger competitors.

Using the InfoChoice Platform

The website is designed for straightforward research and comparison. You can navigate directly to the "Low Doc Home Loans" section to view a list of available products. Each listing typically shows the lender, interest rate, comparison rate, and key features. From there, users can click through for more details or be directed to the lender's website or a partner broker to proceed.

Pro Tip: Use InfoChoice's filters to create a shortlist of 3-4 potential lenders. Pay close attention to the comparison rate, as this gives a more realistic indication of the loan's true cost once standard fees are included.

Pros & Cons

Pros:

- All-in-One Resource: Combines helpful explainer content with powerful comparison functionality, making it an excellent educational tool.

- Broader Market View: Often includes smaller or niche lenders that provide competitive low doc options not always highlighted elsewhere.

- User-Friendly Interface: The sorting and filtering tools make it easy to narrow down a potentially overwhelming number of products.

Cons:

- Not an Exhaustive List: The platform does not feature every lender or product on the market, and some placements may be influenced by commercial partnerships.

- Based on Standard Assumptions: The rates and figures shown are based on standardised scenarios; you must confirm your specific eligibility and final pricing directly with the lender.

Website: https://www.infochoice.com.au/home-loans/low-doc

Top 7 Low‑Doc Home Loans in Australia — Comparison

| Provider | Implementation complexity | Resource requirements | Expected outcomes | Ideal use cases | Key advantages |

|---|---|---|---|---|---|

| Diamond Lending | Low — broker handles process, guided steps | Client documents as advised; broker engagement; possible lender-specific docs | Access to fit-for-purpose loans including low/no-doc and specialist options; timing depends on lenders | Self‑employed, credit‑impaired, renovators, developers, those needing tailored support | Wide lender panel; specialist low/no‑doc expertise; human‑led end‑to‑end support; calculators & insurance partnerships |

| Liberty Financial — Low Doc Home Loans | Medium — apply online or via adviser | BAS/bank statements/accountant declaration; standard lending docs; deposit/LVR info | Transparent product terms (published caps, starting rates); competitive features and clear pricing signals | Self‑employed owner‑occupiers and investors seeking clear low‑doc products | Published LVRs, features and comparison rates; large loan sizes; offset/redraw features |

| Bluestone Home Loans — Alt‑Doc | Medium–High — broker‑led, case‑by‑case underwriting | BAS, business bank statements, accountant’s letter; broker coordination | Flexible approvals, fast assessment, potential high LVR (up to 90%) and no LMI in some cases | Self‑employed with complex income, high LVR needs, or credit blemishes | Explicit alt‑doc pathways; high potential LVRs; broker underwrite for complex cases |

| La Trobe Financial — Lite Doc | Medium — direct or broker application | BAS/trading statements or accountant’s letter; possible application fees | Clear Lite Doc outcomes with published starting rates and up to 80% LVR (no LMI within limits) | Self‑employed applicants wanting transparent product segmentation | Distinct Full Doc vs Lite Doc products; published rates and criteria; experienced specialist lender |

| Pepper Money — Alt‑Doc | Medium — specialist non‑bank with educational resources | Alt‑doc evidence; may accept short ABN/GST histories; case assessment | Regulator‑aligned guidance and specialist consideration; pricing varies by risk | Self‑employed with short trading history or needing guidance on alt‑doc rules | Up‑to‑date educational content; national specialist lender with alt‑doc paths |

| Finder — Low‑Doc Home Loans (comparison) | Low — user-driven market scan | No documents required for comparison; time to research and shortlist | Quick market overview, shortlist of lenders and features; may include promoted listings | Initial comparison and shortlisting for self‑employed borrowers | Broad coverage, filterable comparisons and explainer content linking to lenders |

| InfoChoice — Low‑Doc Home Loans (comparison) | Low — user-driven comparison | No documents required; time to compare tables and round‑ups | Alternate market view with refreshed lowest‑rate round‑ups; may surface smaller lenders | Finding smaller lenders or checking alternate comparator results | Includes smaller lenders and regularly refreshed rate round‑ups; explanatory FAQs |

Your Next Step Towards a Low Doc Home Loan Solution

Navigating the landscape of low doc home loans in Australia can feel complex, but as we've explored, a wealth of specialised solutions exists for self-employed individuals, business owners, and savvy investors. This guide has unpacked some of the leading options, from direct non-bank lenders like Liberty Financial and Pepper Money to comprehensive comparison platforms such as Finder and InfoChoice. Each offers a unique pathway to property ownership when traditional documentation is a hurdle.

The key takeaway is that securing one of the best low doc home loans in Australia isn't about finding a one-size-fits-all product. It's about finding the perfect lender-borrower alignment. Lenders like Bluestone and La Trobe Financial have carved out niches by accepting alternative income verification, but their specific requirements for ABN registration, GST history, and acceptable documents vary significantly. Understanding these nuances is the difference between a swift approval and a frustrating decline.

Key Insights Recapped

Let's distill the most critical points from our review:

- Documentation Varies: A "low doc" loan for one lender is an "alt doc" for another. Some may accept a 6-month BAS, while others might require an accountant's letter plus 12 months of business bank statements.

- Interest Rates and LVRs are Linked: Generally, the higher the Loan-to-Value Ratio (LVR) you seek, the more robust your alternative documentation needs to be. A higher deposit often unlocks more competitive interest rates.

- Comparison is Crucial, but Incomplete: While platforms like Finder and InfoChoice are excellent for initial research and comparing advertised rates, they don't capture the intricate policy details that determine your actual eligibility.

- Your Business Structure Matters: Lenders assess sole traders, partnerships, and companies differently. The strength of your application can depend heavily on how well your business's financial story is presented.

Creating Your Low Doc Loan Strategy

Armed with this information, your next steps should be strategic and targeted. Don't fall into the trap of submitting multiple applications hoping one will stick; this can negatively impact your credit file. Instead, focus on a methodical approach.

First, organise your financial documents. Gather everything you can, including recent BAS, business bank statements for the last 6-12 months, an accountant's declaration, and any business profit and loss statements. Having these ready will streamline the process, regardless of the lender you choose.

Next, critically assess your financial position. Be realistic about your deposit size and what LVR you can comfortably achieve. This self-assessment will help you narrow down the list of potential lenders, as some specialise in LVRs up to 85%, while others are more conservative.

Expert Insight: The most successful low doc loan applications are those presented with a clear and compelling narrative. Lenders need to understand the health and trajectory of your business. A specialist broker excels at crafting this narrative, connecting the dots between your bank statements, BAS, and overall business performance to build a strong case for approval.

This is where the value of expert guidance becomes undeniable. Navigating the intricate policies of different lenders is a full-time job. A specialist mortgage broker who lives and breathes this market knows which lenders are currently favourable to your specific industry, income type, and loan requirements. They can prevent you from wasting time on lenders whose hidden criteria would lead to an automatic rejection. By partnering with an expert, you transform a challenging process into a clear, manageable journey, significantly boosting your chances of securing the ideal property finance solution.

Ready to find the right low doc home loan without the guesswork? The expert brokers at Diamond Lending specialise in structuring applications for self-employed Australians, matching your unique circumstances with the most suitable lenders from their extensive panel. Start with a simple 15-minute, no-obligation chat to get a clear strategy for your property goals by visiting Diamond Lending today.